ESG investing is a moody thing

I have been arguing for years that ESG investing is not about getting higher returns but about risk management. Financial markets and investors tend to be pretty good at assessing financial risks of stocks and other investments. Hence, these financial risks are usually priced accurately in markets. However, when it comes to softer risks such as environmental damage, exploitation of employees or bad governance, it is quite difficult to quantify them and investors have a hard time assessing them. In the past, investors have taken the easy way out and simply ignored them, which is where ESG investing comes in. By analysing potential risks in the E-, S-, and G-space, these investors might be able to discover risks that are not priced in the market and avoid stocks with higher risks in these areas.

What follows from this view on ESG investing is that stock portfolios formed with ESG risks in mind should not outperform traditional stock portfolios most of the time. However, once an ESG risk materialises, the ESG portfolio should have lower exposure to the stocks impacted by this risk and experience lower drawdowns and higher returns (relative to a traditional portfolio). If you were running a portfolio of British stocks in 2010 and had no exposure to BP when the oil platform in the Gulf of Mexico blew up, your portfolio would likely have outperformed simply by avoiding the losses of BP.

Unfortunately, the evidence on lower drawdowns and lower volatility for ESG portfolios is mixed, just like the evidence on ESG portfolios providing higher returns. It depends on the time period and the markets you investigate. But now, it seems as if there is a possible solution to this conundrum. Vitor Azevedo and his colleagues from the TU Munich investigated the relative performance of stocks with high S- and E-scores over time and found a link with investor sentiment.

In times of high investor sentiment stocks of companies with a high E- or S-score underperformed stocks with a low score. In times of low investor sentiment, high E and S companies outperform stocks with a lower score. And the relative performance difference between highly-rated and lower-rated companies was several percentage points per year as the chart below shows.

Outperformance of high E and S stocks depending on investor sentiment

Source: Azevedo et al. (2020).

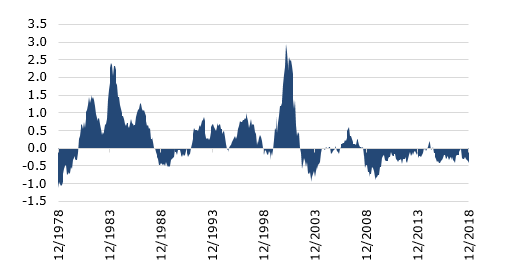

I have to disclose here that investor sentiment is not measured in this study in the usual way, that investors are used to. It doesn’t use the VIX or a sentiment survey like the weekly AAII sentiment survey but instead the stock market sentiment indicator developed by Baker and Wurgler. They create a sentiment indicator that is smoother over time and combines a series of indicators into a monthly sentiment indicator with some properties that are beneficial from an academic perspective. For example, the average value of the sentiment indicator is zero, so that it is easy to identify periods of high and low sentiment visually.

US stock market sentiment

Source: Baker and Wurgler (2006).

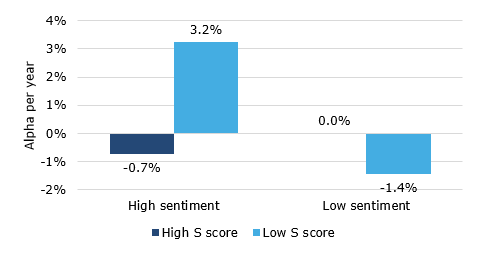

Using this sentiment indicator, it is possible to examine the performance of stocks with a high E- or S-score in times of high and low sentiment and compare it to the performance of stocks with a low E- or S-score. Taking into account the typical Fama-French factors of market risk, value, and size, the chart below shows the alpha of stocks with high and low S-scores.

Alpha of stocks depending on investor sentiment

Source: Azevedo et al. (2020).

Similarly, the chart below shows the same analysis for stocks with high and low E-scores.

Alpha of stocks depending on investor sentiment

Source: Azevedo et al. (2020).

What we can see in these charts is that the crucial swing factor are stocks with low E- or S-scores. In times of high sentiment, investors seem to become complacent and buy the stocks of crappy companies with a low ESG score (and correspondingly high ESG risks). In other words, the complacency of investors who are in a good mood creates a junk rally. When sentiment is low, be it because of a worsening economic environment or other factors, investors pay more attention to risks and try to avoid them where possible. This is when the stocks with low E- and S-scores underperform.

If his result is correct, it can explain several empirical observations. For example, it explains why different studies on the performance of ESG investments are inconclusive. The results of Vitor Azevedo indicate that in the long run, ESG investments should not create better performance than traditional investments. Only if you accidentally look at shorter time periods that cover predominantly a period of high or low sentiment will you see performance differences. In other words, ESG risk factors are not systematically priced in markets.

A second thing these results can explain is that the performance of ESG investments relative to traditional investments does not depend on these risks materialising as I have assumed in the past. Instead, the performance of ESG investments relative to traditional investments depends on the public perception of these risks. As long as the risks of climate change, for example, remain in the spotlight, ESG portfolios should continue the outperformance that I have written about a couple of weeks ago. Once investors become complacent about these risks and focus on other issues, green investments should experience an underperformance relative to traditional investments again. This is unfortunate because we know that investors have very limited attention and tend to only focus on the most pressing issues of the day. And at some point, a new shiny toy will come along that captures investors’ imagination and lift their sentiment…