A watershed moment for bond yields

As I write this, we are coming out of a period of several months when 10-year government bond yields in the US, Eurozone, and UK have risen sharply despite central banks trying to cut interest rates. There are all kinds of drivers behind this development like higher than expected inflation, stronger than expected jobs data and other. But these missives aren’t about current market events but designed to take a step back and look at the bigger picture, so let’s do that. How has the trend in long-term bond yields changed? And what does that say about government financing costs and long-term bond yields in the next couple of years?

Martin Ademmer and Jamie Rush from Bloomberg have done an exceptional job in modelling the trend in real 10-year bond yields over the last 50 years and – crucially – disaggregating this trend change into different drivers. They built a large VAR model that covers 12 advanced economies and all drivers of long-term real bond yields typically discussed in markets and the academic literature:

Trend GDP growth: Trend growth is mostly driven by productivity gains and changes in the labour force. Faster productivity growth increases the return on capital and thus the natural rate of interest because government bonds have to compete with higher returns available in equity markets and other asset classes. Similarly, if the labour force grows, more capital investments are needed to employ them, creating a larger demand for capital and thus pushing real bond yields higher to make government bonds more attractive relative to other investment opportunities.

On the other hand, if the relative price of investment goods like computers and machinery declines, the need for capital investment drops as well, creating downward pressure on real bond yields.

Demographic trends: As the population ages, the savings rate declines because pensioners save less than working-age people. As savings rates decline, the real rate of interest must rise to attract more investments.

Income inequality works in the opposite direction of an aging society. Higher earners tend to save more, hence, rising inequality creates downward pressure on real bond yields.

The global balance of supply and demand for safe assets. On the one hand, government supply of safe assets has increased over time, but so has global demand for safe assets, particularly as emerging markets like China and India became wealthier. If the increase in demand outstrips the increase in supply, real bond yields drop and vice versa.

Beyond this global balance of supply and demand, there is a separate effect from rising indebtedness of governments. As government debt piles increase there is increased competition for domestic savings vs. other asset classes like stocks or corporate bonds. To attract the limited pool of domestic savings, real bond yields must rise if government deficits remain large.

Changes in regulation for banks, pension funds, insurance companies, etc. might create additional demand for government bonds which reduces the real bond yield. This is expressed as a rising convenience yield, i.e. the premium paid for being able to hold safe and liquid assets like government bonds.

Taking all these factors into account, here is how the natural rate of interest (expressed are 10-year real government bond yield) has changed in the US.

Change in the US natural real long-term rate

Source: Ademmer and Rush (2024)

In the 1970s the real bond yield was c.5% but has declined to less than 2% in the 2010s. The key driver for this decline in real bond yields was slowing trend growth both in the US and globally. The decline in trend growth in the US alone reduced the trend real bond yield by one percentage point. Another percentage point drop came from the global decline in trend growth.

The second most important factor driving trend real bond yields lower were demographic trends. The aging population structure in the US reduced trend real bond yields by more than 0.6 percentage points since the 1970s. Globalisation, which reduced the costs of investment goods like machines and computers reduced trend real bond yields by another 30 basis points. In a sense, globalisation helped reduce our mortgage rates.

But most importantly, note that the trend real bond yield has started to increase again since 2015. And there are two crucial factors that drive this increase in real bond yield. The increasing deficits of governments and the shift in the global balance between supply and demand for safe assets have both pushed up real bond yields.

This is a watershed moment, we are witnessing here. For the first time in the last 50 years we see evidence that bond markets are demanding a ‘risk premium’ for US Treasuries because supply outstrips demand.

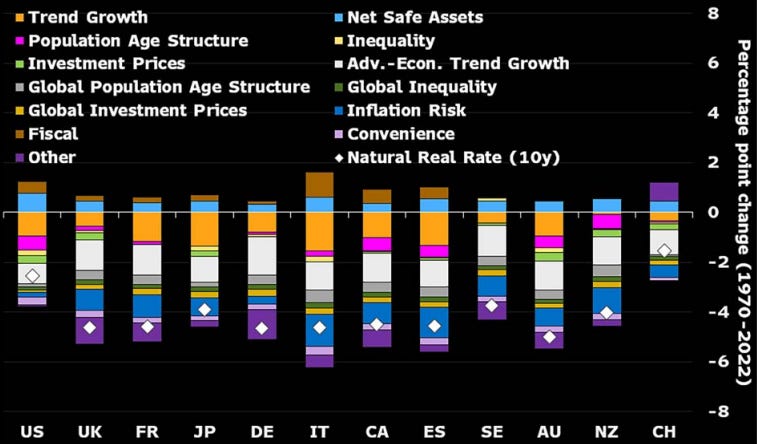

Crucially, this increase in trend real bond yields due to excessive government deficits is a global phenomenon. Here is the total change in trend real bond yields since 1970 across the 12 advanced economies covered in the study.

Change in the natural real long-term rate across 12 advanced economies

Source: Ademmer and Rush (2024)

Note that the US suffered the second largest increase in trend rates due to rising deficits and an oversupply of safe assets. Only Italy has seen a larger contribution from these two drivers. Meanwhile, Germany saw the smallest increase from these two factors, but Australia and New Zealand have also done quite well.

I cannot stress enough how important these results are if confirmed by other independent research. Bond markets are starting to demand a rising risk premium to compensate for the excessive deficits. These are thoroughly new developments that we haven’t seen until about 2015 to 2020 and they could change the entire dynamics of bond markets and government finances.

So far, there is no need to panic. After all this is just one model and one piece of research. But add to that the other results we have seen in 2024 (see here) and you can see how the balance of the evidence is shifting.

These dynamics will surely also feed into the risk asset complex too and lead to greater heterogeneity in asset returns. No?

Excellent, must-read analysis, thank you very much.

We had almost cracked the code, didn't we?

Clintonism (as I perceived it): fiscal prudence made electable by Sista Soulja-populism + globalism (=cheap imports) --> lower interest rates = higher economic growth = lower deficits = circulus virtuosus.

James Carville was complaining about the dictorship of the bond market when he said that's what he'd want to be re-incarnated as, but I think it was in essence a kneefall.

Now, we might be in a malevolent cycle. Maga (possibly): Voodoo Smoot-Hawley economics made electable by demagogic populism --> higher inflation --> higher interest rates which make the deficit untenable --> bond market loses confidence in US Treasury --> higher interest rates...

Funny thing is, Trump was a buddy of Clinton back in the day.