Corruption doesn’t pay, unless it’s no longer prosecuted

I admit, I am ambivalent about bribery. Not about being bribed myself or me bribing anyone. I would never do any of that. But I am under no illusions that there are countries where the only way to get anything done is to pay ‘kickbacks’, ‘incentive payments’, or other forms of bribery.

My personal experience in that area comes from my childhood. Both my parents are from Hungary, and when I was small, we went back and forth between Germany and then-communist Hungary once or twice a year. Inevitably, we would get stopped at the border or by a police car on the road because – well – we were driving a German car with German registration plates. Inevitably, these checks could last for an hour or more. Or they could be ‘expedited’ by conveniently forgetting a couple of Deutschmarks in the documentation you handed to the officer.

Facing these realities, some countries allow their businesses to pay bribes in jurisdictions where this is considered a common or necessary practice. In Switzerland, it was for many years legal for businesses to deduct foreign bribes as an expense and lower their tax liability – though this rule has since been changed.

In the UK and the US, paying bribes is illegal, and the Foreign Corrupt Practices Act (FCPA) allows the SEC to prosecute any company listed on a US Stock exchange (even European ones with ADRs trading in the US) if they paid bribes anywhere in the world. On average, FCPA fines were $150 million per case that the SEC enforced.

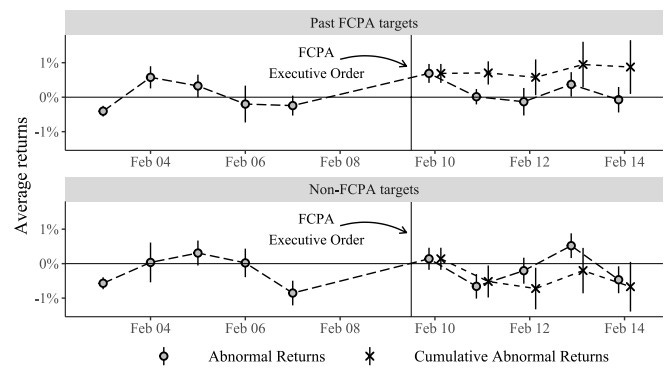

Then came Donald Trump, and in February 2025, he suspended any prosecution under the FCPA and signed an executive order that stopped the enforcement of that law.

Lorenzo Crippa from the University of Strathclyde and his collaborators examined the market reaction to this non-enforcement order. He found that on the day of the executive order, the share price of US companies that had previously been investigated under the FCPA rose by 0.69% more than the average company in the US. The average gain in market cap per company was $160m, eerily close to the average fine imposed by the SEC on these companies in the past.

However, this may not be the result of the market cheering the ability to pay bribes. Instead, it may just be a reflection of the market assessing the impact of lower compliance costs. But if that were true, companies that have never been targeted by the FCPA should have seen their share price rise as well. Yet, on average, the companies that have never been targeted by the SEC under FCPA saw no increase in their share price and a small negative abnormal return in the days following the executive order. And this is hard to reconcile with the assumption that lower compliance costs pushed share prices higher for affected companies.

Abnormal share price reaction to suspension of FCPA

Source: Crippa et al. (2025)

The $160M average gain matching the $150M average fine is the headline but the differential between targeted and non-targeted companies is where the more dangerous information lives. The market drew a map on the day of that executive order. Every company that saw an anomalous gain was being priced as a likely future briber. That map is now embedded in the share price data as a permanent record of which companies investors believe benefit most from the absence of enforcement.

The irony is that the market reaction created the evidence base for future prosecution. If FCPA enforcement is ever reinstated under a different administration, the February 2025 abnormal returns become the obvious starting point for investigation. the companies that celebrated the suspension are now carrying an empirical marker in their own share price history that says "the market believed we would bribe." thats an asymmetric risk the current pricing doesnt reflect because its treating non-enforcement as permanent when its actually a political variable with a four-year half-life at most.

I recall a previously successful company by the name of Petrofac, with a variety of accusations around bribes for contracts in the middle east, which took years to investigate and confirm, during which time it's customers went elsewhere. It may simply be a coincidence that the evidence was supplied and leaked over a very long period of time allowing rival firms to pick up additional business. But we might also speculate on why the regulators allow such a situation to occur, well knowing the damage it causes to individual firms. We can ask whether we assume the only miscreants are on the commercial side of the processes we rely upon to 'regulate' our industries. Does anyone know if there is any correlation between a regulatory career followed by a lucrative retirement consultancy?