Debt debilitates

We all know that most people do not like to hold debt. Some people are more debt-averse than other but in general, people try not to hold too much debt. Personally, the only debt I can get comfortable with myself is the mortgage on my house. I don’t have credit card debt or other consumer debt because that stresses me too much. Indeed, studies have found that debt relief can lead to better mental health and better sleep. Being in debt is not only stressful, but also leads to worse decisions, even if one is just in a little bit of debt.

Alejandro Martinez-Marquina and Mike Shi gave volunteers a series of tasks where they were confronted with a range of savings accounts paying a safe interest of varying degree. The only difference between the setups was that in some cases, volunteers were ‘endowed’ with some debt (accruing interest) and in other cases they were debt-free. Importantly, none of the investments the volunteers could make has any uncertainty around them. The returns were different, but all were guaranteed.

Clearly, this is a simple task. All you need to do is figure out which savings account has the highest interest and put all your money into that account. If you have debt, the situation becomes slightly more complicated. If the savings account with the highest savings rate has a lower interest than your debt, the best move is to first pay back the debt and then invest the rest into the savings account with the highest savings rate. If the highest available savings rate is higher than the highest interest on debt, it is best to use that leverage to your advantage and invest all your money into the savings account with the highest savings rate, independent of how much debt you have.

Here is what really happened.

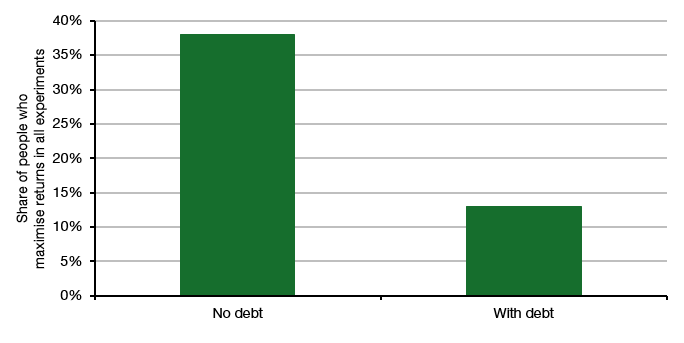

Across several different setups of varying complexity, 38% of volunteers maximised their returns all the time. Most people tried to diversify their investments across different savings accounts, not realising that there was no volatility in the returns and diversification made no sense. But over time, they wised up and put all their money into the best savings account.

Meanwhile, when people had debt (even virtual debt), only 13 % of volunteers optimised their returns all the time. There was the same false diversification going on as in the no debt setup, but something else happened as well. Many people when confronted with debt preferred to pay back their debt before investing the rest of their money even when doing so reduced returns.

On average, people behaved as if reducing debt by $1 was the same as having $1.03 in savings. People are so emotionally distracted by debt that they make bad investment decisions just to get rid of that debt. This can explain why some people enter a devilish debt spiral after just one short time of financial distress. They may have a short-term liquidity problem and go to payday lenders to get a bridge loan. And from there, they slip into more and more debt, even if they could theoretically pay back their loan incl. interest.

Percent of volunteers that maximise returns in all decisions

Source: Martinez-Marquina and Shi (2024)

To a (Significant?) extent attitude to personal Debt is correlated with age. Those of us born just after WW2 lived in a culture which considered Debt ‘a bad thing’. The only loan I had was for house purchase.

Those born in 1970s or later lived in a climate where loans were almost forced on them via credit cards, loans for white goods etc. This may change with those born post 2000.