Should fund managers just stop touching their portfolios?

If your job is to manage money, you are used to being evaluated against the performance of a benchmark or your peers. And because most fund managers underperform their benchmark the community has become quite good at finding excuses. Racecar drivers are famous for their excuses for why they lost a race, but fund managers are almost as good. Here is a selection of excuses fund managers have made over the years:

There is a lack of diversity in thinking (Is it not your job to come up with something different?)

The big funds are dominating market prices (But who is selling when they are buying?)

Smart beta ETFs are ruining our strategy (Only if your strategy is doing something that can be replicated at low cost with an ETF)

Everything is going up at the same time (Then why is your fund down?)

It’s the Fed’s fault (Well, the Fed is certainly not going to go away any time soon, so deal with it)

“From the perspective of the fund’s performance, this lack of patience [by investors] – and this willingness to pay such a high premium for certainty around earnings – is unhelpful: the fund underperformed the index and its peers.” – Jacob de Tusch-Lec.

In other words, we were right, but investors bought the wrong stocks, so we underperformed. You cannot make this stuff up…

In the light of these lame excuses, there is one performance measure that even many professional fund managers do not know: Measuring your performance compared to a benchmark of doing nothing. This directly measures the contribution your active management has made to the portfolio.

The problem with this measure is that it doesn’t allow for too many excuses, though you can be sure, fund managers will find one.

Most of the time, this performance contribution compared to doing nothing is not publicly available or even calculated by fund managers. However, in the United States, it is possible to measure it thanks to the mandatory 13F filings a fund has to make each quarter. In each of these filings, the fund has to show how many stocks of each company it holds. While this misses short-term trades of stock being bought and sold within a quarter, it at least allows outsiders to estimate how much performance was created by the decision of the fund manager to buy or sell a specific stock.

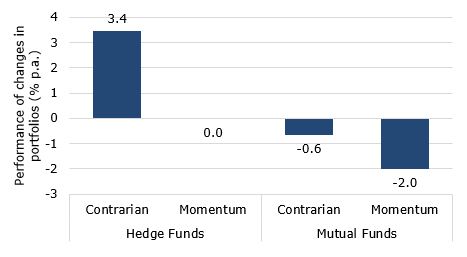

A 2016 study tracked the portfolio holdings of 589 mutual fund managers and 1,342 hedge fund managers between 1998 and 2012 to assess their ability to add value. In the process, the study classified fund managers into momentum investors, who tended to buy stocks that were rising in the past and sell stocks that were falling, and contrarian investors, who did the opposite. The chart below shows the average annualised return generated by these managers with their buy and sell decisions.

On average, contrarian fund managers were somewhat more successful than momentum-driven fund managers but only contrarian hedge fund managers actually added value by buying and selling stocks in their portfolio. The performance of mutual funds would have been between 0.6% and 2.0% per year better had the fund manager just sat there and done nothing. Not a flattering verdict for fund managers.

A closer look at their investment decisions shows that it typically is the stocks they sell that lead to the weaker performance. Quite simply, fund managers tend to sell stocks that afterwards have high returns. Momentum-driven hedge fund managers at least manage to buy stocks that compensate for this loss of performance, and only contrarian hedge fund managers have skill in the sense that they manage to pick stocks that show a strong recovery after they purchase them and sell stocks that decline in value after they sell them.

Annualised return added by fund manager decisions

Source: Grinblatt et al. (2016).

The funny thing is that the study could even check how fund managers and hedge fund managers traded with each other. The table below shows the average performance (per quarter annualised) of stocks bought and sold by different fund managers. The way to read the table is, for example, that the entry in the top left corner of the table is the average performance of stocks relative to the market (after correcting for size, value, and momentum effects) that were bought by both contrarian hedge fund managers and momentum-driven mutual fund managers. The number in the top row, second from left is the performance of stocks that were previously sold by momentum-driven mutual fund managers and bought by contrarian hedge fund managers, etc. Two things stand out from this tale:

Contrarian hedge fund managers tend to be on the right side of the trade whether they buy or sell stocks.

Momentum-driven hedge fund managers are wonderful counter-indicators. If they sell a stock, you should buy.

Performance of stocks bought and sold by different fund types

Source: Grinblatt et al. (2016). HF = Hedge Fund, MF = Mutual Fund.

Of course, this is just one element of the equation that goes into the final performance of the fund. It is what investors pay fund managers to do. On top of that come fund expenses, taxes, and systematic factor tilts that have been eliminated from this calculation (e.g. a fund manager may systematically prefer value stocks). Each of these factors has a significant influence on the bottom-line and can be both positive and negative. Hence, the numbers above do not tell us if a fund finally outperforms its benchmark or not, but it tells us that for most fund managers it would be better if they just quit their job or sit at their desk all year doing nothing. At least then, they would not cause so much damage to their portfolios.