The fundamental problem for every investment adviser

If you are an investment adviser to private investors, you will know that one of the most common problems you face is to convince your clients to invest more in equities – especially if they are older. Investing too defensively has significant long-term consequences in the form of lower retirement savings and an increased likelihood of running out of money during retirement.

Back in my days in wealth management I sometimes asked a room full of clients to raise their hands if they think equities are riskier than real estate. Then I asked them to raise their hands if they thought real estate or equity investments had a higher return.

Apart from the real estate crash of 2007 to 2009, the majority of people said that equities were riskier than real estate, but real estate was more profitable than equities. But if you think about it, it will mean that by investing in real estate, you can systematically get higher returns for lower risk. Why bother with equities then?

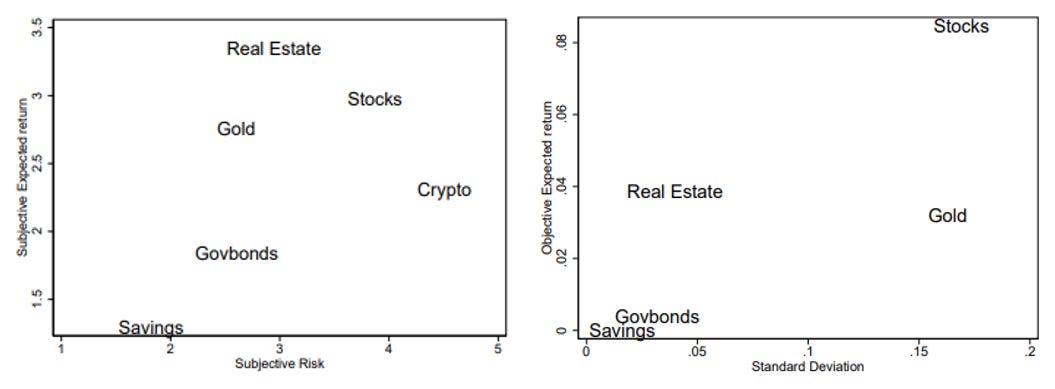

The chart below is from a study by researchers from the University of Hong Kong. It shows the perceived risk and return for different asset classes on the left and the true risk and return on the right. Note the odd position of gold and real estate in the left-hand chart. Not only do private investors believe that real estate is superior to equities, but they also believe that gold has about the same returns as stocks but is much less risky.

Investor beliefs about asset classes (left) and the true risk and return trade-off (right)

Source: Jo et al. (2022)

Of course, if people think that real estate and gold are so much better than stocks, it is no wonder they are reducing their equity investments in favour of both real estate and gold. But a look at the right-hand chart above, it is clear that this roughly halves the expected return of the investments that have been moved from equities to real estate or gold.

There are many reasons why private investors perceive real estate as less risky than equities. One is the lack of daily pricing. People simply don’t see the daily fluctuation in the price of their property investments, but they do see the daily fluctuations of stocks in their portfolios. But they can also see the daily fluctuations of the price of gold, yet they still feel gold is less risky than and as profitable as equity investments.

The study I mentioned above investigated this phenomenon a bit deeper and found that the key problem is not the perception of risk which is only slightly misaligned. Instead, it is the belief that riskier assets have lower returns. Private investors vastly underestimate the true returns of highly volatile investments because they viscerally feel the losses in a bear market, but they don’t enjoy the gains in a bull market that much. Once again, it is loss aversion and prospect theory that explains the misalignment of investor beliefs.

The risk-return trade-off as perceived by investors

Source: Jo et al. (2022)

But if investors are roughly correct in their perceptions of the relative risks of different asset classes but underestimate returns, I wonder if the industry is doing the right thing when it focuses heavily on educating private investors about the long-term risks of equities. One of the most common approaches to convince investors to increase their equity allocation is to preach about “equities for the long run” and how the probability of losing money declines over time (which, by the way, is not necessarily true as I discuss here).

But maybe we should put more emphasis on educating private investors about returns and especially the relative returns between asset classes? Just a thought…

Klement, Tell me you aren’t ashamed of yourself. Real estate as an asset class is “normally” valued based on the buy/sell ratio normalized by years held. Excluding income and as the other commenter said, excluding leverage. Whereas the point of real estate is that it pays for itself. It pays its mortgage down to zero thus ultimately its cost was only the down payment, which itself can be zero (e.g., 20% seller financed). And it pays the owner continuously, so you can go buy more properties, or retire early. Plus it reduces your taxes potentially to below zero with depreciation. Selling it on the last day is not necessarily the entire value of the whole proposition. An investor buying a retirement income might reasonably not care at all about the selling price, so long as the thing keeps paying income forever during life. An indexing argument, TomVeatch.com/re, suggests 85% of wealth should be held in the form of real estate. The indexing argument has come to thoroughly dominate the stock market but is curiously (self-servingly) ignored in discussing the relative investment value of stocks and real estate. The stock flogging consultancy industry represents falsely and repeatedly (as you have done in this posting) that real estate as an investment is inferior to stocks. Which it is, only if you take out the income and the leverage and the depreciation. Which is stupid, or misleading, or criminally fraudulent. So please acknowledge that in this posting, which amounts to a one sided and false polemic against real estate, you have removed its important benefits from the argument, and misled your audience from seeing the important generalization, the truth itself: that which would direct their lifetime of effort and saving to their own greatest long term benefit, rather than to the benefit of the stock selling financial industry.

Or tell me why I am wrong. I’ve stated it strongly but I’d be happy to be wrong — I’d like to know it!

Thanks for sharing that study. Your article is as educating as usual.

One more thought/question: I agree that investment advisors should focus their efforts on (generally speaking) getting the most for the client. What is the right way, when I really educated my client correctly and he or she is still not convinced? Is it the duty of the advisor to fullfill the ‚mistaken‘ plan, knowing up front that it’s probably not going to work out? Should we argue further at the risk of losing the client?

I am of the opinion that after having advised the client our duty is done. If she decides not to listen, that‘s on her. But often I feel very alone with this view (in opposition to some/many advisors giving the client whatever she wants to hear…).