Bang for your buck in private capital markets

Most of us can access private markets only via funds managed by professionals. These funds aren’t cheap, but they come with the promise of access to unlisted assets that provide diversification benefits and potentially high returns. As these private investments have become some of the most sought-after asset classes, it is somewhat surprising that there aren’t that many studies out there that do a cost-benefit analysis of these funds. So, I was glad to see the study by Wayne Lim from Harvard land in my mailbox…

Wayne somehow convinced an advisor to institutional investors to share the data of 10,791 private capital funds from around the world with vintage years from 1969 to 2020. This vast database allowed him to analyse different strategies in private capital funds, their returns, and the fees they charge.

For example, he looked at the IRR (an arguably flawed and much-debated metric of investment returns) or the total value to paid-in capital (TVPI, a much less debated and somewhat less flawed metric) to assess the return of these investments for limited partners. Similarly, he looked at management fees and hurdle rates for these funds as a measure of the costs incurred by limited partners.

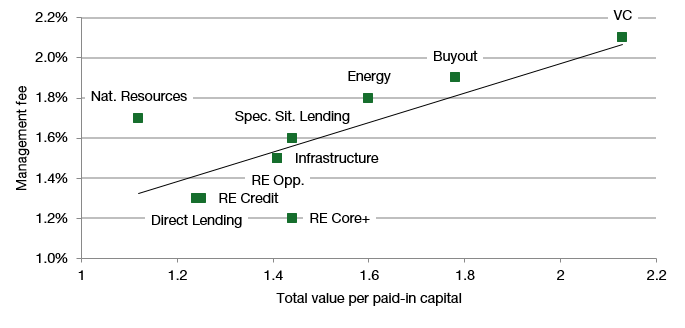

You can splice and dice this data to your liking, but below is a simple way of looking at it. I plot the average management fees of different strategies against the money multiplier (TVPI). One thing that is immediately obvious is that higher returns beget higher fees. Nothing unusual there, that is just how the financial industry works.

Management fees and TVPI of different private capital fund strategies

Source: Lim (2023). Note: RE = Real Estate.

What is interesting to see, though, is that on average more established strategies like real estate show lower fees compared to the average level of return (they drop below the trend line). More exotic strategies like natural resources or energy investments, on the other hand, show higher fees relative to the level of TVPI. This indicates that there is some degree of inefficiency in the market for these private capital funds. As funds become more mainstream, fees are increasingly reduced because more funds compete for the same pool of money.

By looking into the individual funds, other things can be established:

Larger funds on average charge lower fees and European funds charge lower fees than US funds.

Funds with higher fees do not perform better on average than funds with lower fees.

Funds with higher management ownership tend to perform better on average.

Nothing too ground-breaking, but it is good to know that in private capital funds, the world isn’t all too different from what we know in listed markets.

I'm sorry to contradict the Harvard professor - ok not me directly - but an Oxford Professor, Ludovic Phalippou of Private Equity told me on a podcast that the headline figure for private equity is "useless" and "if you combine all of these fees, the average fund we are talking about in private equity gets a fee of about 700 basis points" (at 37min https://youtu.be/WKSWrjssSAM)

Entirely unrelated but interesting for some grumpy middle aged men perhaps, today via the Aporia substack: hope for the social sciences...

'Abel Brodeur and colleagues examine research reliability in economics and political science by attempting to replicate 110 papers in leading journals. They find that 85% are fully replicable. They also find that about 70% are robust to various re-analyses like introducing new data, though effect sizes for re-analyses tend to be smaller than the original ones.'

https://www.aporiamagazine.com/p/does-war-lead-to-norms-favouring?utm_source=post-email-title&publication_id=828904&post_id=144528592&utm_campaign=email-post-title&isFreemail=true&r=6mos7&triedRedirect=true&utm_medium=email#:~:text=A%20New%20Hope.-,Abel%20Brodeur%20and,-colleagues%20examine%20research

The original study (link in article) looks massive but that's the huge amount of material that comes with it. Abstract at page 7, conclusion at p 43. There's still a lot to do and i guess as academia sticks to rewarding production that won't be easily solved:

'Our results suffer from several limitations. To this date and despite some recent progress on the matter, only a small number of economics and political science journals request data and codes (Askarov et al. (2023); Brodeur et al. (Forthcoming)), and a very small fraction check whether the results are reproducible (Vilhuber et al. (2020)).'