Privilege lost?

The US has historically benefited from the exorbitant privilege of issuing the world’s reserve currency and the benchmark safe asset in the form of Treasuries. But evidence is mounting that at least in the Treasury market, the country has lost that exorbitant privilege, possibly forever.

Some time ago, I wrote in my Reuters column that I was concerned about the decline in the Treasury convenience yield compared to German Bunds after Liberation Day. This convenience yield measures the difference in yield between a ‘synthetic’ Treasury note constructed by investing in Bunds plus swaps and simply buying a Treasury note. As you can see in the column, this convenience yield is currently negative, meaning that owning the actual Treasury (the real thing) pays a higher yield than owning a synthetic ‘fake’ Treasury. This is not how it is supposed to be.

If Treasuries are the world’s reserve asset, people should want to hold Treasuries outright rather than some synthetic version. This is why it is called convenience yield in the first place. You get a lower yield for the convenience of not having to hold a German Bund and a couple of swaps in your portfolio, and the privilege of giving your money to the world’s most creditworthy government.

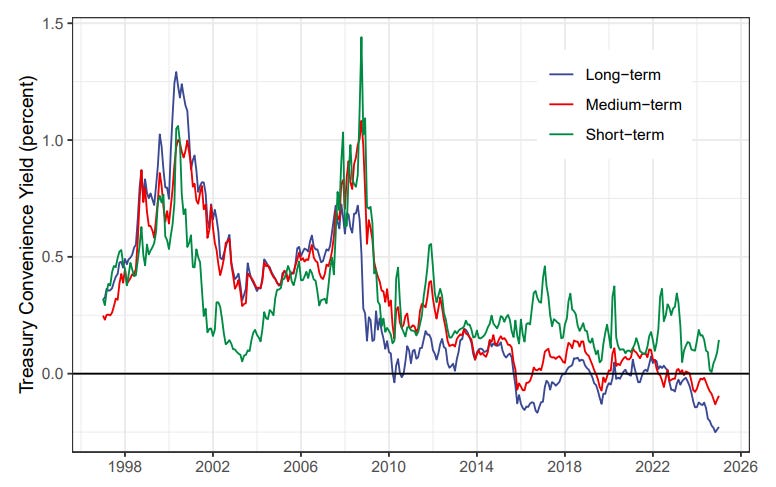

Historically, this has been the case, as the chart below, taken from a study by Zhengyang Jiang and his collaborators, illustrates.

Convenience yields of Treasuries with different maturities

Source: Jiang et al. (2025)

But as you can also see in the chart, this convenience yield has been on a steady decline. And indeed, there is one key driver of the declining convenience yield: The rising debt mountain of the US.

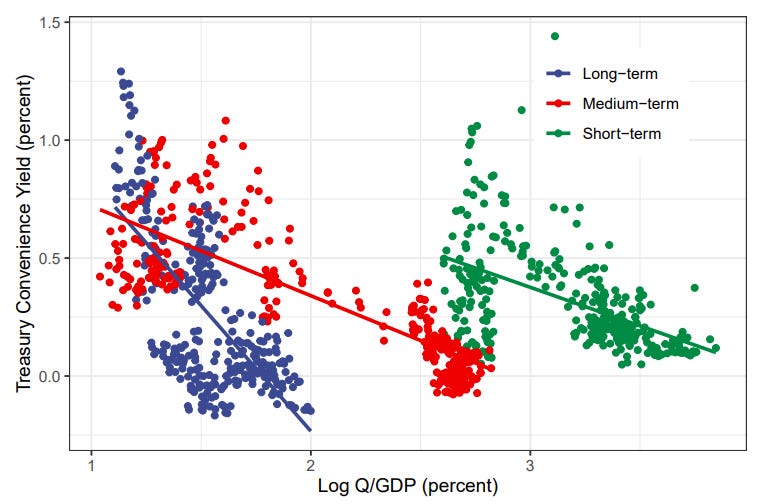

Convenience yields decline as US debt rises

Source: Jiang et al. (2025)

As the US debt-to-GDP ratio rose, the convenience yield of US Treasuries declined and eventually turned negative. The effect is stronger the longer the maturity of the Treasury notes, which makes sense since the probability of the US defaulting on its debt increases with time.

However, the fact that the convenience yield has turned negative also means that the US no longer benefits from the exorbitant privilege of borrowing at lower rates than other nations. Indeed, a negative convenience yield directly translates into higher borrowing costs for the Treasury in the future as it tries to finance its deficit.

And they are saying the death of US exceptionalism isn’t real…

Thank you for this analysis. As an American watching the decline in real time it stirs up many emotions. On one hand perhaps it's good the 'exceptionalism' is over. On the other, if there is a tipping point and the market really becomes to believe it is no longer a safe asset, could it start dumping it and trigger a real sell off/'crash' like sub-prime? The sad thing is neither US political party seem capable or even interested in getting debt under control, which may precipitate a crisis.

I agree. But what's the consequence? From my limited-visibility viewpoint, gold is now the quasi reserve currency and benchmark safe asset. Which is a negative, because the US was an institution, a de facto promise, and a growing "asset", while gold is something of limited use, with static potential.

And yet gold has the potential to become much bigger (with the downside of it possibly bubbling).