Post-earnings announcement drift is not just for equities

Last Thursday, I teased my readers that post-earnings announcement drift has recently been documented in corporate bonds. And it is a factor with such strong performance characteristics that bond investors should take note.

The post-earnings announcement drift in stock markets is the phenomenon that in some cases, share prices do not react to positive or negative earnings surprises as much as the share price beta to the total market would imply. This can happen if a stock is small or less liquid or if the earnings announcement of the company is not followed widely by the investor community because the stock is considered unexciting. Or it can happen when earnings releases are dominated by macro or other events on the same day. Whatever the reason, investors can exploit the post-earnings announcement drift by investing in stocks that have underreacted to recent positive earnings surprises and selling stocks that have underreacted to recent negative earnings surprises.

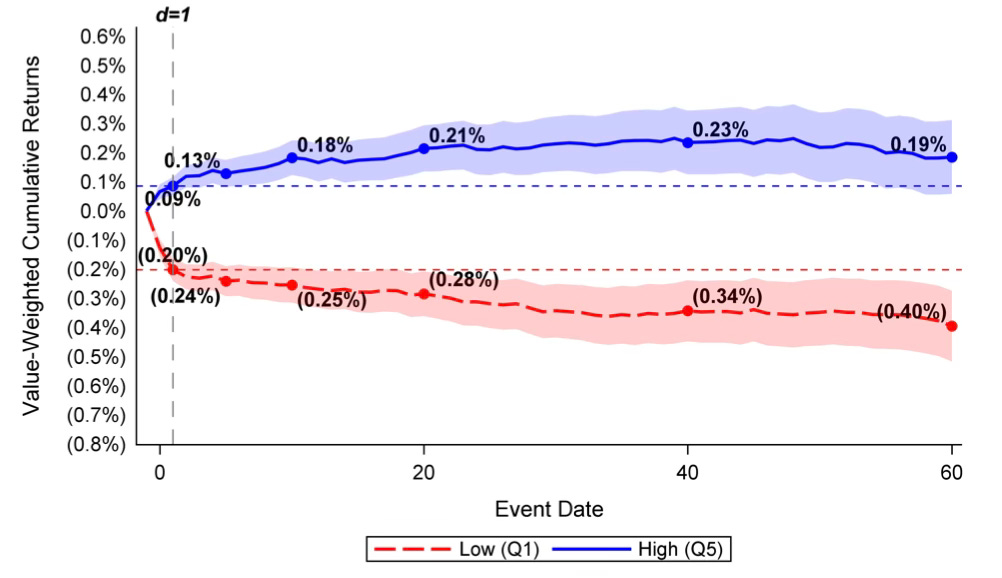

In corporate bonds, Yoshio Nozawa and his colleagues have documented the same effect. Here is a chart of the typical post-earnings announcement drift of investment-grade corporate bonds for companies where the stocks have underreacted to recent earnings surprises.

Post-earnings announcement drift for investment-grade bonds

Source: Nozawa et al. (2022)

