Equity returns don’t compensate for downside risks

One of the basic assumptions of modern finance is that equities have higher returns than bonds because they have bigger risks. The equity risk premium is generally supposed to be compensation for this increased risk. Over the years, more and more holes have been drilled into this basic assumption. Eugene Fama and Kenneth French even showed in a review article in 2004 that the relationship between systematic risk (i.e. beta) and returns is much weaker than predicted by the Capital Asset Pricing Model (CAPM).

Today we live in a world of factor investing where more than 300 factors have been identified that provide a statistically significant risk premium in violation of the CAPM. I was trained as a physicist and physicists tend to abandon a theory when it is empirically violated once. In finance, there are still people who believe in the CAPM even though it has been empirically violated hundreds of times.

Nevertheless, the advocates of modern finance continue to insist that while the CAPM might be imperfect, at least it has a grain of truth in it insofar as it postulates a relationship between risk and return. Now, Yigit Altigan and his colleagues have put this basic assumption to the most direct test I have ever seen. They took all the stocks in 26 developed equity markets and calculated a range of downside risk measures ranging from downside beta to value at risk on a monthly basis. Then, they looked at the relationship between the downside risks of stocks and the subsequent returns. If equity returns are compensation for downside risks, stocks with higher downside risks should have higher returns.

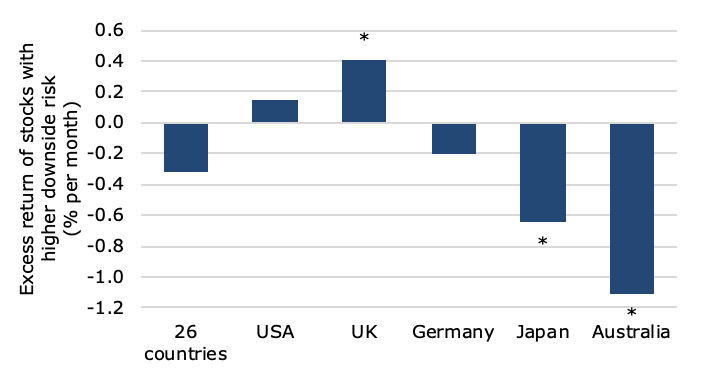

In order to test this hypothesis, they did the usual thing and split the stocks into five equal-sized buckets and measured the performance of the 20% stocks with the highest downside risks relative to the performance of the 20% stocks with the lowest downside risks. The chart below shows the result for five selected countries and the average over 26 developed markets if downside beta is used as a risk measure. Countries with statistically significant return differences are marked with an asterisk.

Equity return premium for downside beta

Source: Altigan et al. (2019).

On average, stocks with a higher downside beta had lower returns than stocks with a lower downside beta meaning that higher downside risks led to lower returns, not higher. In countries like Japan and Australia, the returns were so much lower that the difference was even statistically significant. The situation becomes even more extreme when we go further out to the tail of extreme losses. If we use Value at Risk (99%) instead of downside beta we look at only the most extreme 1% of negative events in each stock. And lo and behold, the risk premium is a risk discount in practically every country.

Equity return premium for Value at Risk (99%)

Source: Altigan et al. (2019).

If this doesn’t give you pause, then you either haven’t understood finance theory or these results. They are a direct contradiction of the most basic premise of finance and indicate that we get something fundamentally wrong about finance (or that this study is completely wrong and needs to be retracted). In my book, I dedicate an entire chapter on the topic of complex dynamic systems theory and how it improves on traditional finance. In a complex dynamic systems view of financial markets, equity return no longer has to be a compensation for increased risk and the results shown above are another indication that this new view of markets may be a better model of the world than the one we currently have.