About that velocity thing

A week ago, I wrote about how monetarist theories of money have been violated empirically and how we really don’t know what drives inflation. And as happens always when I write something against monetarist theories of inflation or the quantity theory of money, I got a lot of replies by readers saying: “But what about…”. Last week, the unison refrain was: “What about the velocity of money?”. So, in this post, I want to address these arguments about the velocity of money.

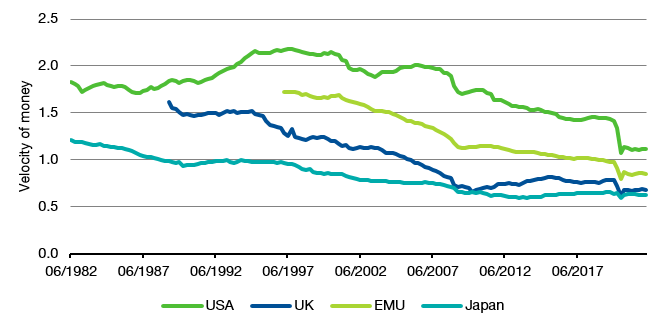

First, a little bit of history. Irving Fisher created the wonderful concept of velocity of money through an accounting identity in 1910: P * Y = M * V. I apologise for the formula, but in this basic equation, P is the price level of goods and services in an economy, Y is the economy’s output, M is the monetary base (i.e. how much ‘money’ is in circulation) and V is the velocity of money (i.e. how fast money is changing hands). Originally, the velocity of money was thought to be constant but well, the chart below shows that that assumption doesn’t work out that well in real life.

Velocity of money

Source: Bloomberg. Note: Velocity of money based on M2

Since the 1980s the velocity of money has been on a secular decline and during the financial crisis and again in the 2020 pandemic it fell off a cliff and never really recovered. There is a lot of speculation what causes this decline in the velocity of money, but the main argument I am making is that the velocity of money is not constant and in fact on a secular decline. Readers of my post last week argue that once this effect is taken into account, the quantity theory of money holds again and an increase in the monetary base leads to higher inflation. Furthermore, some (not all) argue that the velocity of money will rise in coming years triggering a persistent rise in inflation.

My argument is that while the velocity of money is currently very low, I know of no reason why the velocity of money should revert its structural decline over the last 30+ years. In fact, I have written here that monetarist theories of inflation have stopped working more than 30 years ago and trotting out the arguments of Milton Friedman is like trying to ride a dead horse. As a practitioner, I don’t think a theory that has stopped working a generation ago is one I should rely on in my quest to understand the economy. As one of my mentors used to say: “Truth is what works and not what your theory says”.

Some readers have argued (rightfully, I might add) that the growth in the monetary base is not necessarily the right number to compare with inflation. Instead, one needs to compare excess growth in the monetary base above real economic growth with inflation. So, in the chart below, I have done just that and compared broad money growth in the UK minus real GDP growth with inflation. Again, to make long-term trends visible, I have calculated a rolling 10-year average.

Excess growth in monetary base and inflation in the UK

Source: Macrohistory, Bank of England, Bloomberg

The chart shows data for the UK, but the US looks essentially the same. One can clearly see a close link between excess money growth until about the 1970s and a regime change sometime between 1980 and 1990 when the relationship becomes much, much weaker. Coincidentally, or not, this is the time when central banks started to target inflation directly instead of targeting the monetary base and globalisation became a major economic force allowing investors to send their money to wherever they wanted to in the world.

We can zoom in into the last 42 years and switch to quarterly data for that time period. In order to make the comparison as charitable for monetarists as possible, I have reduced excess money growth by 2% per year to take into account the secular decline in the velocity of money and shifted the growth in excess money growth forward by 6 quarters, since Milton Friedman predicted this lag between monetary base growth and inflation. Overall, there is some weak resemblance between the two lines, but deviations are significant and can last a decade or longer. The relationship has been particularly poor since the financial crisis 2008.

Excess growth in monetary base and inflation in the UK

Source: Bank of England, Bloomberg

In summary, my opinion about the quantity theory of money and monetarist theories of inflation is that they are nice models you can read about in your economics textbooks. Economics professors like to teach them because they are intuitive and seem reasonable. But they are of no practical use because in real life these theories are violated so often and so strongly as to make their application useless.

By the way, monetarist theories are by no means alone in that. The Capital Asset Pricing Model (CAPM) or Purchasing Power Parity (PPP) are similar theoretical concepts that are useless in real life. Either they are violated all the time, or one has to wait ten years or longer for them to hold true, which means in practice that you will have lost an awful lot of money betting on these theories before you make a little bit of profit at the end. These are nice theories to compare with data, but their only use is to identify in what way they are violated in real life.

Now, that is my opinion, but you may say I have no idea what I am talking about. Well, a simple search of the academic literature will show you dozens of papers where the concept of velocity of money and the quantity theory of money have been tested empirically. Three examples from the last couple of years: This study tested the quantity theory of money for OECD countries from 1970 to 2005 and found that for low inflation countries the “relationship is tenuous at best”. Meanwhile, this study tested the quantity theory of money for 40 countries in 2002 and 2014 and found that the predictions of the theory were rejected. And finally, this study looked at 27 countries both from the 18th century and since World War II and noted: “There is little evidence that the relationship had been weaker under commodity standards than it has been under fiat standards. Only for the period since the mid-1980s, which has seen the introduction of monetary regimes in which inflation is directly targeted, the relationship appears to have materially weakened”.

In particular, I liked this quote from the study above: “In recent years, however, a dominant view has taken hold that, in fact, the relationship between money growth and inflation is weak and unstable also at the very low frequencies, to the point that (e.g.) such view features prominently in one of the leading macroeconomics graduate textbooks”.

When I went to university, the quantity theory of money was taught as gospel and the best available theory of inflation. By now, it has been discredited so much that textbooks are starting to teach students not to rely on it. And that, I think is a step forward.

But even so, one can entertain the notion that the velocity of money still might be an important driver of inflation. Today’s post has gone on for too long, but for those inclined to hold on to the quantity theory of money I will spend tomorrow’s post trying to figure out in which direction the velocity of money will go in coming years and what that “theory” would imply for inflation. It’s going to be fun.

Has there been any study looking to see if there’s a link between the velocity of money in an economy vs demographics?

Is the “secular decline” really just a measure of the age of an economies participants and the older savers automatically slow the velocity. Let’s face it Japan is leading the charge.

It will of course be materially more complex than this single factor but is it a C material contributor?

Hi Joachim

The problem may be the measure of Money, this excellent article by Jeff Snider describes the problems of measuring the monetary base in the U.S.

https://alhambrapartners.com/2021/11/15/is-m2-the-money-behind-inflation-if-not-what-is-or-isnt/