Kickbacks are bad for clients, banning kickbacks is even worse

As many readers know, I have been working in Swiss private banking for most of my career and I have witnessed first-hand the sales practices of these companies. By now, every Swiss bank pretends to have an open architecture where they offer both in-house and third-party funds, but in practice, the incentives in all these banks are skewed towards pushing in-house products. But I am not complaining, private banks are in the business of making money and in-house products simply are more profitable, so they are promoted more than less profitable third-party products.

In the past, third-party funds could make it into the portfolios of clients of large private banks by offering kickbacks to the distributors. These kickbacks were typically not disclosed to the customers who bought the funds, nor did the customers get any of that money. They were considered compensation for the distributor for the effort to promote the fund.

In October 2012, the Swiss Federal Supreme Court ruled that customers own all the kickbacks the bank was paid. Hence, if a bank was selling funds that paid kickbacks, these kickbacks had to be passed on to customers. In effect, this led to the end of kickback provisions in the Swiss fund market.

Nic Schaub and Simon Straumann examined what happened next.

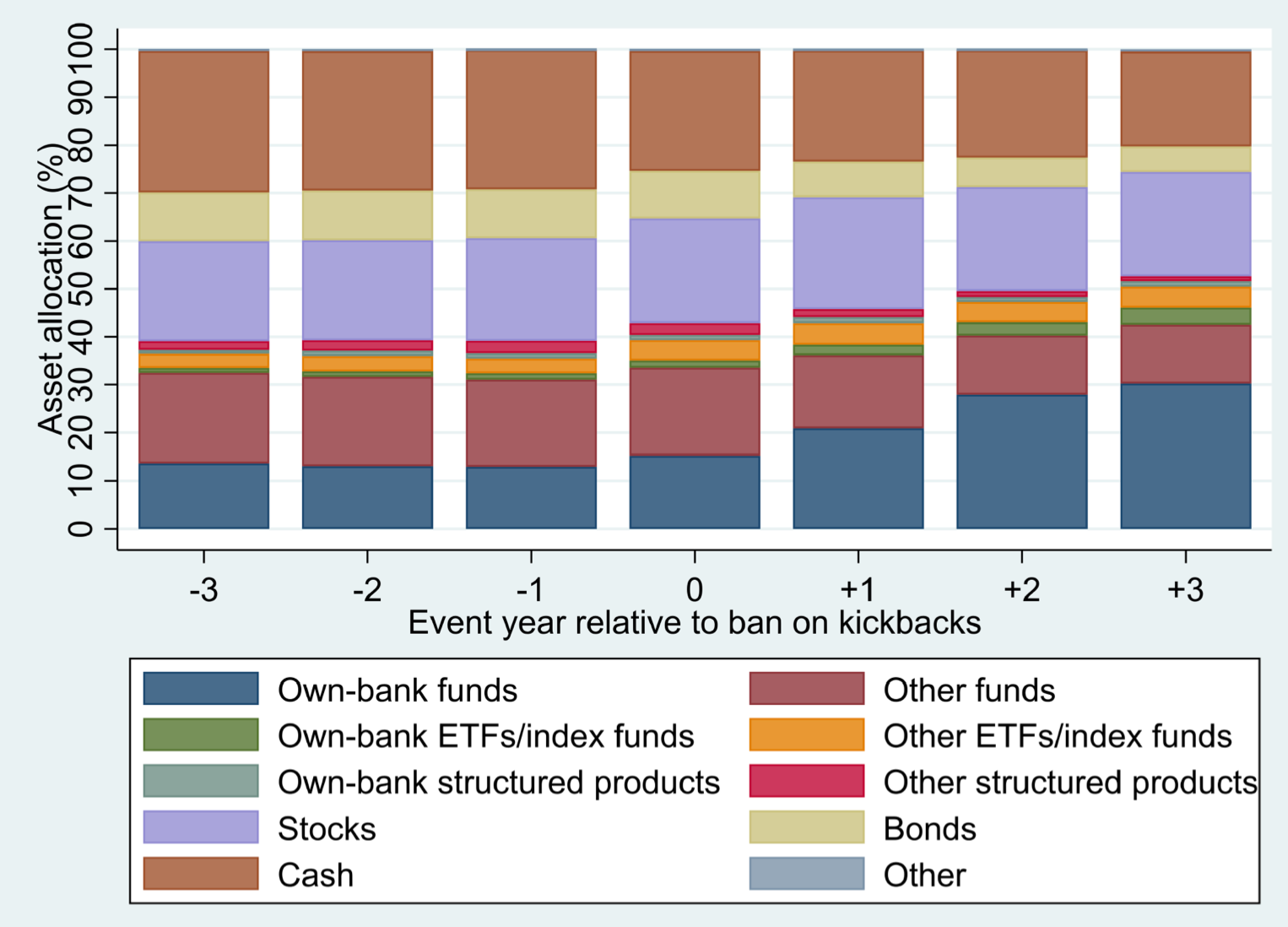

They looked at the portfolios of some 17,400 private banking customers in Switzerland between 2010 and 2020. What they found is summarized in the chart below. Note, how after the introduction of the ban on kickbacks, the share of third-party funds drops, and the share of in-house funds increases by 5-10 percentage points.

Portfolio composition before and after the abolition of kickbacks

Source: Schaub and Straumann (2022)

Banks followed their incentives and replaced third-party funds with in-house funds to protect their margins. The problem is that banks don’t always have the best fund in the market for every asset class. Hence high-quality third-party products were replaced with medium- or low-quality in-house products.

In the end, the outperformance of client portfolios of banks that eliminated kickbacks dropped by 0.9-1.6% per year. Meanwhile, the kickbacks banks received before the ban were some 0.4% per year. In other words, the ban on kickbacks led to a net loss of 0.5-1.1% per year for end customers. Every regulation has unintended consequences and in Switzerland, private banking clients in the end seem to be worse off today than before kickbacks were allowed.

The remedy I have followed is: Do not buy from a Bank. Do your own research and decide which Fund is best for your context,