When brokers go under, every investor loses

When brokers go under, every investor loses

All over Europe, the introduction of MiFID II rules had significant unintended consequences. One of them is a significant decline in market liquidity since 2018, particularly for small- and mid-cap stocks. The regulation has contributed to a doom loop where brokers made less money from trade execution and research, which in turn meant that more brokers stopped making markets in smaller companies or even disappeared altogether. But this triggered even less liquidity in markets since fund managers became more reluctant to invest in less liquid markets or trade much in these stocks.

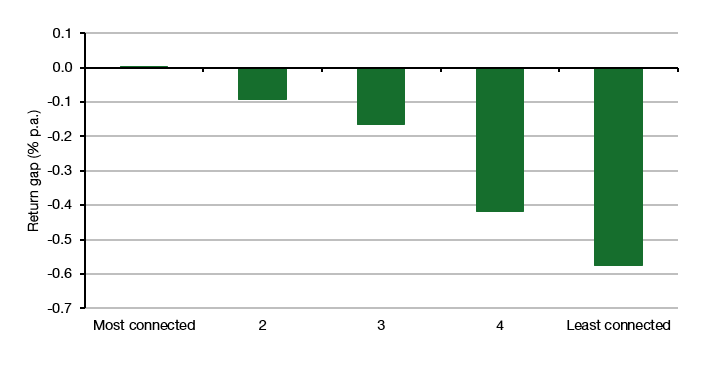

A paper in the Review of Financial Studies examined the impact of the links between brokers and mutual funds on fund returns. They found that mutual funds that are more central in a network, i.e. that have more connections to brokers, had lower execution costs and lower return gaps to an ideal portfolio.

Return gap for mutual funds with differing numbers of connections to brokers

Source: Han et al. (2024). Note: Return gap = loss of mutual fund return vs. ideal execution with no slippage between trade order and trade execution.

Similarly, brokers that had more connections to different mutual funds could execute trades cheaper and more efficiently with less slippage because they were better able to find buyers for sales orders and sellers for buy orders. In particular, more connected brokers could better match buy and sell orders internally and find buyers and sellers that have no publicly announced buy or sell orders.

This is nothing new. After all the job of brokers is to help match buyers with sellers and provide liquidity to a market. But if brokers go under or reduce their market-making activities, mutual funds have a harder time finding counterparts for their trades and pay for that with increased slippage. And this slippage becomes so large that mutual fund managers stop trading and investing in stocks that are too illiquid. And so, the doom cycle begins…

The study shows that most funds are adversely impacted by this effect as the chart above shows. Only the best-connected mutual funds that have broker relationships with practically all the main houses don’t feel the loss of liquidity. Boutique funds and specialist funds that don’t have open lines with every broker suffer more and they have a higher incentive to withdraw from trading in less liquid stocks.

What this means in the end is not only that investors have lower returns due to higher slippage in trade execution, but that markets become gradually less efficient for all but the largest companies. And that is a bad thing for investors and the economy overall because it reduces access to capital and with it the ability of businesses to invest and create jobs.

This looks positive for PE players picking in the small & mid-cap space.

Those institutions housing broking and mutual fund businesses under the same roof are the winners. The loser: competition and the fabric of the overall market.