Media matters for the share price

Media matters for the share price

One of the things that I am fascinated by is the increasing role media plays in shaping public perception. The rise of social media has led to vastly different experience bases (i.e. echo chambers) for each of us. Yet, one area where echo chambers so far are not too prevalent is financial news. Yes, there are differences between ZeroHedge and CNBC and their respective views on markets, but overall, investors still get their financial news from a small group of leading newspapers like the Wall Street Journal and the Financial Times and from TV stations that are either dedicated to financial news (Bloomberg TV, CNBC) or general broadcaster (e.g. BBC, public TV all over Europe).

This relative concentration in opinion-shaping media allowed two researchers from Germany to measure the impact of media tonality on share prices. They looked at almost 105,000 news reports on companies in the S&P 500 from 2006 to 2016. Then they formed a Media Tonality Index that measured, how positive the media coverage of a company was at any given time. Naturally, since the analysis covers the financial crisis, coverage of financial services firms dominated, with one in four reports covering a firm in that sector. But coverage of cyclical consumer companies and communication services companies was also well-represented with 16% of all repots covering each of these two sectors. Meanwhile, utilities, industrials and mining companies were relatively underrepresented in the coverage. But the study still provides a good overview of the impact positive or negative media coverage can have on a company’s share price.

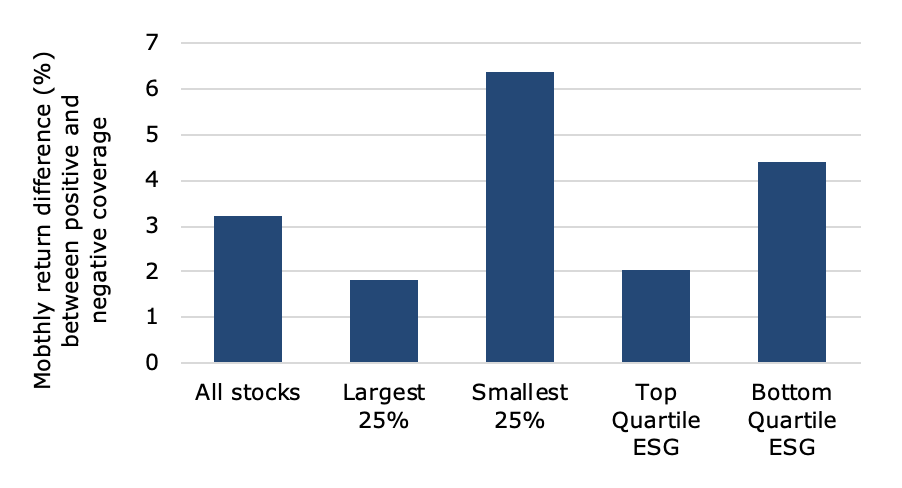

And the impact is truly substantial. On average, the 25% companies with the most positive media coverage outperform the 25% companies with the most negative media coverage by 3.2% per month. Hence, if an investor can forecast positive and negative media coverage, she would be able to massively outperform the market. Unfortunately, the performance difference only exists as long as one uses contemporary media coverage. Using past media coverage makes the performance difference disappear. Hence, this is not a strategy to outperform markets because nobody can predict media coverage.

Average monthly share price impact of positive and negative media coverage

Source: Naumer and Yurtogly (2020).

However, the chart above also shows that the performance impact of positive vs. negative media coverage is not the same for every company. Larger companies tend to have inbuilt insurance against negative media coverage. Because these companies have a larger investor base and are heavyweights of indices, it takes much more negative and much more persistent media coverage to seriously impact the share price. A Diesel scandal like in the case of Volkswagen will do the trick but reports about child labour used to produce the cocoa used in the chocolate of Nestle and other food producers will be shrugged off.

Smaller companies don’t have that luxury. If a smaller company becomes the focus of negative media coverage the share price can be dramatically impacted. On the other hand, if a smaller company becomes the focus of positive media coverage, its share price can skyrocket. Thus, managing the media coverage and the media image is much more important for smaller companies than for larger ones.

Which brings me to another variable that influences the impact of positive and negative media coverage on share prices. Companies that rank in the top quartile of all companies in terms of ESG scores tend to suffer much less from negative media coverage than companies that rank in the bottom quartile. The study does not say why this is the case, so I am free to speculate. I think, though I cannot prove it, that if a company takes ESG risks seriously, it inadvertently reduces the risk of negative media coverage for bribery, excessive compensation, environmental damages or other issues. And when there is no story, then there is no negative coverage of the company. As a result, companies that take ESG seriously tend to be more resilient against negative media coverage. For company executives, this should be yet another incentive to increase their efforts in the ESG space. It may not lead to a higher share price, but it seems to insure you against a sudden drop in share price due to negative media coverage.