Do lower rates lead to cheaper mortgages? Kind of

After yesterday’s Fed meeting, the Bank of England will decide on its policy rates today. Investors hope for another rate cut today, and I, for one, am not an independent observer. My mortgage is up for renewal in a year, so I am hoping for rate cuts by the Bank that will lower my mortgage rates by then. But while my mortgage rates may have dropped by then, it doesn’t necessarily mean my mortgage will be cheaper.

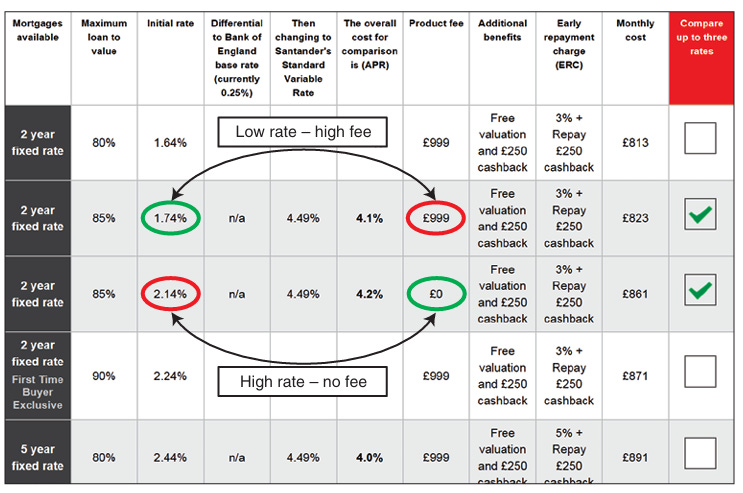

The cost of mortgages is determined essentially by the interest rate charged and the origination fees the bank charges for providing the mortgage. Below is a snapshot of a UK bank's mortgage menu.

A note to my readers in the US: If you are wondering why the mortgages on offer are 2-year or 5-year fixed mortgages, that is how the UK mortgage market works. We can typically only fix mortgage interest for two or five years. If you are lucky, you might get a competitive offer for a 10-year fixed rate, but that is almost unheard of in this country. I wish we had 30-year fixed rates or, at the very least, 10-year fixed rates available, but somehow, banks here are unable to do what they do in the US or continental Europe. Don’t get me started…

The mortgage menu of a UK bank

Source: Benetton et al. (2025)

In any case, the mortgage menu shows that the typical trade-off is between lower interest rates and higher fees or the other way around. When the Bank of England cuts interest rates, the mortgage interest rate obviously starts to drop, as the rate cut on the short end of the swap curve filters through to longer maturities. But that, of course, means that banks make less money with mortgages.

And where would we end up if banks would make less money? So, banks try to compensate by increasing their origination fees for new mortgages. After all, that fee is largely made up anyway, so how will any customer check whether the fee is justified?

Matteo Benetton, Alessandro Gavazza, and Paolo Surico analysed the development of mortgage rates and fees charged by banks in the UK after the introduction of the ‘Funding for Lending Scheme’ (FLS) by the Bank of England in 2012. The goal of that policy was to provide cheaper loans to homebuyers when the Bank Rate was essentially zero, but the UK housing market struggled to get out of the crisis of 2007-2009.

The left chart below shows that after the introduction of the FLS, banks lowered their mortgage rates more aggressively for customers who chose a mortgage with fees than without fees. Meanwhile, they increased their fees by about £100 in the two years after. The idea was to incentivize customers to move into fee-generating mortgages and then charge them higher fees.

The chart on the right shows that it worked. The average house price in the UK continued to rise after the introduction of the FLS, but the interquartile difference between cheap and expensive homes also increased as expensive areas like London benefited more from the Bank’s promotion of cheaper mortgages.

FLS and market outcomes

Source: Benetton et al. (2025)

And some of these banks were bailed out by the taxpayer during the GFC so we’re paying the banksters twice. Last time I checked the banksters still owed taxpayers £400m+.