Persistence > performance

Earlier in the year, I showed the chart of analyst forecasts and how they struggle to get even the direction of equity returns (positive or negative) right. Strategists are no better than the flip of a coin in getting the direction of markets right. Yet, it seems that it is possible to get the direction of returns right and that if it is done the right way, one could earn excess returns in the order of 1% per month.

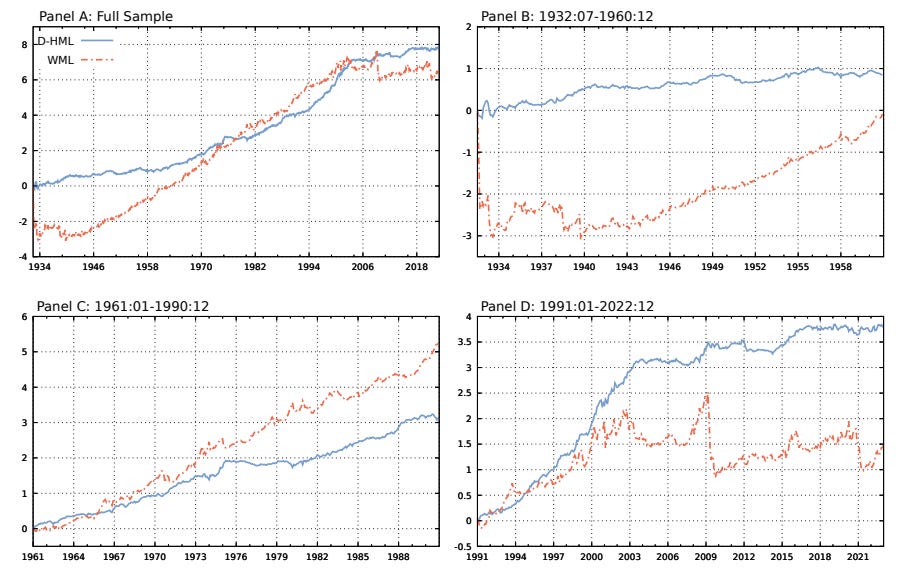

A team from ESADE Business School developed a model that they call Directional High Minus Low (D-HML) which tries to estimate the probability that a stock is likely to have a positive return next period and then sorts stocks by this likelihood.

This probability is estimated by looking at the number of days, weeks, and months in the last 12 months when the stock had positive or negative returns as well as the idiosyncratic volatility of the stock. The idea is that if a stock has seen a long run of positive days, weeks, or months, it is likely to show a positive return the next day, week, or month as well. If this type of momentum persists, then buying stocks with the highest probability of a positive return and shorting stocks with the lowest probability should create positive returns.

And indeed, before transaction costs, this strategy does create an average annual long-short return of around 1% per month (12.7% per year). Crucially, though, these returns are different from traditional momentum returns. By counting the length of a rally, one would suspect that the D-HML strategy would simply be a momentum strategy in disguise, but rather than look at the absolute past return of a stock, it looks at the persistence of return, which is a different thing. The charts below show that the performance of this D-HML can be quite different from a traditional momentum strategy (denoted WML for winners minus losers in the charts).

Performance of a D-HML strategy vs. a traditional momentum strategy

Source: Del Viva et al. (2023)

Crucially for investors, this D-HML strategy is much less prone to momentum crashes, i.e. the sudden turn of fortunes for momentum investors that can destroy months or years of past outperformance in a couple of weeks. The chart below shows the performance of the D-HML in comparison to the traditional momentum strategy during extreme drawdowns. In essence, the losses of the 5% worst periods for traditional momentum are similar to the losses of the 0.1% worst periods in the D-HML strategy. Hence, there is much more downside protection included in the D-HML strategy.

Drawdowns of D-HML and momentum strategies

Source: Del Viva et al. (2023)

This resonates with observations I have made in two previous posts. This post showed that momentum strategies can be made more robust if one restricts momentum stocks to those that show shorter-term persistence in momentum. And this one showed that momentum crashes can be anticipated by looking at shorter-term persistence (or lack thereof) in price momentum. In other words, the persistence of performance is probably a better indicator of future performance than pure price momentum.

On Twitter, there was a meme being passed around during Covid showing two guys. One guy said, “when stocks go up, I buy. When stocks go down, I sell” the other guys said, “I can’t read”. Perhaps the strategy is as “simple” as that as, put simply, that’s what those professors found