So, you’re trying to manage inflation…

It’s Fed Day (again) and Jerome Powell and his colleagues at the FOMC are trying to manage monetary policy in such a way that they hit their dual mandate of low inflation and full employment. While trying to target the unobservable real risk-free rate (the infamous r*) one thing that can be measured is inflation expectations – even though there is not that much empirical evidence that inflation expectations have any meaningful relation to future inflation.

But if we follow conventional wisdom and assume that inflation is driven by actual behaviour of consumers and businesses in the real world, and that this behaviour is influenced or even determined by inflation expectations, then we have to ask how consumers form their views about inflation. I am on the record for criticizing all existing theories of inflation (whether they are monetarist, Keynesian or fiscally driven) for being based on rational expectations and discounting future cash flows into the present.

As I said in the article linked above, I think any theory of inflation based on rational expectations or discounting future cash flows is bound to fail in the real world because that is simply not how normal people on the street think and act. Instead, I think we need to develop a behavioural theory of inflation informed by real people and their actions in the real world.

While developing a behavioural theory of inflation is well beyond my capabilities, nor is it something that academics seem particularly interested in at the moment, I am glad to say that my view has received support from a new piece of research.

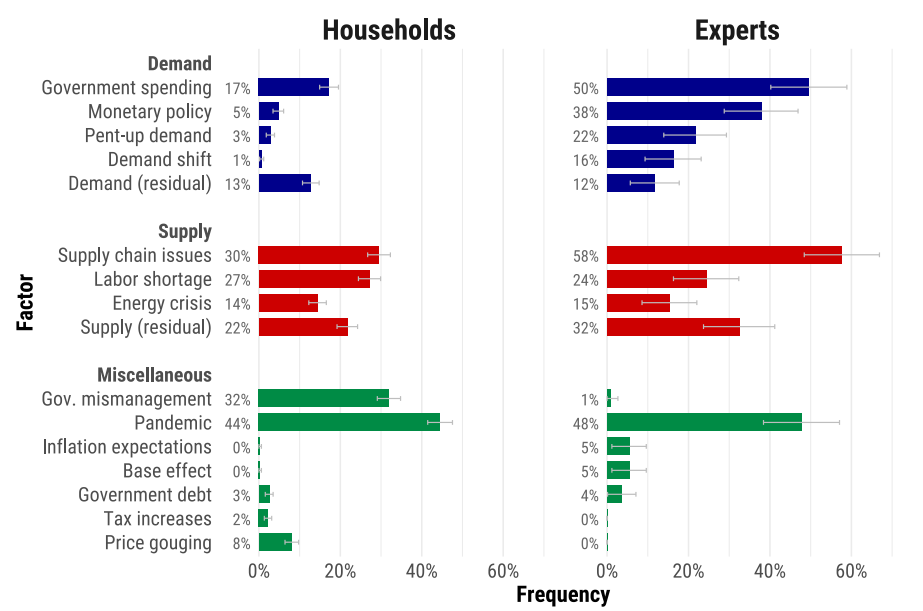

Peter Andre and his colleagues surveyed more than 10,000 US households and more than 100 experts about the recent surge in inflation and its causes. Below is the key chart from their paper showing the percentage of times different factors appear in the narratives about inflation of households and experts.

Drivers of inflation narratives

Source: Andre et al. (2023)

Let’s look at expert explanations first. The key drivers of the inflation spike in 2021-2023 according to experts was excessive government spending (in particular government spending during the pandemic), supply chain issues and monetary policy. These are the factors that I and every other economist have been debating for the last couple of years ad nauseam. Did the Fed keep rates too low for too long? How much inflation was created from the Covid support packages and the Inflation Reduction Act? How much of the price spikes in oil and other goods are due to supply disruptions? And so on and so forth.

Now, let’s look at how private households form their inflation expectations. Government spending and monetary policy by the Fed hardly featured as an explanation, showing up in just 17% and 5% of all answers.

If you ask households what caused inflation, they will tell you it was the pandemic, government mismanagement, supply chain disruptions and labour shortages. In essence, households form their inflation expectations based on what they experience in their everyday lives. Whether that is a shortage of goods on supermarket shelves or an inability to find qualified workers for a business. Government red tape or the disruptions experienced in pandemic lockdowns. This is what drives inflation expectations of real-life people, not abstract monetary or fiscal policy decided in Washington.

And if you ask me, as long as economists try to explain inflation through abstract actions taken in Washington that most people don’t know about or don’t understand, inflation models will continue to fail.

More importantly, as long as central bankers insist on trying to guide inflation expectations by providing forward guidance about future rate hikes or cuts and similar abstract measures only intelligible to experts, they will fail to influence real life inflation through managing inflation expectations. Instead, they just form their own echo chamber where central bankers talk to other experts about how they think the world works.

Perhaps it's also a matter of a new generation of people being asked who never really experienced inflation before recently?

An average German in the 1950s might have said: it's societal breakdown, and extremely high government debt due to reparations payments that cause inflation.

Me being a child of the sixties and seventies, I am on the lookout for a middle-east fueled oil crisis, and the resurgence of labor unions. Which is why lots of fellow boomers worry about Israel./.Hamas.

If folks focussed on the Pandemic, then there's little to worry about.

On the other hand, labor shortages caused by demographics are here to stay... (That said, Japan has had a tight labor for decades, in combination with deflation -- what gives?)

I work in tax consulting for small and medium-sized enterprises. This year, the margins of many pizzerias compared to variable costs have increased significantly. This means that they have increased prices without a proportional increase in raw materials. Also, the energy prices have been capped thanks to contracts at fixed prices from before 2021 and the government's interventions with large tax credits for energy expenses. I would like to do an experiment. In a time of low inflation, start a journalistic campaign in which a fake uncontrolled increase in prices is loudly denounced with fake statistical projections. It would be the spark that would create a cartel among retailers without any agreements but only on the basis of a collective consciousness that would feel authorized to increase prices without real reasons. This is what happened in Italy with the transition to the euro. 1 euro = 1936.27 lire. But retailers and restaurant etc, decided to simplify it to 1 euro = 1000 lire, in the name of simplicity everyone felt authorized. So what was priced 1000 lire became 1 euro instead of 50 cents, while wages suddenly saw their purchasing power halved. It was a great opportunity for the Italian government to reduce public debt, but it was instead used to increase it.