The long run is lying to you – or is it?

In March last year, Cliff Asness wrote a note called “The long run is lying to you”. In it, he defends value investing by emphasising that what drives return is not the current valuation but the change in valuation. And because value stocks are particularly cheap vs. growth stocks these days, any improvement in the relative valuation of value stocks vs. growth stocks leads to higher returns for value vs. growth. Now, the concept is nothing new under the sun. In the 1980s Jack Bogle already popularised a simple way to estimate future equity returns as dividend income + earnings growth + change in valuation. And every bond investor knows that the total return of a bond is approximately its interest income plus its duration times the change in yields.

But Cliff’s simple way of looking at the market still is a good approximation and his notion that value is very cheap vs. growth is correct. I think value will outperform in 2022 vs. growth and unlike in the United States, value has already outperformed in the UK and Europe last year. But do I think that value will outperform over the next 3 to 5 years? No.

The reasons are manifold but here I would like to use an argument similar to Cliff’s about changes in valuation that I haven’t used before. Equity markets are discounting machines and the fair value of equities is driven by future cash flows discounted to the present. But because future cash flows are nominal quantities (i.e. they include inflation) that are discounted by nominal discount rates (which also include inflation), the inflation component in a discounted cash flow model cancels out. Similarly, if you use the price/earnings-ratio or the CAPE to value stocks, inflation enters both the price component as well as the earnings component. Thus, the thing that matters for equity valuations are real rates, not nominal rates. Higher real rates should lead to lower valuations and lower real rates should lead to higher valuations. And while Cliff and his colleagues at AQR don’t believe that rate changes have anything to do with value outperformance they only test the impact of nominal rates, not real rates. And my own research from a decade ago was very clear about the relationship between CAPE and real rates. Real rates proved to be significant at the 1% level in determining CAPE levels.

Now, I will restrict myself to stock market valuations overall here rather than valuation differences between value and growth stocks simply because there isn’t enough space to cover all of that. I want to mention though, that I subscribe to the notion that most value stocks are value stocks because they have lower growth expectations than growth stocks and thus the share of the present value of future cash flows far in the future is lower than for growth stocks. Thus, if interest rates rise, value stocks should suffer less than growth stocks because they have more of their present value closer to the present (i.e. they have shorter duration) and thus in a time of rising real rates, value should outperform growth.

Whether you believe that argument or not, looking at real rates in different countries and stock market valuations overall will at least be relevant to the discussion if US markets will have to suffer a larger decline in valuations than European or UK markets if real rates rise. Thanks to the data of Paul Schmelzing, we can look at the current level of real rates in different countries vs. their long-term trend. If real rates are below their long-term trend, they should eventually rise, pushing valuations down. If US real rates are likely to rise more than UK or European real rates, then US markets should devalue more than UK and European markets and underperform.

The chart below shows the rolling 7-year average of real rates in the UK and the United States since 1980. As you can see, there was a general downtrend starting after the Volcker rate hikes and current real rates are roughly where the trend says they should be.

Real rates in the United States and UK since 1980

Source: Liberum, Schmelzing

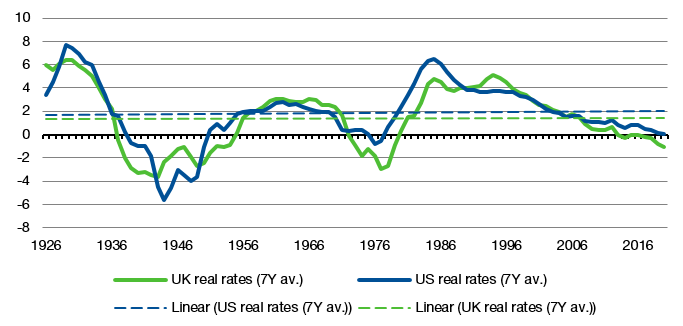

Ok, but that obviously ignores the period of the 1970s and in fact many would argue that this is a long-term decline in real rates that is not representative of the true long-term behaviour of interest rates. It is “common knowledge” that interest rates are mean-reverting and they eventually have to rise to long-term averages. So let’s look at real rates since 1926 when the famous Ibbotson and Fama-French data starts. The time period since 1926 is commonly used to identify long-term trends in valuation risk premia, interest rates and the like. And what could be wrong about that? It is almost 100 years of data, so it should be a true long-term view that doesn’t lie to us. The chart below shows real rates since 1926 and based on this long-term view, real rates today are truly too low and should rise going forward. However, they should rise about the same in the United States and the UK, so no real advantage for UK over the United States from this perspective.

Real rates in the United States and UK since 1926

Source: Liberum, Schmelzing

But my claim is that the long-term picture of using 1926 is lying to you. Because when it comes to interest rates, you are not constrained by a lack of data pre-1926. So you can go back much further in time and check how interest rates behaved in the very long run over centuries. I can already hear the outcry from stock investors who say that such ultra-long time series have no relevance since markets are different today than they were a couple of hundred years ago. But then why do we use data from before WW2 to identify long-term trends in equities. Why do we use data from the 1970s when the economy was very different from today? If we are only using trends in markets that are similar to our current ones, we need to restrict historic data to the period of globalised free capital markets after the opening up of emerging markets and former socialist countries for global trade. So we should only use trends starting in the 1990s or 2000s and these trends all say that current real rates are roughly where they should be and there is no argument to be made that real rates should rise or stock valuations decline.

Finally, let’s take all the data we have and calculate the long-term trends in real rates in the United States and the UK. The result is shown below. To give you an idea about the numbers, real rates are currently very close to these long-term trends but slightly below. In order to get back to trend, real rates would have to rise by about 0.7% to 0.8% in the United States and the UK. And that is roughly what I expect to happen this year. So, overall, I think valuations may come down this year as real rates rise, but the long run is not in favour of significantly lower valuations in the United States or the UK. At least not if you look at the fundamental drivers of the economy.

Real rates in the United States and UK using all available historic data

Source: Liberum, Schmelzing