Stock index weights are … different

One of the things that I do instinctively every time I look at short-term movements is to check if the performance of markets is “consistent”. What I mean by that is that on a risk-off day when markets decline and safe assets are in demand, I would expect stock markets with a higher weighting in cyclical sectors to underperform markets with a higher weighting in defensives. Differences in sector composition can explain why the Swiss stock market with its high weighting in food and pharmaceutical companies tends to outperform in a down market while the German stock market with its high weighting in cyclical stocks tends to outperform in a bull market.

Another simple check is to look at oil prices. On days with declining oil prices, markets like the UK should underperform Europe or the United States, which have a lower weighting in energy and mining stocks. And if the relative performance of markets doesn’t add up, something strange is going on and I need to dig deeper to find out.

In that respect, markets have behaved pretty much as expected over the last month or two with the UK market being one of the weakest markets worldwide due to its exposure to energy and mining.

But when I checked sector weights of different indices, recently, I noticed that the current market crash has dramatically shifted the sector exposures of different markets. Let’s start with the S&P 500, which is one of the most diversified indices in the world. We all know that today, the biggest sector in the S&P 500 is the IT sector. Before the financial crisis it was financials, in the early 1980s it was energy, and in the 19th century it was railroads.

But look at the shifts in sector composition over the last 12 months. Not only is It the largest sector in the S&P 500, but one in four Dollars invested in the index is effectively invested in the IT sector today. A year ago, it was just one in five Dollars. Meanwhile the two smallest sectors are mining and energy, which together make up less than 5% of the index. If you hold an S&P 500 ETF today, only one out of every 40 Dollars of your investments is in mining stocks and another one in oil and gas companies.

Sector weights in the S&P 500

Source: Bloomberg.

Most of these shifts are due to the last few weeks. The chart below looks at the shifts in sector composition in percentage points since the beginning of the year. If you invest in the S&P 500 the massive underperformance of banks and oil companies means that you are now investing about two percentage points less in these sectors and instead about 2 percentage points more in IT, and one percentage point more in both health care and staples. Your index investment has become more defensive as markets have sold off. And while that protects you from any further downside, it also means that when the market eventually starts to recover, your investment will be the most defensive it has been since the beginning of the crisis.

Change in sector weights in the S&P 500 since the end of 2019

Source: Bloomberg.

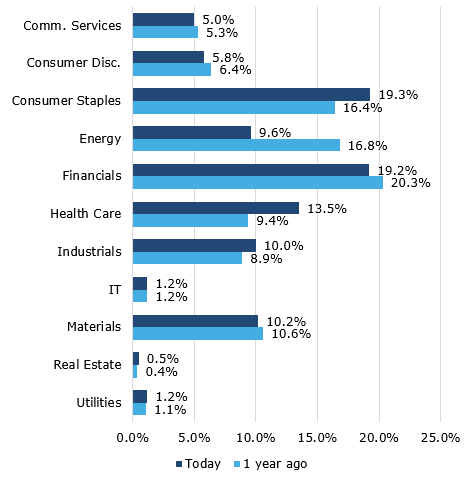

For a well-diversified index like the S&P 500, these shifts in sector weights are relatively small, but the more concentrated an index is, the bigger these shifts. The FTSE 100 index in the UK was exposed to four main sectors a year ago. 15% in consumer staples like British American Tobacco or Unilever, 20% in banks like HSBC and Barclays and 25% in oil and mining stocks like BP and BHP. Together these four sectors accounted for 60% of the index. But if you look at the sector composition today, it is vastly different. The exposure to energy has dropped from 17% to 10% in a year while health care has increased from 9.4% to 13.5% and is now the third-largest sector in the FTSE.

Sector weights in the FTSE 100

Source: Bloomberg.

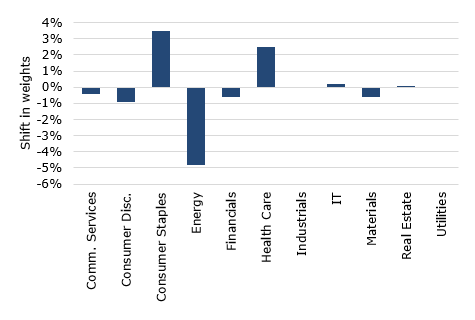

Again, most of the sector shifts have happened over the last couple of months. But there is no denying that the FTSE today is much less of an oil index than it was just three months ago. Since market indices are based on the market value of their index constituents, they do not rebalance (well, they do every year or twice a year when the index weights are reset, but that is not a rebalancing to previous levels).

Change in sector weights in the FTSE 100 since the end of 2019

Source: Bloomberg.