A survey of voting intentions

No, I am not talking about one of the many political elections in 2024 but about a survey of institutional investors and why they vote for or against issues at general meetings.

Roni Michaely, Silvina Rubio, and Irene Yi examined why institutional investors in the US and Europe voted on specific issues using a dataset of 611,389 voting rationales between 2014 and 2021 published by these investors.

While 600,000 rationales sound like a lot, we have to state that this accounts for only a small fraction of all votes cast. Only 5.4% of all institutional shareholder votes were accompanied by a publicly available rationale in 2021, which is up a lot from the 1.4% in 2014, but still amounts only to one in twenty votes. Providing a public explanation why an investor has voted one way or another is even rarer in the US, where only 2.4% of votes came with a rationale, compared to 11.2% in the UK, 10.5% in the Netherlands, or 5.7% in France.

Nevertheless, the analysis of these explanatory notes allows us to identify what institutional investors find most important to vote on (in particular what topics they tend to object to most commonly because voting rationales are more common when an investor rejects a proposal).

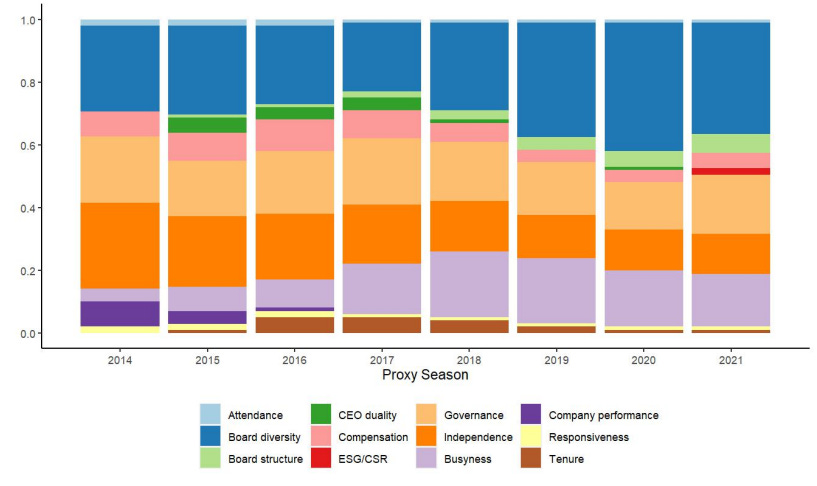

The chart below shows the results for US institutional investors. Board diversity has become the most important topic in recent years but was among the top three topics in 2014. A lack of diversity (both in terms of gender and ethnic diversity) is one of the most common reasons why US institutional investors reject a candidate for the board of directors. The issue that used to be the most important issue was the independence (or lack thereof) of board candidates. After Sarbanes Oxley was introduced in 2002 the issue of board independence became much more of a focus and it has remained so to this day, though the relative share of independence issues has declined over time.

Meanwhile, the other two issues that seem to be very important to US institutional investors are governance issues in general and the busyness of directors. US institutional investors tend to get worried when directors have to juggle too many mandates at the same time and can’t focus enough on their job.

Shareholder voting intentions of US institutional investors

Source: Michaely et al. (2023)

In Europe, other topics tend to dominate voting rationales. Yes, the independence of corporate boards is a key topic but just like in the US its relative importance is declining. Meanwhile, the busyness of directors is less of an issue. Instead, European institutional investors focus more on board tenure. They don’t like to see directors who have been on a board for too long.

And they really don’t like CEOs with a dual role as Chair of the board. CEO duality is a much more common objection by European institutional investors than in the US. Diversity, on the other hand, is less commonly quoted as a rationale to vote against a director candidate – possibly because companies in Europe already are subject to legal diversity requirements in many countries. Note also that general governance issues are less commonly mentioned as a voting rationale by European investors than by US investors.

Shareholder voting intentions of European institutional investors

Source: Michaely et al. (2023)

Overall, the relative focus in Europe seems to be less on the diversity and busyness of directors and more on enforcing increased board independence by preventing CEOs with a dual mandate or allowing directors to become too chummy with the executives after long tenures.

And these institutional investors manage to enact change with their votes. Shareholder votes are notoriously lopsided making the election outcomes in dictatorships look pluralistic in comparison. But even though most shareholder votes get accepted with more than 90% of the votes, objections by institutional shareholders matter. Using the voting rationales as a tool to check if dissent matters, the researchers could show that two years after institutional investors objected to certain dimensions at shareholder votes, the company did significantly improve its governance issues in these dimensions to accommodate the criticism of investors.