Stability seems to be key

Last Monday, I wrote about a study that examined the performance of ESG momentum portfolios. The same study also examined another approach to ESG investing that I have never considered myself before. But it does sound interesting.

Investments based on ESG momentum rely on companies improving their ESG credentials and thus reducing nonfinancial risks over time. But instead of investing in companies with the largest improvements in ESG credentials, one can also look at the companies with the most stable ESG ratings.

A company that is consistently good at managing its nonfinancial risks should have fewer accidents and fewer losses due to lapses in environmental standards etc. The better a company is at managing these risks, the less investors must worry about them. Over time, the risk premium placed on the company’s shares by investors will drop simply because investors have increasing confidence that the company knows what it is doing. In a way, it is minimum volatility investing translated into the ESG world.

In theory then, companies with less volatile ESG ratings should have higher share price returns than companies with more volatile ratings (especially if that volatility is created by downgrades in the ESG rating).

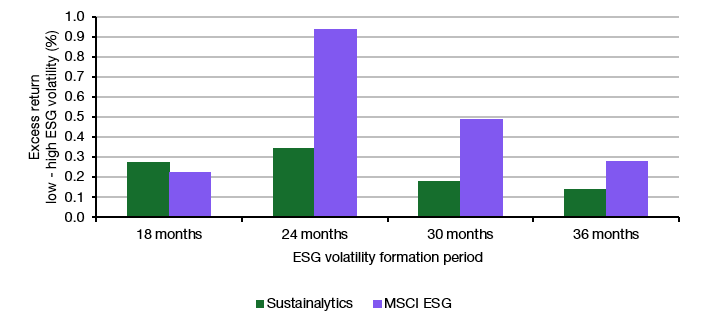

The chart below shows the result of investing in the 20% of companies with the lowest ESG rating volatility and shorting the 20% of companies with the highest ESG rating volatility. Again, several lookback periods for measuring ESG volatility are tested for both Sustainalytics and MSCI ESG ratings.

ESG low volatility strategy performance based on Sustainalytics and MSCI ESG ratings

Source: Guidolin et al. (2023)

Luckily, this time there is no contradiction between the two ratings agencies. Companies with less volatile ESG ratings outperform companies with more volatile ones by 0.2%-0.3% per month or 2.5%-3.5% per year. Of course, this is before transaction costs but luckily, stable ESG ratings mean that there won’t be many changes over time in these portfolios so not much of this performance will likely be lost to transaction costs and other frictions.

And given that it matters less which ratings provider an investor chooses for this strategy than for an ESG momentum strategy, it might be a worthwhile approach for ESG investors who do not have the resources to examine all the details of every investment they make.