Global house prices and the temptation of populist policies

Last week the Bank for International Settlement (BIS) released its latest set of quarterly house price statistics around the world. While this data has significant lags (it only runs until the end of Q1 2019), it has the advantage that the BIS uses a unified methodology that allows for cross-country comparison and it has the most extensive data that I know of. So, if you want to know about the house price developments in North Macedonia, the BIS can help you.

House price developments have been in focus lately in many countries. In the US, house price growth has slowed down somewhat as the Fed has increased interest rates. In the UK, there is a marked dichotomy between London and the rest of the country, with house prices in London falling due to Brexit woes while they keep rising in the rest of the country. And in Germany, the state of Berlin wants to introduce a cap in order to curb the perceived excessive growth of rents in the nation’s capital due to fast rising house prices.

And indeed, the chart below shows that real house prices in Germany have grown faster than in any of the other major developed market. A lot of this is a result of steep house price increases in Berlin after the city managed to digest the supply glut that developed after the reunification in 1990.

The negative outlier in developed markets is Australia where real house prices have declined fast and there seems no end in sight. No wonder, the Reserve Bank of Australia tries to cut interest rates as fast as possible. They have to in order to stabilise the housing market.

Annual real house price growth in developed markets

Source: BIS.

But I digress. Coming back to Germany, there is lots of talk about a property bubble developing in the country and many people think it might be accelerated by the European Central Bank’s negative interest rate policy. By now, the public has become so concerned that the pressure on politicians to do somethingmounts.

The result are frankly stupid policy measures like the rent caps proposed in Berlin. Indeed, the proposed limits on rents are a typical example of regulatory incompetence. The left-wing government of Berlin proposed a cap of EUR 7.97 per square metre per month for flats completed between 1991 and 2013 – independent of location. This means that in pricy Prenzlauer Berg or Berlin Mitte, where rents are EUR 17 per square metre or so, rents will be halved, while in less desirable areas, rents will remain stable or may even increase. This means that wealthier households who can afford higher rents now receive a cut in rent by up to 50% while poorer households face potential increases. Furthermore, flats that were built in the early 1900s that are in particularly high demand due to their character features will face a rent limit of EUR 6.03 per square metre – because they are older. So, the people who can afford the best flats in the city will get the biggest rebates…

Of course, rents in Berlin have increased due to a serious lack of new supply and guess what a rent cap (that may not even be adjusted for inflation) will do to the supply? You guessed it. Nobody wants to build a new house or apartment building if they cannot get a decent rental yield. So, the undersupply is only going to get worse with the proposed legislation. The rent cap is about the best policy to increase inequality and the lack of supply you could think of. Well done.

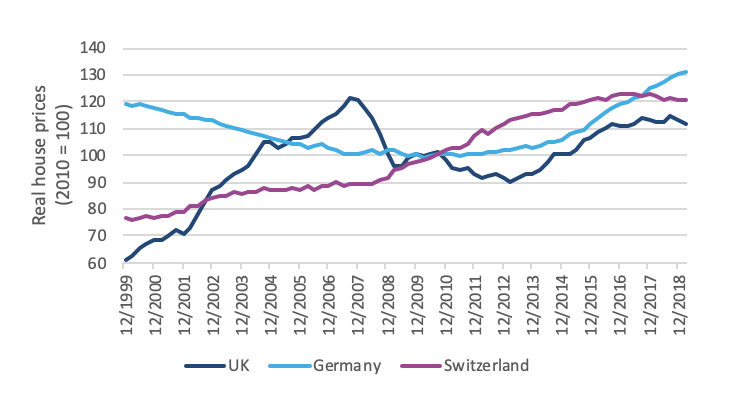

By the way, in my view, German house prices are not in a bubble at all. As the chart below shows, property prices in Germany have only recently managed to recover the losses of the first decade of the 21stcentury when oversupply led to massive drops in house prices. And back then nobody complained that rents were too low and needed to be increased…

Real house prices since 2000

Source: BIS.

Also, the chart above shows that negative interest rates need not lead to a property bubble. Switzerland has experienced negative interest rates for almost a decade now and house prices did not explode. All that was needed to do was for the Swiss National Bank to introduce countercyclical measures like an increased reserve requirement for banks wanting to lend money for new mortgages. This “antizyklischer Kapitalpuffer”, together with stricter requirements for the amortisation of mortgages was enough to keep house prices under control. In fact, over the last year or so, house prices have even started to decline in Switzerland.

Politicians in Germany and other countries who flirt with crude regulations should take notice of the Swiss example. A market-based solution is usually the best way to keep asset prices under control and in local housing markets, central banks still have a lot of tools at their disposal that they can use. There is no need for political intervention.