OK Boomers

It has become fashionable to blame many of today’s problems on the baby boomer generation. Born between 1945 and 1965, these people enjoyed the full extent of the 40-year decline in interest rates in the United States during their prime earnings years. Hence, they could invest their savings at exceptionally high equity and bond market returns while at the same time see the value of their homes increase steadily. Now, this generation is retiring and calmly “plundering” social security, pension funds, and Medicare putting an increasing burden to finance these safety nets on younger generations. As a member of Gen X, I have felt my entire life as if I arrived at a party just after it ended.

However, whenever I think that our problems today are bigger than those of my parents, all I have to do is remind myself that in 30 years’ time, the world will be run by kids that have been home-schooled in 2020 by their drunk parents. And then I feel better…

But getting back on topic, I don’t want to chime in on the “blame the boomers” game because it is useless and certainly doesn’t help us solve our current problems, let alone those we will face in 30 years. But I cannot help share with you a series of studies that showed that despite the financial tailwinds boomers enjoyed throughout their lives, they still seem to have been unable to live within their means.

Let’s start with the latest study by the godmothers of personal finance research, Annamaria Lusardi from George Washington University and Olivia Mitchell from the University of Pennsylvania. Together with Noemi Oggero from the University of Turin, they analysed data from the 2015 National Financial Capability Study to check how many Americans remain in debt shortly before retirement.

Ideally, we all should reduce our debt to zero or close to it in the years before retirement because, with the end of our working lives, our income tends to drop, and our ability to get new loans diminishes significantly. Hence, after retirement, we tend to be forced to live within our means, and servicing existing debt at this stage in our lives increases the chance of old-age poverty and bankruptcy. Unfortunately, the boomer generation that was within five to ten years of retirement in 2015 (people born between 1955 and 1960) still held debt rather frequently. The chart below shows that about one in three Americans in that age bracket still had to service a mortgage on their house and one in ten even had a home equity loan on top of their mortgage. Furthermore, about three in ten did not own their car and one in seven had to rely on alternative sources of loans like payday lenders or pawnshops to finance their living.

Share of Americans aged between 56 and 61 with debt

Source: Lusardi et al. (2019).

But never mind the credit sharks in pawn shops and payday lending forms, what really stands out, in my view, are the 11% Americans with a home equity loan and the 6% with a student loan, at age 56 to 61! How can you go through life without ever paying back your student loan? How can you go through life relying on a home equity loan on top of your mortgage? As a German, I am notoriously shy to take on any debt (I always pay my entire credit card balance every month, thus effectively turning my credit card into a debit card), so this kind of behaviour is shocking to me.

One may argue that the study does not say how big the outstanding debt is. If it is small, it probably can be paid off before retirement or it doesn’t matter too much during retirement, but a different study by researchers from the Federal Reserve Bank of Philadelphia looked at the amount of outstanding debt for older people in the United States. It then tracked the value of that debt from 1996 to 2006 as these people grew older.

The chart below shows that Americans do try to reduce their debt in retirement. Median unsecured debt (i.e. credit card debt) stood at roughly $2,000 for people aged 65 in 1996 and the trend during retirement was towards less unsecured debt. But secured debt (i.e. mortgages, home equity loans, etc.) increased during retirement. The youngest cohort tracked in the chart saw their median secured debt increase from $30,000 at age 65 to $43,000 at age 75. To finance their retirement, these people need to increase their debt.

Median gross debt of Americans in retirement 1996 to 2006

Source: Nakajima and Telyukova (2019).

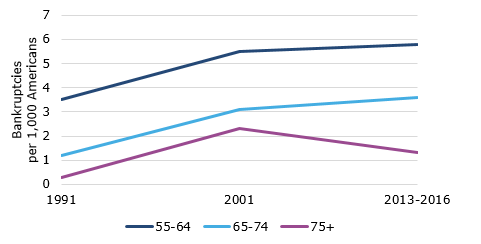

In extreme cases, retirees cannot pay off their debt and have to default. We live in an age where families are increasingly fragmented so that the traditional safety net of family members has become weaker and is less able to support older people. When there is no help from family or friends forthcoming, living beyond your means in retirement can drive you into bankruptcy. While bankruptcy rates in the United States have declined on average, baby boomers face rising bankruptcy rates. The chart below shows that the rate of bankruptcies amongst people close to or in retirement has doubled or even tripled between 1991 and 2016. The silent generation knew how to live within their means and rarely defaulted on their debt. The baby boomers are saddled with debt well into their retirement and are increasingly unable to pay off this debt.

Bankruptcy rate by age 1991 to 2016

Source: Thorne et al. (2018).