Does SFDR matter for fund managers?

In March 2021, the EU introduced the classification of investment funds according to articles 8 and 9 of the Sustainable Finance Disclosure Regulation (SFDR). In an effort to fight greenwashing, funds that claim to be ESG compatible must declare themselves to be either aligned to article 8 or article 9 of the regulation. Article 9 poses a particularly high hurdle because it requires a fund to show that it puts ESG impact at par with the goal to achieve high returns. Meanwhile, article 8 provides a much lower hurdle essentially saying that fund managers must document how ESG criteria influence their investment decisions as one set of criteria amongst others.

The broad scope of article 8 has led to a large number of funds in the EU claiming to be ESG funds in accordance with article 8 even though they effectively didn’t change their investment process when they reclassified themselves as article 8 funds nor do ESG criteria play any meaningful role in the investment process. To which Morningstar in February essentially said: “Nice try, but we will not consider these funds as article 8 funds in our database.”

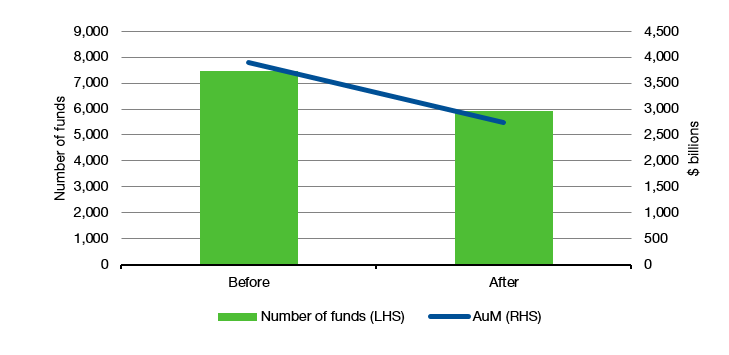

The result is that Morningstar culled its list of article 8 funds by 1,527 funds managing $1.15tn in assets among them. Here in the UK, Terry Smith’s Fundsmith fund which manages £27bn in assets has been the most prominent victim of that cull, which is somewhat fitting because Terry Smith not too long ago publicly chided Unilever for focussing too much on ESG and not enough on profitability.

Morningstar’s reduction in article 8 funds

Source: Morningstar

Terry Smith probably won’t care too much about the loss of that article 8 designation because he is such a prominent manager that he won’t lose any assets over this. But should his less prominent fund manager peers worry?

According to a new study by researchers from the University in Giessen in Germany, they probably should. Because the SFDR only affects EU funds, they could compare European funds with their “closest peer” in the United States in terms of holdings and investment style. First, they checked if a fund in the EU that was classified as an article 8 fund increased its holdings in sustainable investments. And indeed, on average, funds classified as sustainable increased their investments in green and other sustainable stocks. This of course may have unintended consequences since it creates additional demand for green stocks that may lead to excessively high valuations in these companies and eventually an ESG bubble.

But of mor immediate concern is the fact that funds that were classified as article 8 funds experienced a substantial increase in inflows from investors in the order of 0.5 percentage points per month. If a fund was classified as article 9 fund with its more stringent criteria, it experienced a somewhat higher flow increase of 0.6 percentage points per month. Which tells us that the funds that have been stripped of their article 8 designation by Morningstar either need to up their game in order to regain that classification or face missing out on some investor flows.