Technology does not make squirrels less important

Technology does not make squirrels less important

Mark Zuckerberg is reported to have said “A squirrel dying in front of your house may be more relevant to your interests right now than people dying in Africa”. That may be true of squirrels in distress, but surely, when it comes to business news, which is available almost instantaneously worldwide, this news is incorporated into share prices by global and local investors at the same time.

There is a well-known local bias, i.e. the tendency of investors to invest predominantly in companies located near the investors’ home. This is essentially the sub-national form of the home bias, which describes investor bias toward investing in companies in their home country.

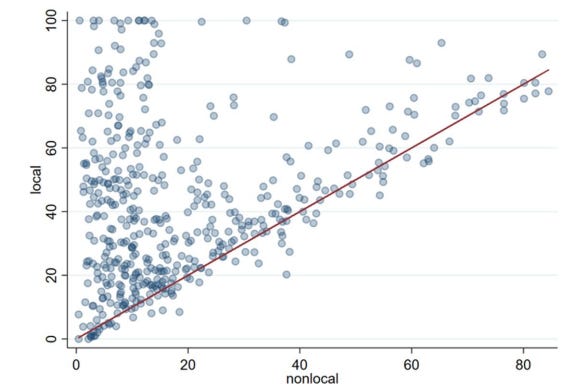

Of course, these local investors also pay more attention to earnings reports and other news of local companies, as Stefano Mengoli and his collaborators have shown. Google searches for a specific company are much more common for local investors than nonlocal investors as the chart below shows.

Google searches for companies by local and nonlocal investors

Source: Mengoli et al. (2024)

When a company releases earnings, local investors react much stronger to the news flow than nonlocal investors. Similarly, if a company has major operations in a specific US state where it is not headquartered (e.g. Boeing in Washington and around Seattle) local investors in that state also pay more attention to news from these companies than investors elsewhere. In terms of size, retail investors pay more than twice as much attention to local firms than nonlocal firms.

But what is really interesting is the time distribution of this attention. Again, using Google searches as a proxy for the attention investors give to each company, the researchers could show that local investors digest information from a company about one to two hours before nonlocal investors. And no, this has nothing to do with time zones as the same lag can be seen between local and nonlocal investors in the same time zone in the US.

But if the average local investor has about an hour’s head start to nonlocal investors, that opens up the possibility to make money. As news from a company gets disseminated in the market, the share price drifts. And while it drifts quickly at the start, this drift continues for hours, and sometimes for weeks and months as documented in the research on post-earnings announcement drift.

Indeed, the new research shows that local investors have a slight informational advantage and on average make a tiny bit of profit from digesting information from local companies faster than nonlocal investors. This in turn means that sophisticated investors (i.e. hedge funds) can do the opposite and focus on companies with a relatively small and retail-dominated local investor base (e.g. businesses headquartered in rural states in the US with fewer finance professionals in them) and front-run the information processing of nonlocal investors to make money.

Once again, Klement comes through and shared another fascinating scientific study we probably all would've otherwise missed.

It's always interesting to see when "conventional wisdom" on the local information edge we always suspect exists is supported by data. Living in and around a "company town" clearly has to present opportunities to assemble lots of little pieces of non-material, non-public information into a mosaic that reveals a larger truth.

That said, I wonder if this exploitable "home field advantage" will hold or not. As public markets have globalized, an odd situation has emerged where many German, French, other European, and Asian companies now issue earnings releases and hold management calls exclusively in English, often shifting the latter to accommodate US investors' time zone convenience, leaving local investors to (ironically) have to translate stuff back into the local lingo, and then watch the stock flail around on local exchanges around for six-eight hours or so pending further information.

Sadly, over time this might actually dissuade locals from investing locally, as they start to feel even their "local champions" are now only catering to a fan club of which they no longer feel they're members :-(