Forget about calendar anomalies

Wall Street and the City of London have been obsessed with all kinds of “get rich quick schemes” for decades. As a result, several anomalies have been proposed to help investors make money. Among the anomalies that pop up regularly in the media and in questions from investors are calendar anomalies (makes you wonder why…). Every year in late April we are inundated by articles on the saying “Sell in May and go away” (in order to come back to the markets at Halloween or on St. Ledger’s Day, depending on whether you are American or British). And at the beginning of each year we hear about the January indicator.

Other prominent calendar anomalies are the day of the week effect that states that stock returns are higher on Friday than on Monday because traders tend to close short positions before they head out of the office for the weekend. Similarly, the holiday effect postulates that returns on the day before a public holiday are higher than normal, again because books are balanced and short positions closed. Finally, the turn of the month effect is based on a study that found that stock market returns at the end of the previous month and in the first weeks of the new month are higher than in the second half of the month.

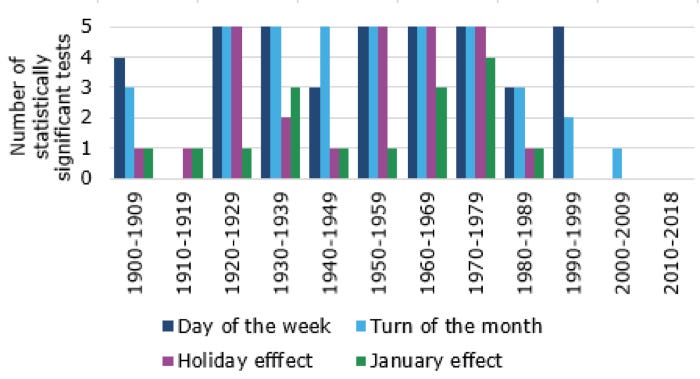

By now there is a plethora of studies that show that, at least historically, these calendar anomalies existed not only in the US but also in many countries around the world. On the other hand, more recent studies tend to show that these calendar anomalies seem to have lost their power in recent years. Now, a study by the University of Pretoria in South Africa has investigated the strength of some of these calendar anomalies in the US over time. Using the Dow Jones Industrial Average going back to 1900, this study tried to identify the day of the week effect, the turn of the month effect, the January effect and the holiday effect in each decade. They used five different statistical methods to identify the effect and simply counted how many of these statistical methods identified the effect as statistically significant. The chart below shows the main result of their study.

During the 1920s to 1980s, most of these calendar anomalies seem to have been significant and created relatively good signals for stock market traders. But with the advent of modern quantitative methods and automated trading in the 1980s and 1990s markets seem to have become more efficient insofar as these calendar anomalies gradually disappeared. In the 21st century they all seem to have disappeared completely. So, the next time you read an article in the press that touts the January effect or any of these calendar anomalies, you know what to do with it: ignore it.

Evolution of calendar anomalies in the US

Source: Plastun et al. (2019).