Is the carbon premium real?

As many readers will know, I have long been saying that companies with lower greenhouse gas emissions intensity outperform companies with higher emissions intensity. I rested my view on studies I have written about before (e.g. here) that show that there is a systematic outperformance of ‘green stocks’ vs. ‘brown stocks’. This is one of these posts where I have to put ashes on my head because it may well be that this research fell prey to an unintended forward-looking bias.

Shaojung Zhang from Ohio State University has written a paper that re-examines the results of previous papers on the performance differences between green and brown stocks. What these papers have typically done is use emissions data as reported in databases like Bloomberg or Refinitiv. As is common in such studies, one typically uses data from the middle of the year following the year for which the data applies, i.e. June of year 1 for data concerning year 0.

This is done because it is well known that there is a publication lag. Data for a fiscal year is typically published only several months later in an annual report and then it takes another month or two for this data to show up in databases of data vendors. For accounting data, a six-month delay has become a standard approach in research since this is plenty of time to publish an annual report and then get that data into Bloomberg.

But for ESG data, Zhang realised the time lag is much longer. CDP, for example, updates its emissions database only once per year in October, which is a 10-month lag on the year the emissions data relates to. Trufin and MSCI seem to have similar time lags of 10 to 12 months.

This means that if one uses emissions data in the middle of the year, it will show the accurate historical data for both accounting metrics and emissions metrics in the database but the emissions data would not have been available at the middle of the year. In a sense, backtests use emissions data that would only have been available four to six months later.

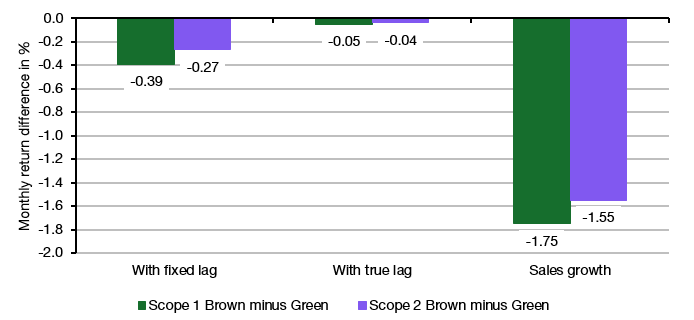

What happens if one uses only emissions data as published on these ESG databases? In other words, what happens when the time lag is increased from six months to ten or twelve months? Unfortunately, nothing good. The performance difference between brown stocks and green stocks as reported in the literature almost entirely disappears once corrected for other factors like valuations, profitability, sales growth, etc.

Underperformance of brown vs. green stocks in the US

Source: Zhang (2024)

What Zhang shows is that the previous studies on carbon risk picked up the correct accounting data but the incorrect emissions data. But because emissions are essentially a function of sales, the resulting outperformance of green stocks vs. brown stocks can almost entirely be explained by the difference in sales growth between green and brown companies.

This is the mistake that we made, and I need to apologise to readers for promoting studies (and using that insight myself) that have turned out to be flawed. But this is science, and I am not ashamed of that mistake. I always use the best knowledge available at any given time. Our knowledge constantly evolves, and we get better. This is why we no longer use bloodletting to cure diseases. Science and research get things wrong, but we correct our mistakes, learn from them, and then move on to greener pastures. And I intend to do so here as well.

Because there is a silver lining in all this. The brown minus green performance difference may not be due to a risk premium on carbon emissions intensity but rather a premium on higher sales growth, but guess which products and services have higher sales growth? In the automotive sector electric vehicles have much higher sales growth than internal combustion engines, despite the recent setbacks in EV sales. In energy infrastructure, wind and solar have sales growth rates that are multiples higher than oil or gas. In all kinds of consumer and industrial products, greener product growth beats the sales growth of traditional products by a wide margin. In other words, green stocks still outperform brown stocks, not because of their lower emissions but because of their higher growth.

Acknowledging previous mistakes let alone apologising is rare and much appreciated.👍

Well done for publicly correcting the error.

Always good to look at the original data.