NextGenerationEU works

During the pandemic, the EU launched its massive NextGenerationEU industrial policy programme. It was Europe’s answer to the Inflation Reduction Act in the US. But after last year’s European elections, some €400bn in additional spending was put on ice. And that may have significant long-term growth consequences for Europe.

Large-scale industrial policies like the Inflation Reduction Act and NextGenerationEU are often dismissed by conservative economists and politicians as a form of government intervention in free markets and a form of ‘the government picking winners’. However, there is plenty of evidence that if done right, industrial policy can substantially boost economic growth for years, if not decades. Just ask anyone in Japan, South Korea or Taiwan what they think of industrial policies, and they will give you a very different answer than people in the US or Europe.

For everyone interested in what makes industrial policy so powerful and how to design a good industrial policy, I highly recommend a recent overview by Réka Juhász and Nathan Lane.

In the case of NextGenerationEU, a team from the ECB has done an interim assessment four years into the programme to assess how it has worked so far and what its likely consequences are for growth and inflation in the EU.

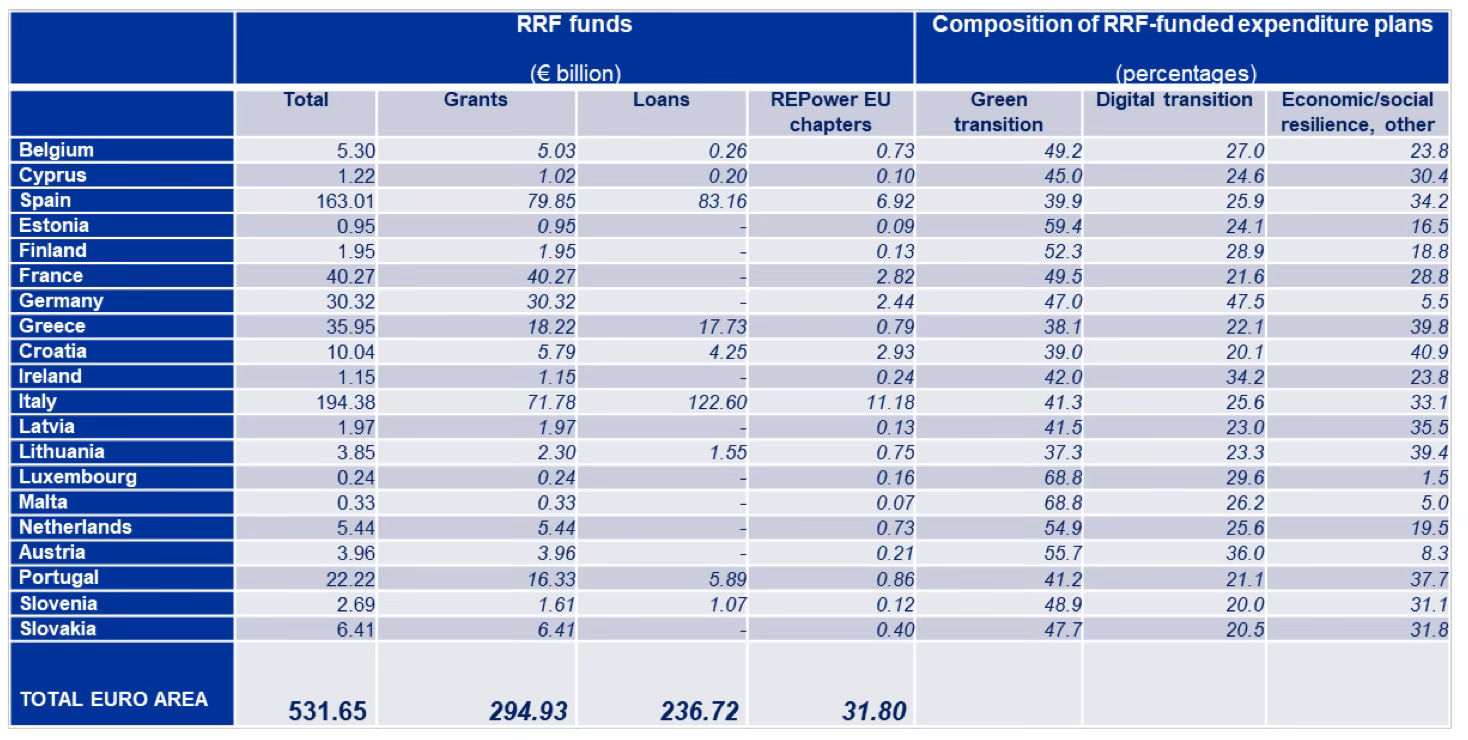

So far, NextGenerationEU has a volume of more than €600bn allocated to different countries in the Eurozone as shown below. Italy and Spain are the largest recipients and poorer countries like Croatia, Greece, and Portugal receive more relative to their GDP than richer countries. On top of the monies shown below, there is another €100bn to other EU members that are not part of the Eurozone. About half that money goes to Poland, a quarter to Romania and about 8% each to Czechia and Hungary.

