Sometimes, you have to wonder if they know what they are doing

Sometimes, you have to wonder if they know what they are doing

It is Fed Day (again) and if markets are to be believed, today will be the day when the Fed will cut interest rates for the first time in this cycle.

I have written before that I think central banks (or anyone, really) do not really understand how inflation works or how monetary policy should be conducted to manage inflation. No policymaker would ever admit to that, but at the very least our understanding of the link between monetary policy, inflation, and unemployment is tenuous.

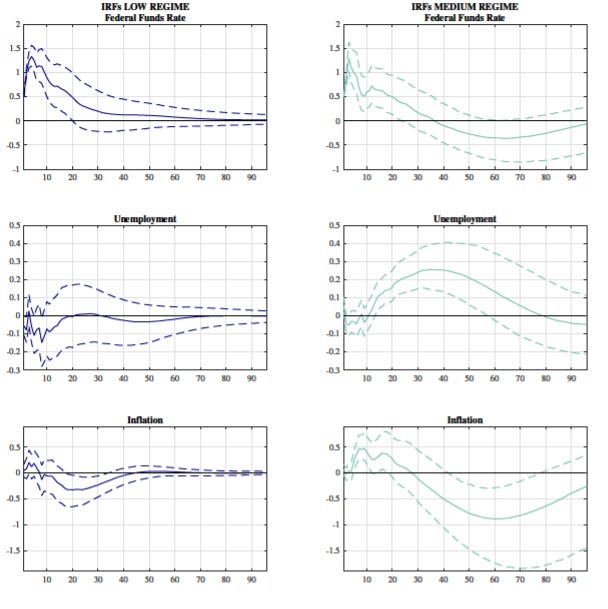

But sometimes, you come across a piece of research that makes that point for you, though inadvertently. Valeria Gargiulo and her collaborators have analysed the impact of rate hikes by the Federal Reserve on inflation and unemployment in the US. However, their approach was to split their analysis into different periods determined by the prevailing level of inflation. They define an environment of low inflation as one where annual inflation rates are below 5.5%, while an environment of medium inflation is defined as inflation rates between 5.5% and 11%. Finally, high inflation is defined as above 11%. These thresholds are defined based on the historical experience of inflation in the US between 1970 and 2007.

Then they estimate a VAR model with different lags for each of these environments and find that monetary policy has significantly different leads to and impacts on inflation and unemployment. The chart below shows the results for the low and medium inflation regimes.

Impact of rate hikes on inflation and unemployment for different levels of inflation

Source: Gargiulo et al. (2024)

In the low inflation environment, unemployment rates do not increase in response to a 0.5% increase in interest rates but drop by about 0.1% after nine months or so. Inflation, on the other hand, drops by about 0.5% 18 to 20 months after a 50bps rate hike.

In the medium inflation regime where inflation rates are above 5.5%, a 50bps rate hike by the Fed creates an increase in unemployment rates of about 0.25% three to four years later. And it creates a 0.9% drop in inflation rates as late as five years after the rate hike.

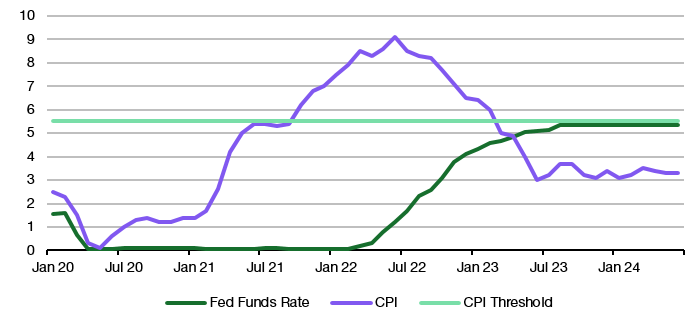

Note that I said above that their analysis uses the years 1970 to 2007, so now we have an out-of-sample event to test their results. In 2021, the Fed hiked interest rates from 0.25% (Upper Bound) to 4.75% while inflation was above 5.5% and from 4.75% to 5.5% while it was back down below that threshold.

Based on the results of the study, unemployment rates in the US should have started to rise at the start of 2024 and continue to rise until 2026. Meanwhile, the impact on inflation should kick in only in 2025. But the last three rate hikes from 4.75% to 5.5% should have no impact on unemployment and should start to reduce inflation in 2025.

But so far, we haven’t seen unemployment rise a lot, while inflation has dropped a lot. So, could it be that the latest rate hike cycle is again completely different from the average of the past? Maybe. Or maybe not. The fact that unemployment rates have remained low in 2024 is well within the errors of the model. In which case we should expect unemployment to rise significantly in the next twelve months while the US may get a massive deflationary shock.

It’s not impossible but I find that rather unlikely. Especially, if you start checking when inflation in the US was low (below the 5.5% threshold) and when it was high. Looking back to 1970 the only periods of inflation above 5.5% I could find were in the 1970s and early 1980s. Since then, we have always been in a low-inflation environment.

But back in the 1970s, the relationship between monetary policy and inflation/unemployment was very different. We had more rigid labour markets with stronger unions and stronger bargaining power for workers. We have monetary policy that was conducted by managing the growth of money supply instead of interest rate targeting. And we had a much smaller and less globalised financial market and more direct transmission of monetary policy to the real economy through bank lending. Today, capital can move around freely to wherever it can find the best opportunities, and businesses can refinance themselves outside the traditional banking system all of which reduces the impact of monetary policy on the real economy.

In short, I find the results the research shows for higher inflation rates wholly unusable in today’s environment. And that this is not mentioned as a major shortcoming in the paper tells me that the researchers don’t think it is an issue. Or that they haven’t thought about it. Or that they don’t know what drives inflation and are just taking a stab in the dark hoping to find something, anything.

Inflation and the latest rate hike cycle by the Fed

Source: Panmure Liberum, Bloomberg

Can we even discuss recent US inflation without taking in account the massive fiscal input? Making it indeed once a gain a 'different time'. Add the fact that many CFO's and households locked in low rates for their debt, mortgages etc before the event, while the high rates of the past few years are actually a boon to those with access to assets i.e. to a degree high rates are stimulating the economy instead of beng the supposed break to it...

Part of me thinks that modern monetary policy is a magic trick. Let's all pay attention to this relatively inconsequential interest rate policy, while in the background the real work is done by QE as central banks hand out the dough to their cousins wife's mother who runs this or that massive bank.