China, Coronavirus and the middle income trap

One of the debates about China that I expect will gain more prominence this year will be if China is going to fall into the middle income trap. For those unfamiliar with the term, it was coined by Indermit Gill and Homi Kharas in 2007 in a World Bank paper and describes the observation that GDP growth drops rapidly for some countries, once they have achieved a GDP per capita around $10,000 to $15,000 in today’s money. Classic examples for countries that have been caught in the middle income trap are Argentina, Brazil or South Africa, all of which seem unable to catch up with high income countries despite significant natural resources, increased integration in the global economy and rising human capital due to improving education.

On the other hand, there are countries like Japan, South Korea and Taiwan that managed to avoid the middle income trap and grow from relatively low levels of GDP per capita to levels that are similar to Western Europe and other high income countries.

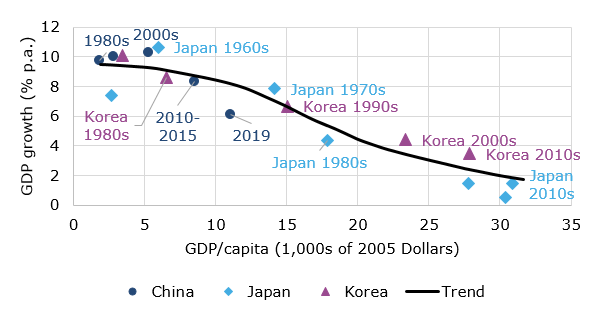

China so far has followed the growth trajectory of both Japan and South Korea relatively closely as the chart below shows. China’s GDP growth, extraordinary as it may seem to many of us in the West, has not been unprecedented. During the 1960s, Japan was as poor as China was in the 2000s and posted annual average GDP growth in excess of 10%, just like China did in the first decade of this century. Similarly, Chinese growth between 2010 and 2015 was similar to South Korea’s growth rate in the 1980s and the decade-long average of Chinese growth in the 2010s was about the same as Japan in the 1970s and South Korea in the 1990s.

Growth in China, Japan and South Korea as they became richer

Source: Ahmed (2017).

However, in 2019, Chinese growth dropped rapidly and it seems as if China’s growth is decelerating faster than it should, given the level of GDP per capita in the country. The meagre growth of 2019 was mostly blamed on the US-China trade war, which may or may not be true. But let’s not forget that in 2018 and 2019, China provided a fiscal and monetary stimulus package that was similar in size to the stimulus provided to the US economy from the 2018 tax cuts. And in the United States, this stimulus easily boosted GDP growth by 0.3% or more.

And now, after a miserable 2019, the Chinese economy is hit by the Coronavirus pandemic which may reduce Chinese GDP growth by another 0.3% or so in 2020, depending on how fast the pandemic can be contained and how effective the record emergency stimulus of the People’s Bank of China is.

It could well be that the trade war and the Coronavirus pandemic are just cyclical phenomena that will quickly be overcome in 2021 and the years thereafter. Or it could be that China’s economy is slowing down faster than we would like to admit at the moment and that the trade war and the pandemic are merely covering a more systemic development.

I don’t know if China is at risk of falling into the middle income trap but I know that investors tend to extrapolate current trends too far into the future. And while one year of weak growth may be an outlier, two years of weak growth form a trend. And that, I fear, implies that China bears will come out of their caves again and argue that the Chinese growth miracle is over, while China bulls will argue that it is just a temporary setback.

In five to ten years we will know the truth but in the meantime, stocks of companies with large exposure to China (think luxury goods, car manufacturers, capital goods, etc.) will be caught in the sentiment swings about China and experience increased volatility as the world tries to figure out the future path of the Chinese economy.