The long-term impact of low interest rates on company balance sheets

I know we are debating in the United States and the UK when the central bank will stop buying additional government bonds but if we are honest, no one who should be taken seriously currently expects long-term bond yields to go through the roof. We will face several more years of very low bond yields compared to historical averages.

All of this is done to incentivise businesses to borrow money and invest it for future growth. And on average that is what low bond yields do, though to a much smaller degree than central bankers would like. But as the old joke goes, an economist is someone with his head in the oven and his feet in the fridge, saying “on average, this is quite comfortable”.

The problem with low bond yields is that the impact they have on companies is very different. And once more, we can and should learn from Japan where we have more than two decades of low interest rates to teach us how business leaders take advantage of them.

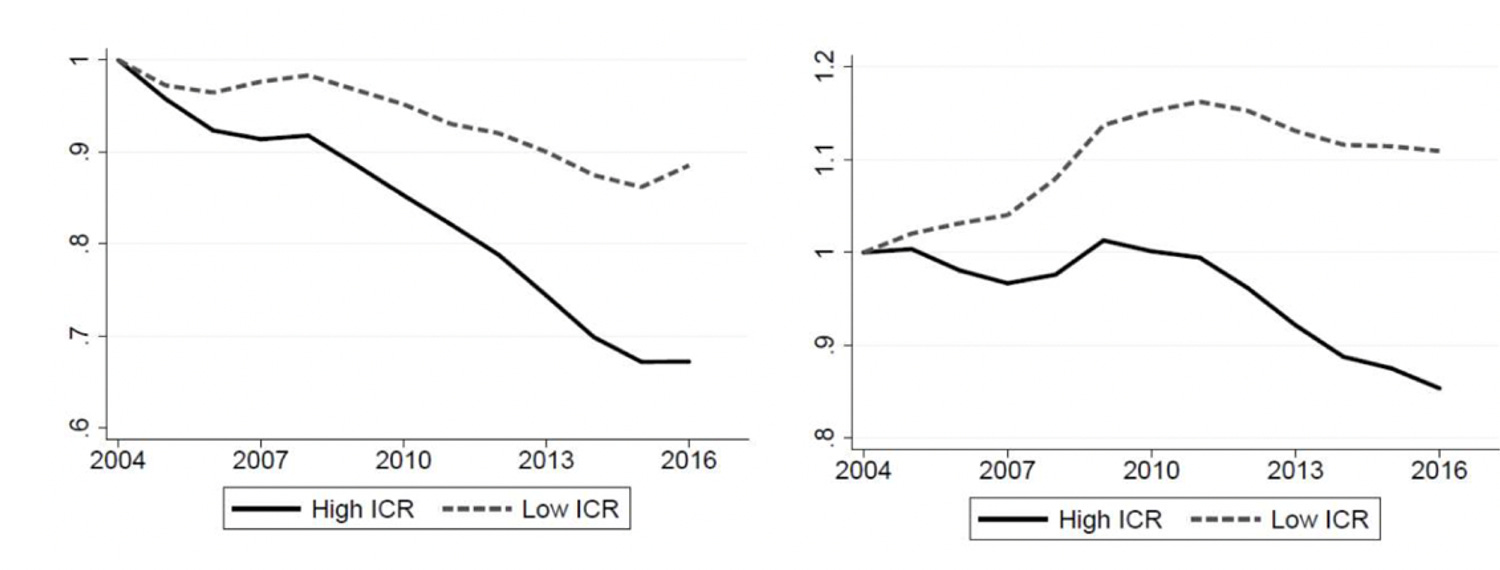

One key driver of corporate behaviour with respect to long-term bond yields is the interest cover ratio of the company. Most companies (even in Japan) have an interest cover ratio (ICR) above one, that is their operating earnings cover their interest expenses and more. But there is a substantial minority of companies (in Japan it is currently about 15% of all businesses) that are zombie companies in the sense that their operating earnings aren’t sufficient to even cover the interest expense on their outstanding debt.

In an environment of low short-term and long-term interest rates, these two types of companies behave very differently. High-ICR companies with profitable businesses tend to take advantage of low interest rates and invest in future growth. While this may mean taking out loans in the short term, over time, the investment in future growth will create additional profits to pay back the outstanding loans and debt and delever the balance sheet. Meanwhile, low-ICR companies that can’t even cover their interest expense don’t invest. And rightfully so, because if you take out a loan to invest in an already unprofitable business, you are just making your situation worse. Instead, the best thing you can do is to replace short-term debt with long-term debt to lock in the low interest rates for as long as you can. As the two charts below show, this is exactly what happened in Japan. Profitable high-ICR companies invested in their business and reduced their debt over time, while unprofitable low-ICR companies just shifted short-term debt into long-term debt.

The impact of low long-term rates on corporate balance sheets. Short-term debt on the left, long-term debt on the right

Source: Igan et al. (2021)

In the long run, this increases the difference between zombie companies and profitable companies in several metrics. Profitable companies invest in future growth and create large amounts of shareholder value while zombie firms just shift debt from short-term to long-term and continue to slowly erode shareholder equity. Thus, paying attention to which company is able to cover its interest payments with its operating profits and which is not, is a key factor to understand if you want to invest in companies that will do well over the next five to ten years.

Change in balance sheet due to low interest rates

Source: Igan et al. (2021)

Fascinating article, Joachim! I started reading about investing and doing it part-time (because I automate most of it via SIPs) a few years ago. A few months later, I came across the interest coverage ratio as a means to evaluate solvency. It has been a good, quick check for me to analyse companies, ever since. However, looking at how low borrowing rates have an impact on companies with differing ICRs is eye-opening.

You've talked multiple times about how low interest rates are here to stay for a while. Does that make the interest coverage ratio an even more valuable tool? And how do higher interest rates affect high ICR companies vs low ICR companies?