It’s all in the earnings

Share prices deviate from fair value all the time. And the volatility of stock markets is much higher than what is justified by fundamentals. That clearly is old news, and in fact, it is so old that people have formally proven that four decades ago and were awarded the Nobel Prize for that proof almost a decade ago.

But when it comes to what drives investors to move share prices away from fair value, a paper by Andrei Shleifer and his colleagues has caught my eye. It is easy to say that what drives variations from fair value are things like sentiment (optimism vs. pessimism, greed vs. fear) or faulty expectations about future earnings (if you go back to late 2019, people did not expect earnings to drop as much as they did because they didn’t expect a global pandemic). But it is much harder to try to quantify the impact of these factors.

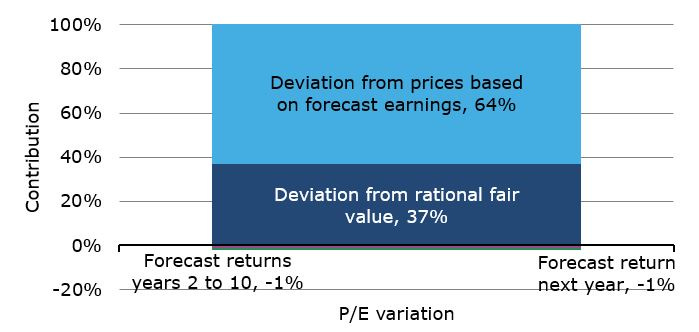

Andrei Shleifer is a member of the pantheon of behavioural finance and his research is always worth reading, though it can be quite theoretical. In this case, he built a simple model for deviations from fundamentals based on analyst expectations for earnings growth and future stock market returns. I spare you the technicalities, but one of his key findings is that the variation in valuation measures like the P/E-ratio is driven by two factors: the difference between expected earnings and realised earnings, and the difference between expected fair value and fair value after realised earnings. What has practically no influence on valuation measures is the expected return next year or over the next decade. It is all in the earnings.

Contribution to variation in P/E-ratios

Source: Bordalo et al. (2020)

The two factors I mentioned above as key drivers of valuation ratios may sound similar but they are not. The first one is driven by faulty forecasts of future earnings. Investors form their expectation of future earnings and put them into some kind of fair value model, like a discounted cash flow or a dividend discount model. Then, over time, earnings materialise and they may be substantially different from the original forecasts. This forecast error is what drives about two-thirds of the variation in P/E-ratios in the United States, according to Shleifer’s estimates. The second factor, deviation from rational fair value, accounts for all the mistakes investors make in forecasting the other ingredients of a fair value model, like the risk premium for equities or the expected inflation rate, etc. This is for example what drives short-term swings in valuations due to sentiment shocks like market panics.

So, if forecast earnings and the errors made by investors in these forecasts are the key drivers for market deviations from fair value, then we have to ask which earnings forecasts are the most important ones? Again, I spare you the details, but it turns out, that next year’s earnings or the earnings in the subsequent years aren’t relevant. What drives the deviation from fair value more than anything else (by a factor of ten more than near-term earnings forecasts) are long-term expected earnings growth.

This makes sense because most earnings are many years in the future and if investors become too optimistic about long-term earnings growth, they are likely calculating a ‘fair price’ that is much higher than an investor who is only optimistic for the next couple of years. So, one of the key drivers of valuations that investors should pay attention to is long-term expected earnings growth. Below, I show the situation in the United States (S&P 500) and Europe (Stoxx Europe 600) today in comparison to historic data as far back as I could find it. According to the research by Shleifer, what matters is not the level of expected long-term earnings growth but the change. If analysts upgrade their long-term earnings growth expectations, that is typically followed by rising valuations and lower returns over the subsequent 1, 3, and 5 years. When analysts reduce their long-term earnings growth expectations, this is followed by lower valuations and higher equity returns. And what we observe today is that long-term earnings growth expectations in the United States are rising while in Europe they are falling. The difference between the two regions is small, so one should not make too much of it, but at least we can say that investors in the United States are pricing in more and more optimistic scenarios for the future, while investors in Europe do not.

Current long-term earnings growth expectations

Source: Bloomberg