Intangible assets and rate hikes

The increasing share of intangible assets on the balance sheets of companies has created all kinds of problems, particularly for value investors. At the same time, recent research indicated that companies with lots of intangible assets on their balance sheets might be the better growth investments. Now it seems as if these companies with lots of intangible assets could also be a haven for growth investors in times of rising rates.

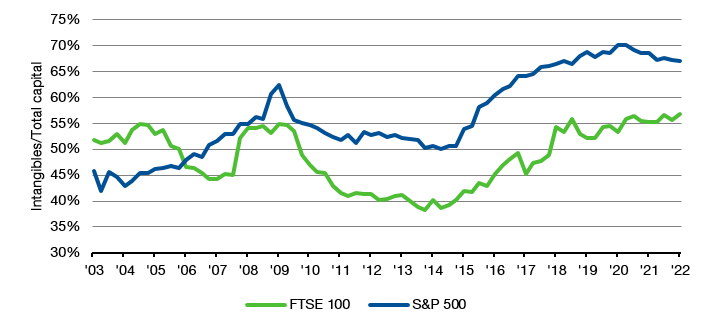

Robin Döttling and his colleagues from the IMF have investigated how the share prices of companies react to changes in monetary policy. They looked at companies with a high ratio of intangible assets on the balance sheet and compared their performance around Fed rate announcements with that of companies with a low intangible ratio. US companies have seen their intangibles as a share of total book value or total assets rise substantially over the recent decades, but as the chart below shows, that isn’t just a US phenomenon. We have seen this all over Europe, even in the FTSE 100 which is so full of commodity and financial stocks that it was once compared to Jurassic Park by hedge fund manager Paul Marshall – shortly before he made a large bet on UK stocks as oil prices rose…

Share of intangible assets

Source: Bloomberg

What the researchers from the IMF found was that in reaction to rate hikes by the Fed, companies with a high intangible asset ratio reduced their investments less than firms with a lower intangible asset ratio. They can do that because of two fundamental effects. First, companies with a higher intangible asset ratio rely less on debt when they acquire companies and more on equity transactions. This means, that their M&A activities are less sensitive to the prevailing interest rate environment.

Second, intangible assets are typically depreciated at a faster rate than tangible assets. In a time of rising interest rates, when investors increase their discount rate for future cash flows, this means that the net present value of companies with high intangible asset ratios drops less than the net present value of companies with low intangible asset ratio. If we think about it in terms of bonds, intangible assets have a shorter duration than tangible assets so when interest rates rise, their value drops less. This discounting effect even helps to reinforce the M&A effect because if a company’s share price drops less in times of rising rates, it is better able to use its equity as collateral for future M&A.

And in the long run, it also helps companies with a high intangible asset ratio outperform companies with a lower intangible asset ratio. Because if a company keeps its investment activity relatively unchanged in response to rate hikes it means it is investing more in future growth than its peers and will on average outperform them in the long run.

https://etf.sparklinecapital.com/itan/