The changing impact of divestments

The changing impact of divestments

I have been an outspoken opponent to divestment campaigns. My argument is that if you divest from a fossil fuel company, for example, you are just selling your stocks to people who care less about these issues than you do. Better to invest and instead engage with company management to put pressure on them to change. Advocates of divestment campaigns have argued that if enough people divest from a stock, the share price will suffer and force corporate management to change. To which I replied that so far, the empirical evidence was not in their favour.

But the times they are a’changing. By now divestment campaign have become so large and widespread that new studies show a clear short- and medium-term impact of divestment decisions on the share price of energy companies. A reader pointed me to the research by a group of academics at the University of Augsburg that showed that European energy companies with higher selling pressure from divestment campaigns have lower share price returns and subsequently reduce their carbon emissions more aggressively.

Another research paper from the University of Waterloo in Canada showed that when adjusted for underlying changes in the oil price, energy companies have lower share price returns after publicly announced divestments by major institutional investors than the rest of the market.

Effect of divestment events on share price when adjusted for oil price changes

Source: Dordi and Weber (2019)

So here I am, publicly revising my opinion on divestment campaigns. By now, the divestment trend has become so large that it indeed does what it intends to do. It puts persistent pressure on the share price of targeted companies and thus forces company management to reduce their carbon emissions. Well done.

…except that this leaves investors with a problem in their portfolios. If they divest from fossil fuel companies, they effectively put a massive underweight on the energy sector in their portfolios. That is fine as long as oil and gas are in a secular bear market like the one we have lived through over the last decade. But what if oil and gas prices rise? We have just witnessed a massive surge in energy prices over the last six months which has led to significant underperformance of portfolios that did not include oil and gas companies.

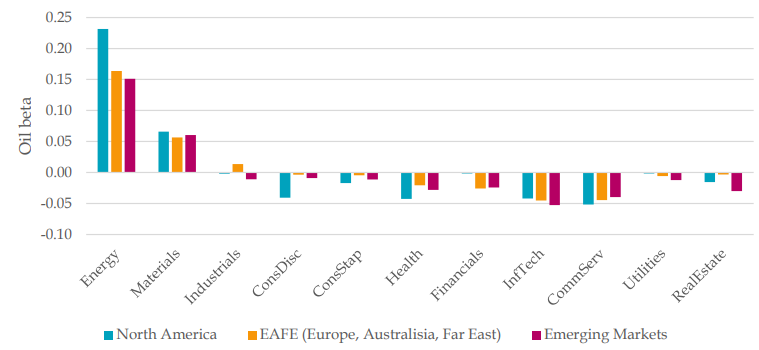

David Blitz showed recently that no matter which region you look at, divesting from oil and gas stocks creates a large bet on falling oil prices in your portfolio. And there is no real way to hedge against this risk since the only other sector with significantly positive share price beta to oil prices is the mining sector. And many ESG investors don’t like those stocks either because these companies have large carbon footprints as well.

Share price beta to changes in oil price across sectors and regions

Source: Blitz (2021)

If you ask me, feel free to divest from oil and gas if you like, but be aware that you are not doing your portfolio a favour. I think it is still better to not divest but instead engage with company management as a shareholder.

Beware of the unintended consequences but before I say something and ideologues jump down my throat I very much look forward to the day when fossil fuels are an element of history. Now however this is not possible.

Due to divestment, not just of share portfolios, but restrictions in capital as banks, especially Euro domiciled, there is no green or brown field investment the rate of reserves is now plummeting and resource companies are being cut off from capital markets on both the equity and the debt side.

We at present do not have the technology to generate, let alone store, the energy that fossil fuels provides. There is an irrevocable nexus between energy conversion and quality of life/GDP/mortality and a range of factors many would consider rather important.

Further complicating affairs is that should we somehow possess by instant miracle the technology and the capacity based on existing core technologies then we have NOWHERE near the resources to build it anyway. Oh and BTW many of these resources that we do possess are located in China and Russia.

So a further consideration of engagement over divestment one also needs to consider the benefit of engineering possibility and practicality over ideology and twitter trend following of the uninformed masses.

The way things are going $140/barrel oil is not even on the expensive end of where energy prices can go. Whilst demand is flatlining due to efficiency and some greener energy options it is the precipitous cliff of supply that will determine prices in the next 5-10 years.

Just watch Germany crumble if Putin cuts off the gas, they have divested coal and nuclear, cut of France (nuclear) from their grid and relied on renewables and gas. This one factor has greater short term financial risks to the globe than the invasion of Ukraine, humanitarian issues notwithstanding.

I wish for a cleaner better world, I just want to be able to cook the kids dinner and read them a book by bedlight in the evening.

Interesting, thank you, Klement! I wonder about the overall effect, though: If Shell stops to produce oil, will that really lead to higher oil prices and (therefore) lower consumption or will other oil companies fill the gap?

The most likely scenario is that Shell would sell its oil operations to another company, isn't it? So there probably isn't much to be gained for the environment here, is there?

And let's make the (wild) assumption that all publicly traded companies stop producing oil: Wouldn't private equity fill that gap as long as there is demand for oil? Granted, PE might look for higher margins which would probably lead to higher prices (unless they can buy oil operations for cheap).

My current understanding is that reducing oil consumption (e.g. by pushing forms of transport that use less or no fossil fuels) is more effective than making individual oil companies change their way of doing business. But maybe I'm wrong. :)