Energising energy producers

Competition is good for business. It forces companies to become more efficient and more productive and it reduces profit margins, often leading to lower prices for consumers. But sometimes it requires outsiders to break into an industry and ‘disrupt’ it to rejuvenate a staid industry. And it seems one industry where this is happening right now is one of the most boring ones: electric utilities.

Utility companies are famously boring. They often have low or no growth opportunities, and operate in stable markets, some of which are heavily regulated and there is little incentive to innovate or increase efficiency. In the past, this often led to underinvestment in infrastructure and high prices for consumers as utility companies were more concerned with paying high dividends to their owners than serving their customers well.

For decades now, the response of politicians has been to deregulate electricity and water markets so that prices fluctuate, and different providers compete with each other to produce at the lowest cost possible. Yet, all too often the result was simply an even bigger underinvestment in ageing infrastructure and even poorer customer service as margins for utility companies declined but owners still insisted on their fat dividends (if you live in the UK, just think of the disaster that are our water utilities).

Enter an unlikely disruptor. Ten, or twenty years ago, if you had asked a private equity manager if they ever considered buying a utility company, they would have laughed all the way to their yacht. Private equity invested in tech, consumer, and maybe industrials, but that was about it. They wanted either an investment with extreme growth potential or a turnaround case.

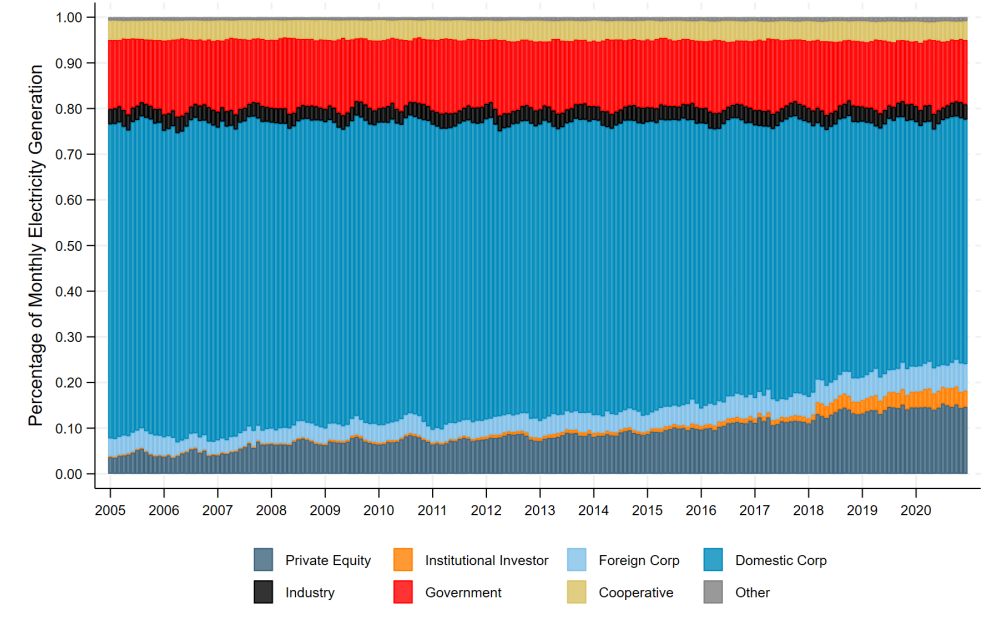

Then along came wind and solar and investment opportunities in deregulated electricity markets that promised significant growth. And guess what, private equity and institutional investors started paying attention. In the last ten years, the percentage of electricity generated by private equity and institutional investor-owned utilities more than doubled. Originally, these outsiders invested mostly in wind and solar but today, they are also a major player in gas power plants.

Ownership and US electricity generation

Source: Andonov and Rauh (2024)

So, how do these newcomers fare compared to established listed US utility companies?

It turns out, much better. A study by Aleksandar Andonov and Joshua Rauh looked at the efficiency and performance of private equity-owned electric utilities and compared them to electric utilities owned by US or foreign listed businesses.

Holding all things equal, private equity firms are much better at running these electric utilities than US listed utility companies. On the one hand, they run the power plants more efficiently, using 5% less fuel per unit of produced electricity than similar power plants owned by listed utilities. They don’t do that by underinvesting in the infrastructure or owning mostly newer plants. The study that private equity owners are just as likely to decommission older plants as utility companies and private equity owners do not operate power plants at a higher intensity. Rather, they invest in the necessary upgrades to make an existing plant more efficient.

And private equity is less risk-averse than listed utility companies. They tend to sell electricity under contracts that are shorter in duration and cover more peak-term periods. They focus on being able to adjust their electricity output flexibly in reaction to prevailing market prices (particularly when running gas power plants), rather than run the power plant at a steady output level. As a result of this dynamic management of output and the more flexible contracts, private equity-owned power plants sell electricity at an average of $2.59 per MWh more than established listed utility companies. This creates higher revenues for the investors in private equity funds investing in electric utilities while at the same time ensuring that there is always sufficient electricity supply available without charging customers more in off-peak hours.

Who would have thought that these private equity guys could teach the establishment a couple of new tricks in an industry like this?

Very thought-provoking. I was always taught that the main rationale behind regulated public utilities was to 1) prevent the sort of chaos that emerged when competing entities all started stringing-up/digging-in redundant infrastructure, and 2) prevent consumers from being price-gouged. The common denominator appears to be when a service becomes "essential" https://en.wikipedia.org/wiki/Public_utility .

Railroads were a capitalist free-for-all https://en.wikipedia.org/wiki/Railway_Mania , literally propelling the Industrial Revolution, but also leaving tons of redundant capacity in its wake. It was largely nationalized, and then slowly privatized, with generally negative outcomes.

Telephony was a regulated monopoly (commonly owned by national post offices) for decades, and most were broken up https://en.wikipedia.org/wiki/Breakup_of_the_Bell_System , However, even though telephone and data backbone infrastructure has remained in flux, requiring continuous upgrades, the consumer is definitely better off than when a three-minute 'phone call from New York to San Francisco cost $500 in 1915. So positive outcomes.

In light of how badly privatization has gone in other regulated public utilities (as you point out, notably water), perhaps electricity generation is a special case. Could that be the result of a more developed and interconnected grid where the technology doesn't really change that much over the decades (other than needing more of it), which might more easily allow investments to be targeted at productive capacity ... even single generating plants?

P.S. I am currently also fascinated by moves on the part of "hyperscalers" now anticipating their massive future power requirements and deciding to invest directly in nuclear power plants themselves https://www.technologyreview.com/2024/09/26/1104516/three-mile-island-microsoft/ and this https://www.ans.org/news/article-5842/amazon-buys-nuclearpowered-data-center-from-talen/ . "Screw it, we need our own power plant!"

P.P.S. If nuclear power hadn't been abandoned, Germany could've reduced emissions 73% 2002-2022 instead of just 25%, plus the "Energiewende" cost almost €700 billion (!), which could've been half that with the aid of nuclear in the power mix https://www.tandfonline.com/doi/full/10.1080/14786451.2024.2355642#abstract . "The road to Hell is paved with good intentions" indeed.