Investment consultants re-arranging deck chairs

Investment consultants re-arranging deck chairs

I make no secret of the fact that I dislike investment consultants. But I probably will never write what I really think about them here because if I ever lose my job and move back to the asset management world, I might have to work with them again. And if they know what I think about them, I probably would be black balled by pension funds and their investment consultants everywhere.

Because if there is one truism that every asset manager knows it is that investment consultants have enormous influence over the pension funds they advise. Investment consultants are the gatekeepers that can prevent even the best asset manager from ever being invited to a pitch again.

So, let’s focus on a harmless and largely inconsequential example of the influence investment consultants have on pension funds. A team of researchers from the University of Missouri collected data on how pension funds benchmark their investments in private equity. In general, benchmarks for private equity investments can be either the performance of a peer group or the performance of public equity markets plus a required excess return above that. And of course, one could choose to compare the investments against a local benchmark or a global benchmark.

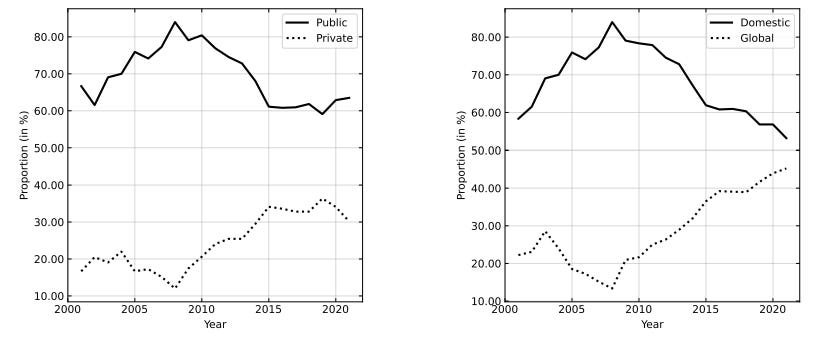

The chart below shows that over the last five to ten years, pension funds have increasingly shifted toward using global benchmarks (probably reflecting the more global reach of many of their investments) and private benchmarks, i.e. they compare their private equity investments to a peer group rather than listed stocks.

Benchmark choice for private equity investments.

Source: Augustin et al. (2023). Note: Public vs. private benchmark on the left and global vs. domestic benchmark on the right.

However, the majority of private equity investments is still benchmarked against listed equities, but it is notable that the required spread above listed equity returns has declined dramatically from 420bps in 2000 to 280bps today. Is this a reflection of the lower returns of private equity investments over time or investment consultants lowering the hurdle for their fund selectors so they don’t get blamed for selecting poor performing private equity funds? I don’t know.

But what really stood out for me in the research paper was the discussion of the influence investment consultants have over the choice of benchmark. To quote from the paper:

“Investment consultants play an important role in the benchmarking process for US public pension funds, even though it is often the pension fund’s board of trustees that sets overall investment and portfolio policies.

We find that pension fund allocations and the use of PE [investment consultants] positively predict the choices of the types of benchmarks that used. However, major changes to the benchmarks such as the base (e.g., S&P 500 vs. Russell 2000 vs. Cambridge Associates) or to the spread overlaid on the base index are driven by changes in the general [investment consultants]. General [investment consultants] also drive changes in the PE [investment consultants], potentially this serves as a way for the new general [investment consultant] to make their mark.”

And I will leave it at that.

I have long had concerns that Solvency II is driving insurance companies to allocate too much to private equity and other "alternatives" rather than liquid equities to balance their perpetual overweight position in bonds, and perhaps pension funds are falling into the same trap for different reasons.

Pension funds have one fiduciary duty: Pay the promised pensions to their plan participants. When did benchmark or peer-relative performance become important at all? Perhaps it's a bit like the endowment size race at elite US universities; bragging rights on growing the pile have taken on more importantance than actually using the funds for education.