An interesting indication of an ESG bubble before the inflation shock

Green stocks had a torrid time over the last couple of years as high inflation and higher interest rates made investments in these growth areas unprofitable. On top of that, ESG investing has gone too far in some areas, due to tons of companies greenwashing their business or engaging in empty virtue signalling. No doubt, the air has gone out of the bubble. But was there a bubble to begin with?

Andreas Barth and Christian Schlag from the University of Frankfurt have creatively tackled this issue. They reason that if ESG investments are made primarily because companies with better ESG credentials have fewer downside risks, then a company that improves its ESG credentials should not only see its equity risk premium drop but also its credit risk premium.

If, on the other hand, investors buy green stocks because they are green and not because they have lower risks, then share prices should rise as ESG credentials of a company improve while credit risk premia do not change.

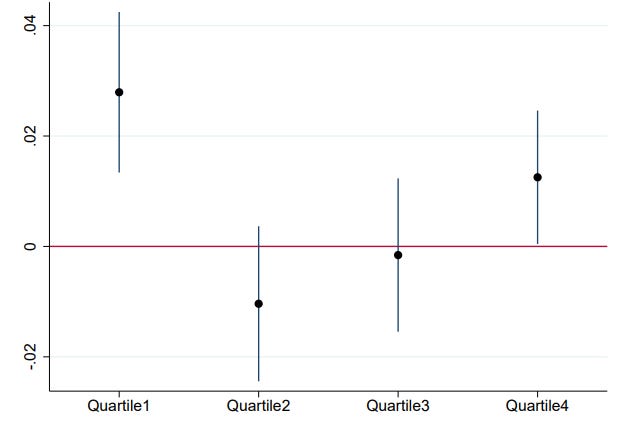

By looking at the behaviour of share prices vs. credit risks as priced in company CDS one can differentiate between one and the other. So, here is what happens to share prices vs. credit spreads for companies sorted by the ESG credentials. Quartile 1 stocks are the companies with the best ESG credentials, while Quartile 4 stocks are the companies with the worst credentials. As you can see, companies with the best ESG credentials saw their share prices rise above and beyond the change in CDS spreads, indicating that these stocks benefitted from being green.

Equity return vs. ESG risk impact

Source: Barth and Schlag (2024)

Unfortunately, the study covers only the years 2010 to 2020 but when we look at this green equity premium over time, we can see that it only appeared in 2017 and wasn’t present before. I guess that today, this equity premium for green companies has disappeared again and today improvements in ESG credentials are only rewarded if they reduce operational risks or reduce the cost of capital, etc. In other words, ESG improvements are only rewarded if they have a provable and tangible impact on the company’s fundamentals.

But that is just my guess. It would be good if the authors could expand their research to include the recent years after the Russian invasion of Ukraine.

Equity return vs. ESG risk impact over time

Source: Barth and Schlag (2024)

In my view 'ESG' performance is highly correlated with operating performance. Good business practice is generally good ESG, so well run companies should - if theory follows - be good ESG companies in most instances. At a fundamental level, ESG (when defined and measured correctly) can't be really be separated from good operating practices. They're both measuring a similar thing, albeit from a different perspective. So for me, it comes back to the 'ESG metrics' used. Are quant ESG screens giving us good outputs? Are these outputs consistent? Can they be easily gamed? My answer to those questions is no, no and yes.

The definition of ESG has been perverted into a sort of measure of wokeness which can be easily gamed, rather than the framework for assessing fundamental business characteristics that it was originally conceived as.

The un-resolved (and probably un-resolvable) point whenever trying to establish a relationsship between ESG and financial performance: Is a company financially successful because they are "good at ESG" (however you want to meassure that) ? Or are they "good at ESG" because they can afford it (are financially successful) ?