Improving factor returns through structural factors

While smart beta funds and factor investing have moved into the background a little after years of disappointing returns, it is by no means dead. Clearly, fund managers follow a certain style which is often informed and dependent on the performance of one or more factors. But what if the factors reported in the literature are distorted by the constantly changing valuations of stocks?

Obviously, if you are a value investor, you want to see the valuation of your shares improve. That is what you try to exploit. But if you are a momentum or quality investor, changes in valuation aren’t really what you are after. Yes, if the market realises a company is highly profitable, it should reward this with a higher valuation. But the fundamental return driver should be the increase in book value and the dividends generated from the profits, not the change in P/E-ratios or P/B-ratios.

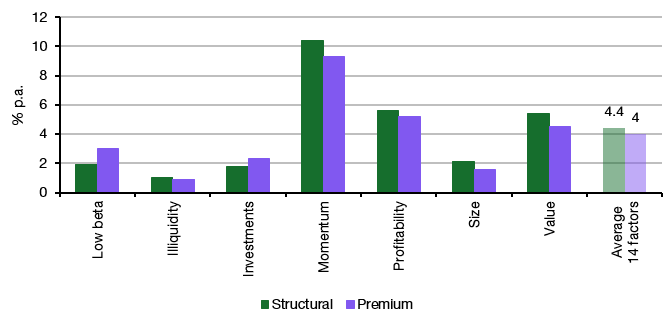

What the folks at Research Affiliates did is estimate how much of the reported factor return is due to this change in valuation over time and how much is due to structural risk premiums that are driven by changes in the fundamentals of the factor at hand. Effectively, they backed out the change in P/B-multiples from the reported factor return and called what is left the structural component.

Here is a chart of the structural premium vs. the reported premium for a selection of prominent factors and the average of the 14 factors they analyse in the note. In most cases, changes in valuation give a negative contribution so that the structural premium is a little bit higher than the one reported in the literature. For the 14 factors analysed, the reported average annual factor premium is 4% (between July 1973 and December 2022), but changes in valuations created an average drag of -0.4% p.a., reducing the true structural factor return of 4.4% p.a.

Attribution of factor returns

Source: Arnold et al. (2025)

The question that arises from this analysis is the ‘so what’ question. After all, you can’t invest in such a way that you only get the structural factor return. You will always get the realised return, and you cannot ‘hedge’ changes in valuation multiples.

But investors need to build portfolios, and changes in valuation should (in theory) cancel each other out in the long run. The very fact that there is a small revaluation return in the chart above shows that even for investment periods of 30 years, that isn’t necessarily true, but the return contribution from this revaluation effect declines significantly over time.

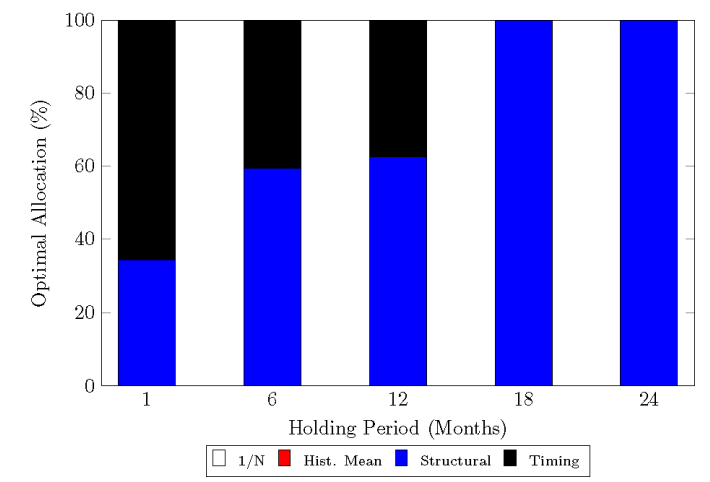

Hence, if you construct a portfolio, the longer your investment horizon, the less important the revaluation return and the more dominant the structural return. Hence, if you are a long-term investor, you should get better results if you use the structural factors to estimate the right weight for different factors in a multi-factor portfolio. And that is exactly what the researchers get in their analysis when they try to build a multi-factor portfolio and compare its performance to several benchmarks.

Optimal weights to multi-factor portfolios

Source: Arnold et al. (2025)