Distribution of NextGenerationEU funds among Eurozone countries

Source: Bankowski et al. (2024)

The reason why the remaining €400bn in NextGenerationEU funding has never been approved by the European Parliament is the column titled ‘Green transition’ in the table above. About half of all funds are targeted for green transition projects, which is something the conservative parties across the EU will not support. As a result, the remaining money for NextGenerationEU will not be approved.

Had these additional €400bn been approved, NextGenerationEU would have been of the same size as the Inflation Reduction Act in the US relative to the GDP of the EU. The damage this reluctance to green transition projects will do to EU economic growth can be seen by looking at the headline results of the impact of the €600bn spent so far on the EU.

I encourage everyone to read the full paper linked above because there is a lot of detail about individual countries and how institutional reforms linked to industrial policies and grants have been a major growth driver. But for now, let’s stick to the headline estimates.

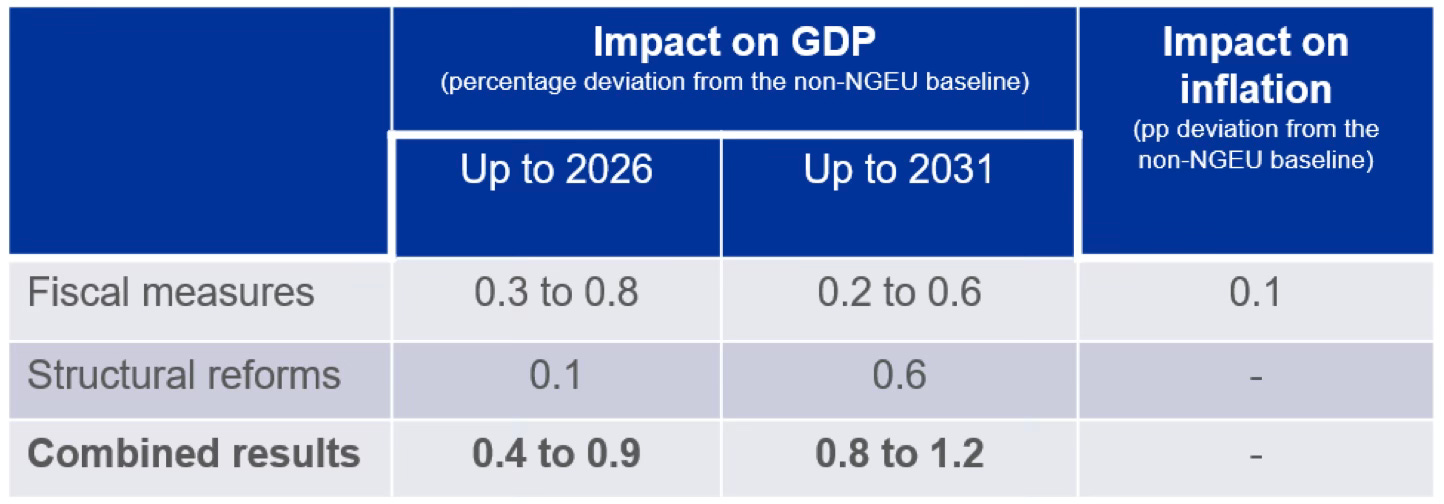

Estimated impact of NextGenerationEU funds on Eurozone GDP and inflation

Source: Bankowski et al. (2024)

The Eurozone may have been lagging the US in growth, but without the NextGenerationEU investments, the gap to the US would have been even larger. The authors of the study estimate that Eurozone GDP will be some 0.4% to 0.9% larger in 2026 than without the investments from NextGenerationEU. And by 2031, ten years after the programme was launched, Eurozone GDP may have been boosted by 0.8% to 1.2%. Meanwhile, they cannot find any evidence of inflation increases due to the programme.

If you ask me, the EU should spend more money on industrial policies like NextGenerationEU and not less. Politicians arguing against such investments are doing the region a disfavour and are effectively reducing growth in the EU while the US is marching ahead with an Inflation Reduction Act that is almost twice as large as what the EU has done so far.

Yes, the numbers are large, and many fiscally conservative politicians argue against these investments because they add too much to the EU’s debt. But this is shortsighted. If investments boost GDP growth, the debt/GDP-ratio will be lower, not higher. Arguing that all debt is bad is what the Germans call a ‘Milchmädchenrechnung’ (I don’t think there is an equivalent English term, but please let me know in the comments if you know of one).

It ignores that some debt leads to higher growth and higher income while other debt does not. It’s all in the fiscal multiplier as I have argued here. And the fiscal multiplier of NextGenerationEU is larger than 1.0.

I was working in the Malaysian government for many years, and if you want further evidence on what good government planning and involvement in industry can accomplish, look at the success it had in that country. In a few years it changed its agriculture from subsistence rubber trees to the most extensive palm plantations and palm oil No.1 oil in world trade.

Let's hope the EU listens to the evidence and doesn't get to horny over military spending and waste it on that.

I guess the UK will continue to just bumble along...and waste billions on getting people from Birmingham to London in the same time it takes them now, and in litigation trying to get new runways approved!