The decline of ethics

Ok, I am going to sound like a grumpy old man in this post, but let’s face it, our society is going down the drain anyway, so I might as well say it.

One of the things, I am keenly aware of when interacting with other people is how ethical and principled they behave. I guess my experiences of working in the IT industry during the tech bubble in the late 1990s and then in the financial industry during the financial crisis have been traumatising. I immediately notice if a company or a person I meet not so much acts unethically, but is willing to bend the rules. And having worked in different companies within the financial industry, I noticed how different the culture can be from firm to firm and from job to job.

Financial advisers don’t always have to follow the fiduciary rule and as a result, sometimes don’t even have a legal obligation to put their clients first. Meanwhile, as a person with both a CFA and a CFP working in the UK, I have three institutions (the FCA, the CFA Institute and the CFP Board) forcing me to fulfill my obligations as a fiduciary. And I can be sanctioned by any of the three if I misbehave.

But when it comes to ethics in our profession, there is sadly a constant pressure both on regulators and credentialing organisations to soften the required standards. Just think of the Series 66 examination in the United States. This exam is required for financial advisers who want to give investment advice to private investors. The exam consists of an ethics part and a technical part that asks questions about stocks, bonds and other investment instruments.

If you are an adviser who took the test before 2010, the ethics part had a weight of 80% in the test. But in 2010 (notably, two years after the financial crisis) the weight of the ethics part was reduced to 50%. The contents of the test were still the same, only the weighting changed. And as advisers studied for the test, they focused less on ethics and more on the technical part, with the result that incidents of misconduct by financial advisers increased after the test changed. A recent study showed that advisers who took the test before 2010 with the higher weighting on ethics, were about one fifth less likely to be fined for misconduct than advisers overall. If the sample is restricted to obvious cases of misconduct like fraud, theft, and deceit, the gap in ethical behaviour is even bigger.

Frequency of ethical misconduct of financial advisers in the US

Source: Kowaleski et al. (2019).

It is often argued that such ethics exams don’t really work because students study for the exam and then forget the things they learned afterwards. But the research shows that this is not the case. Even though advisers had to sit for the exam only once and never had to refresh their license, their conduct remained more ethical years after the exam. And advisers who passed the old exam were more likely to quit companies with a less ethical work culture. What seems to happen is that merely being exposed to ethics questions acts as a prime to reflect on your own behaviour. As a result, advisers should regularly be exposed to ethics tests to make them aware of their obligations to their clients. And ideally, the ethics part in exams and continuing professional development should have the highest weight possible to emphasise the importance of ethical professional conduct.

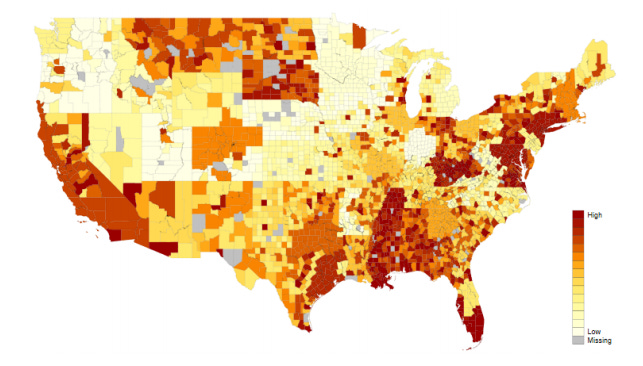

Unethical behaviour has many sources. We know from other research that financial advisers who grow up in counties where unethical conduct is more prevalent will be more likely to act unethically as adults. A study by Christopher Clifford, Jesse Ellis, and William Gerken looked at 86,000 FINRA registered financial advisers in the United States and found that an adviser born in Staten Island or in Queens was about seven times as likely to engage in misconduct during his career than someone who was born in Douglas County, NE, or Lake County, IN. The map below shows the misconduct index of the United States corrected for other factors that can influence misconduct rates like income or religiosity. What this map tells us is that if you deal with a guy who grew up in Queens and made his money in an investment-related industry where shady deals are more common than not, it’s quite likely he will try to screw you. If only I had known sooner…

Misconduct rate by the birthplace of financial advisers

Source: Clifford et al. (2019).

As you might expect, ethics training is a corrective force to learned ethics (e.g. from childhood experiences). But ethics training is unable to overcome the learned ethics of a person. No matter how much training a person gets, if you hire an unethical adviser, you will face a higher likelihood of being cheated.

And now think about the environment that people live in today and that children grow up in. We used to live in a world where rogue traders went to prison and fraudulent CEOs of companies did so as well. But over the last twenty years, we first became used to senior managers not being held accountable for their wrongdoings in the run-up to the financial crisis and now we have entered a stage where unethical behaviour of politicians not only goes unpunished but is considered acceptable behaviour. Meanwhile, senior executives of large companies can evade justice in a way that we only saw from criminals in the past. Yet, nobody seems to care.

What we have done over the last decade or two is teach young professionals that it is OK to bend the rules and cross the line to unethical behaviour because even if you are caught, it is unlikely you will be punished for it. And we are in the process of teaching our children that unethical behaviour is not only OK but helpful for your career. It is clear to me that misconduct rates in the financial industry are in a secular bull market unless we do something against it and introduce more ethics requirements for advisers and requirements for regular continuing education in ethics and professional conduct where this is not already the case. Advisers whine about having to pass so many exams and trainings that keep them from doing their job, but what the data on ethical misconduct of advisers tells me is that we are by far not doing enough.