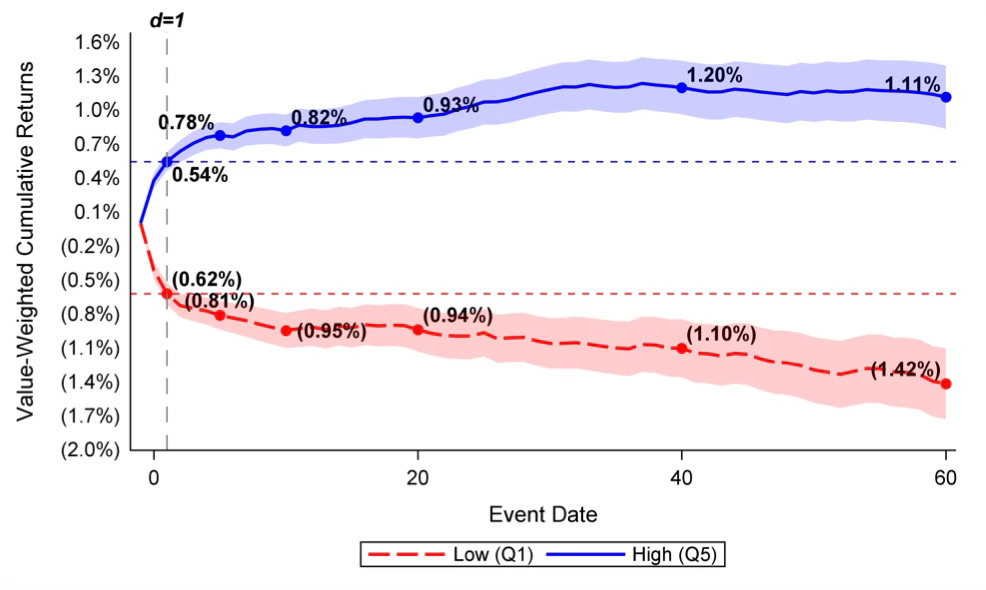

And here is the same chart for high-yield bonds.

Post-earnings announcement drift for high-yield bonds

Source: Nozawa et al. (2022)

Going long the bonds of the companies with the 20% highest earnings surprises and shorting the bonds of stocks with the 20% largest earnings misses delivers on average a return of some 0.59% after three months for investment grade bonds and some 1.53% for high yield bonds. And that is per bond.

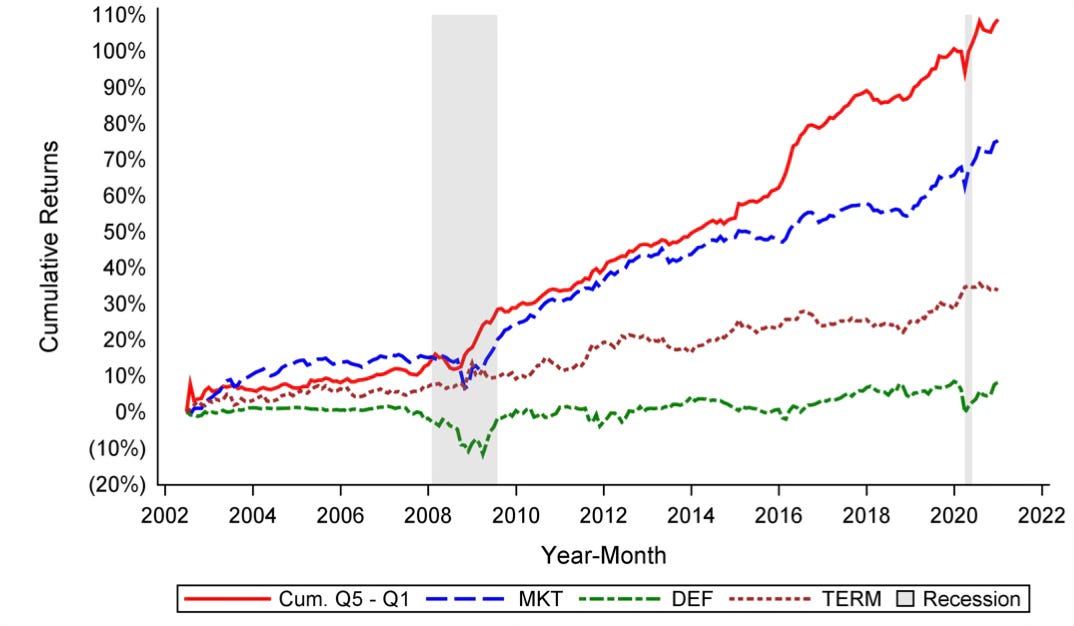

So, what happens if one creates an entire portfolio of investment grade and high-yield corporate bonds based on this long-short strategy? The chart below compares the performance of this long-short strategy based on post-earnings announcement drift with the performance of the overall bond market, the performance of going long 10-year Treasuries and short T-Bills (TERM), and the performance of going long investment grade bonds and shorting Treasuries (DEF). Adjusting for a battery of 11 possible factors, the annual alpha of the long-short strategy on post-earnings announcement drift is some 4% and the annual return is some 5%. That is extremely large for a bond strategy and much more impressive than investing in the market or exploiting the term-premium or the credit risk premium as the chart below shows.

Performance of different bond investment strategies

Source: Nozawa et al. (2022)

Very surprising to me. Since the biggest brains in the investing world work in the bond market, I would have supposed anything like this would have been arbitraged away long ago.