A flashback to the days when I studied for the CFA exams

Normally, I don’t comment on individual stocks, because I am not an equity analyst and there are plenty of people out there who can do a much better job than I do. Having said that, I find myself writing about an individual stock for the second time this week. This time, it was Aston Martin Lagonda that caught my eye.

I’ve been a petrol head all my life and one of my lifetime dreams was to one day own an Aston Martin. Alas, while I have driven their cars before, I will likely never own one myself. But instead, I might buy the next best thing, namely a share in their company. The company had its IPO in October last year, but the offering seemed to be troubled from the beginning. Days before the IPO, the company had to reduce the top of the price range from £22 per share to £20 per share and eventually floated at £19 per share – just to drop to £17.75 per share on the first day of trading.

But looking back today, I think there are many investors who wished they would have sold back then, because since then, the share price has dropped 72.5%, while the share price of the closest competitor, Italy’s Ferrari, rose 22.5% and the StoXX Europe Automobiles & Parts Index dropped 10.6%. This chart reminds me of an old joke amongst investors:

“What is a stock that dropped 75%?” – “A stock that halved in price, then you bought it because you thought it was cheap and then it halved again.”

Share price of Aston Martin, Ferrari and the StoXX Europe Automobiles & Parts

Source: Investing.com. Note: AML = Aston Martin Lagonda (blue), RACE = Ferrari (red), SXAPEX = StoXX Europe Automobiles & Parts (grey).

There are many reasons why Aston Martin shares were such an abysmal investment, not least the fact that the company issued a profit warning a week ago and published big losses in their results for the first half of 2019 yesterday. Apparently, their clients in Europe are reluctant to buy a new car as the economy slows down.

With the massive losses piling up throughout 2019 so far, the company now has to hope that the new Vulcan supercar and the DBX SUV, both of which will be launched in 2020, will become big hits and boost the low profitability of the company. Unfortunately, though, the company builds its cars in the UK and a hard Brexit would seriously damage the sales outlook for their cars in 2020. In essence, Aston Martin seems to have become the Tesla of luxury cars – never profitable and always banking on the hope that the launch of the next model will bring the turnaround.

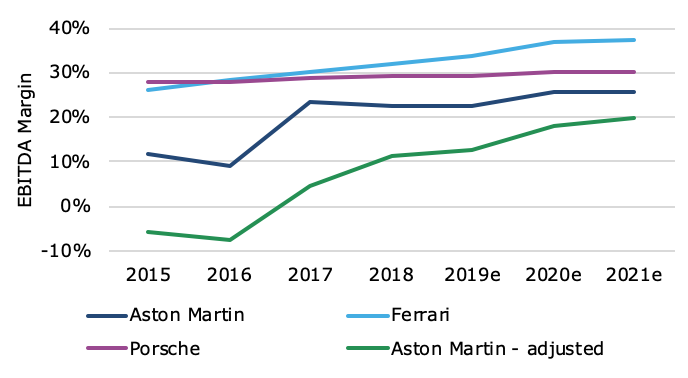

What worries me most about Aston Martin, though, is not the company itself, but how easily investors were convinced that the company was profitable. As the analysts at Bloomberg write, Aston Martin capitalizes 95% of their research and development (R&D) expenses on their balance sheet, while competitors like Ferrari and Porsche only capitalize 40%. The result of this accounting trick is that the profit margins of Aston Martin look significantly better, though they remain still below their competitors. The chart below shows the EBITDA margin of Aston Martin, Ferrari and Porsche as reported and the EBITDA margin Aston Martin would have reported, had they capitalized only 40% of their R&D expenses like their peers. With the lower capitalization rate, Aston Martin would have reported losses in both 2015 and 2016 and only a small profit in 2017. But of course, that is not what you want to show if you plan to offer your shares to the public.

EBITDA Margins in comparison

Source: Bloomberg Intelligence.

Capitalizing expenses like Aston Martin did results in shifting future profits to the present, one of the oldest accounting tricks in the book. When I studied for my CFA exams many moons ago, the book “Financial Shenanigans” by Howard Schilit was part of the curriculum. By now it is in its fourth edition, but I had to read the second edition. In the chapter called “Shenanigan No. 4: Shifting Current Expenses to a Later of Earlier Period” he even has a box that warns readers: “RED FLAG – Watch for changes in capitalization policy just before the IPO” and in the text he states:

“Investors should be alert for companies that capitalize a disproportionately large amount of their costs or companies that change their accounting policies and begin to capitalize costs.”

How many CFA charter holders and professional investors have looked at the shares of Aston Martin and ignored this red flag? According to Bloomberg, of the 10 analysts that cover Aston Martin, 5 have a buy recommendation on the stock, 4 a hold and only one analyst continues to rate the stock as a sell. The most optimistic analyst has a price target of £16.80 per share on the stock and that price target was re-affirmed in mid-July. Note that the current share price of Aston Martin is £5.928, so that price target equates to an upside of 183%.

The funny thing is that several of these analysts are CFA charterholders and one of the most optimistic ones in the sample passed his CFA exam the same day that I did. So, this guy must have read through the same curriculum. But as I said before, most people these days don’t read anymore. This has become so bad, even amongst professionals, that reading has become a competitive advantage for investors. The result is that companies can continue to engage in the same shenanigans they engaged in ten or twenty years ago and the analysts who examine the shares won’t call them out and the investors keep buying into the bs of these companies.