Real estate cannot move

As global weather gets more and more extreme and climate change extorts and ever-increasing cost on investments, it becomes clear that we all will have to react. Over time, we will have to adapt to climate change by avoiding areas that may become too hot to live or that may be flooded so often, that it makes no sense anymore to live there or use this land commercially.

This is all fine and well most of the time, but it isn’t that easy for real estate investors because, well, property does not move. So, if you invest in property, climate change and extreme weather become a problem long before they become a problem for most other investors. There is an increasing trend towards green real estate and I am a big fan of it and have explained the investment case for green real estate in a longer report I wrote about a year ago. However, green real estate mostly focuses on increasing operational efficiencies like the reduction of energy usage and waste generation rather than the impact of extreme weather on the location of the property. But now MSCI has published a good new study about this topic. They look at three kinds of climate risks on private real estate assets around the world.

In the United States, the main risk for real estate investors to consider is hurricane risk and concomitant floods triggered by storm surges. According to the specialists at MSCI, the states along the Atlantic Coast are the most exposed to these hurricanes and storm risks. In Florida, about one third of the capital currently held in direct real estate funds is at risk for total damage to investors of up to $7.4bn. Admittedly, the share of capital at risk is even higher in South Carolina and Louisiana, but these assets are only a small part of investor portfolios.

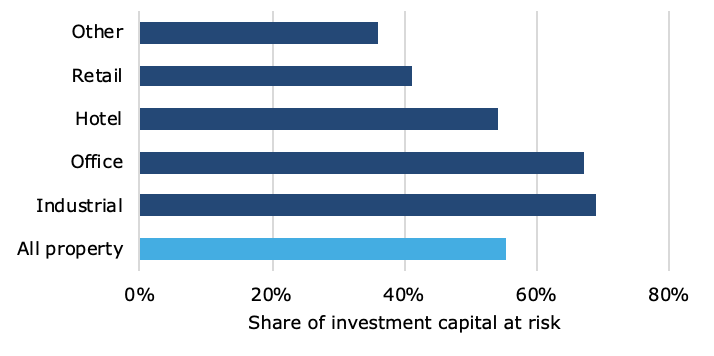

The biggest danger is, of course, another hurricane in New York City. Hurricane Sandy in 2012 provided a taste of what it would mean if a decent hurricane and storm surge hit the Jersey shore and New York City. Even though Sandy was “just” a category 2 storm, it was the second most costly hurricane in US history, causing about $70bn in damages. According to MSCI, about 29.3% of total real estate investments in New York state are at risk due to climate change. It is just a matter of time until these risks materialize and losses for real estate investors skyrocket.

Real estate investment exposure to hurricanes and storm surge in New York

Source: MSCI.

In the UK, hurricanes are luckily not a problem. Instead, the country has to deal with increasingly frequent floods. Current forecasts expect the number of households at risk of flooding to double by 2050 to almost two million. Ironically, the most expensive real estate in the country built right next to a major river is not really at risk. Thanks to the Thames Barrier, the world’s second-largest movable barrier that can protect London from storm surges as high as an eight-story building, the expensive property in central London is exposed to only very small flood risk. It is only if the Thames Barrier fails that London will be in trouble, but then it will be big trouble indeed. Flood risk is indeed much higher in the midlands and in the home counties that are densely populated but have little infrastructure to protect against floods.

UK property at risk from floods

Source: MSCI.

Finally, my friends in Australia have to deal with a very different kind of climate change risk, namely water stress, and droughts. A whopping 55.4% of capital invested in property in Australia is at risk from both baseline water stress (i.e. a decline of freshwater access and an increase in drought conditions) as well as increased intra-annual variability in the water supply (i.e. the risk of changing water supply within a year). Both of these risks are already materializing frequently today. Last summer, Sydney had to restart its desalination plant to provide freshwater to the city and New South Wales. This only happens when the level of water reservoirs drops below 60%. And while this ensures that Australians still have enough freshwater, it also means that their water costs skyrocket since freshwater from desalination plants is extremely expensive to produce.

Australian property investments at risk from water stress and intra-annual variability

Source: MSCI.

From the perspective of investors, there are only three ways to deal with the additional risks caused by climate change. Avoid the investment altogether (not a good idea given the stable returns with relatively low correlation to stocks and bonds), insure the risks, or lobby for better climate protection by governments. Insuring risks is still possible today, but as the experience of Hurricane Harvey and other major storms of recent years has shown, insurance companies cannot rely on their flood projections to price insurance contracts anymore. Thus, insurance companies have started to dramatically increase the price of flood insurance or have declined to insure certain high-risk properties altogether. Relying on insurance companies to protect against climate change risks thus seems to me only a medium-term strategy at best. The only sustainable solution to me is to become an activist investor in the sense that you lobby governments and local authorities to invest in infrastructure that helps mitigate and adapt to climate change. The Dutch with their dams have led the way, and London’s Thames Barrier is a great example of how one can protect people and property from adverse effects of climate change. We need to spend more money on such projects in the future and who better to lobby for them than the investors who own property in endangered areas. After all, their investments can’t move.