A waste of time and money

I am no fan of influencers. The last time I wrote about them I got some stick for calling them talent-free people with fewer brain cells than the money I have in my bank account. Maybe that was a bit harsh. So, let me revise my opinion based on a new study on the performance of the recommendations of financial influencers: They are a waste of time and money.

The authors of the study looked at financial influencers, or ‘finfluencers’, on StockTwits from 2013 to the start of 2017. Based on this database, they identified close to 30,000 users making stock recommendations. The chart below shows the average alpha of these recommendations in the 20 days after a recommendation was made. Because the vast majority of finfluencers make trading recommendations, it makes sense to look at such a short investment horizon of just one month.

20-day alpha of stock recommendations

Source: Kakhbod et al. (2023)

The chart splits the recommendations by skill level. On average, investors underperformed the market by 0.35% per month (4.1% annualised) if they followed the advice of these finfluencers. Yet, there is a minority of finfluencers that add value. The top 25% by performance managed to outperform the market by some 1.9% per month or 25% annualised. However, the distribution is skewed towards underperformance with the bottom 25% of finfluencers underperforming the market by 29% annualised.

Indeed, the authors find that 28% of finfluencers are skilled in the sense that they generate positive alpha, while 16% are unskilled inasmuch as their alpha is no different from zero. But wait, I hear you say (ok I don’t hear you say that, but bear with me), there are 56% of finfluencers missing. The study found that these 56% of finfluencers have ‘antiskill’, i.e. their recommendations have a statistically significant negative alpha.

This means that if a user randomly follows finfluencers, she is more likely to follow a finfluencer with statistically significant antiskill than an unskilled or skilled finfluencer.

But of course, users of StockTwits or any other social media platform don’t follow influencers randomly. The hope is that users are able to differentiate between finfluencers that add value and those that don’t so that skilled finfluencers get more followers.

Yeah, right.

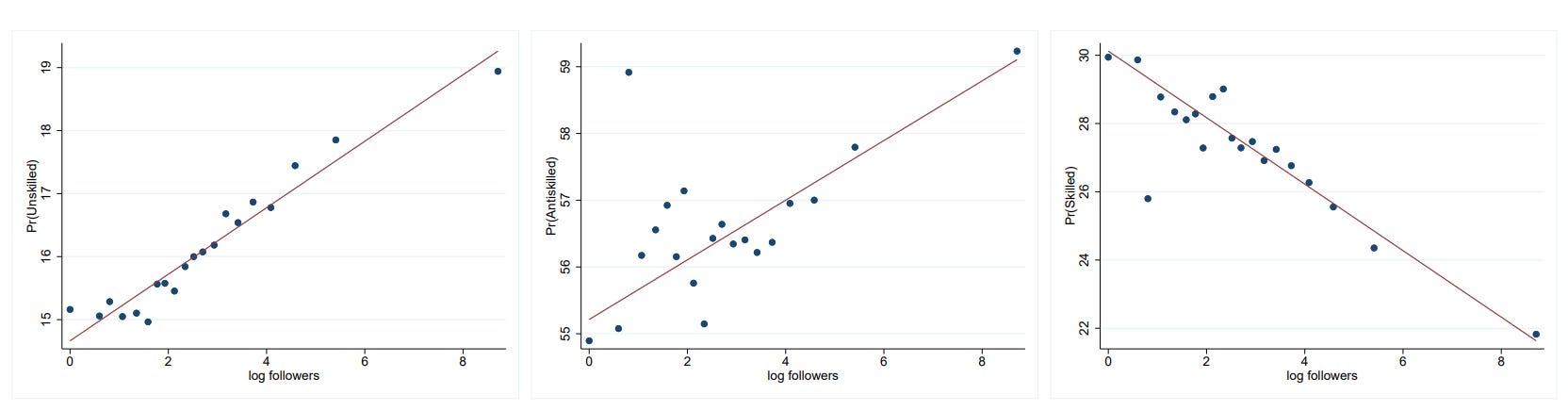

The charts below show the relationship between the number of followers for unskilled (left chart), antiskilled (middle chart), and skilled (right chart) finfluencers and the probability that these finfluencers are truly skilled, unskilled, or antiskilled.

Skill vs. followers

Source: Kakhbod et al. (22023). Note: Unskilled finfluencers on the left, antiskilled in the middle and skilled on the right.

Note how the unskilled and antiskilled finfluencers with the most followers are far more likely to be unskilled or antiskilled (i.e. their recommendations are more likely to destroy performance) than finfluencers with fewer followers. Meanwhile, skilled influencers with more followers are less likely to have truly positive alpha than finfluencers with fewer followers. To put it bluntly, the worse their recommendations are, the more followers finfluencers tend to have.

According to the study, what happens is that users tend to follow influencers that ride return and social sentiment momentum, i.e. they egg users on to act on their emotions and their pre-existing beliefs and act as amplifiers rather than serious advisers. Whether it is gold bugs and crypto bros that claim the world is going to end or HODLers who think that Tesla shares can only go up (remember the data is from 2013 to 2017 when crypto became big and Tesla was the ultimate hype stock) finfluencers most easily increase their influence and follower count by actively encouraging users to do what they already wanted to do. Finfluencers create an echo chamber that removes competition and insulates them from questioning performance or the validity of their beliefs. The unfortunate thing, though, is that markets don’t care about a person’s belief, which is why finfluencers are so destructive and a waste of time and money.

In my time at a long-only asset manager, I was often frustrated at how consultants and other fund selectors will wait until a fund has a strong 3-5-year track record before recommending their clients buy it, only to (as probability and statistics would imply) watch it miserably underperform. Why not set up a consultancy that recommends the *worst-performing* funds of the prior year ... assuming, of course the long-term track record was sufficiently positive to demonstrate that the fund managers were in fact skilled stock pickers? Seems really straightforward ... but nobody does it.

Apropos your thoights, the much-maligned Jim Cramer on CNBC became so hated for underperforming stock picking https://en.wikipedia.org/wiki/Jim_Cramer#Controversies , that an ETF called "Inverse Cramer ETF" was launched https://alts.co/inverse-cramer-etf-performance-and-holdings/ ... only to eventually shut down https://finance.yahoo.com/news/inverse-jim-cramer-etf-shuttered-140000106.html "Cramer makes a multitude of calls, so deciding which ones to bet against—and when to close those inverse bets—takes discretion. In other words, even if it’s the case that Jim Cramer is a bad stock picker, the sheer number of calls he makes and the speed at which he shifts gears makes it difficult to devise a repeatable blueprint for betting against him."

So the secret to success appears to be "you can't dazzle them with brilliance, baffle them with bullshit" ;-)

Question: The study covers 2013-2017 a period of upward trending markets with very little volatility. How did these influencers perform at the during the downturn at the end of 2018 or during the pandemic panic in 202o or the Fed induced bear market from Jan 2022 to Oct 2023? It would be interesting to see how they fared during difficult times as opposed to good times.