The Renminbi is getting more important, but…

On Tuesday, the Bank for International Settlement (BIS) published its triennial survey of global FX and interest rate markets. The survey is worth looking at because, well, it comes around only every three years.

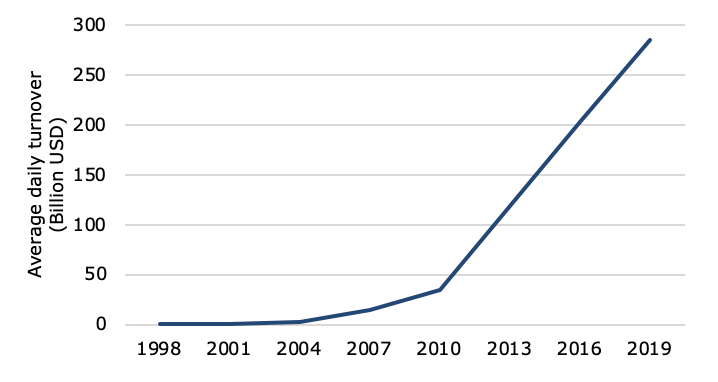

What I find interesting about the survey is to look at the rise of the Chinese Renminbi (CNY) as a global currency. There are a lot of people out there who think that with the rise of China the US Dollar may lose its status as the world’s reserve currency to the Renminbi. One necessary condition to become a major reserve currency is to have a deep and liquid market. And indeed, the average daily transaction volume in the Renminbi is growing at breakneck speed. Since 2010, the trading volume in Renminbi has grown by about 26% per year on average. Compare that to the 6% average growth rate in US Dollar transactions and you understand that the Renminbi is catching up fast.

Average daily trading volume of Chinese Renminbi

Source: BIS.

Today, the average daily transaction volume in the USD/CNY is $269 billion. That is almost as much as the $287 billion in the USD/CAD and quite a bit more than the volume in the USD/CHF.

But before you get too worried about the rise of the Renminbi to world dominance, it is necessary to put these numbers into perspective. And that is where the but comes in.

The share of the Renminbi in the global currency markets is a mere 4.3% today. Compare this to the 88.3% market share of the US Dollar and you understand that we are a long way from the Renminbi becoming a serious contender for global reserve currency. At the moment, the Renminbi is the most traded emerging market currency in the world but still only the eighth most traded currency overall, quite a bit behind the Swiss Franc and the Canadian Dollar. Thus, arguing that the Renminbi could become the world’s reserve currency is like arguing that the Loonie or the Swiss Franc could become the world’s reserve currency. It’s a bit premature.

Global market share by currency

Source: BIS.

But of course, transaction volumes in the Renminbi grow much faster than in the US Dollar. If we extrapolate the average growth rate of the last ten years into the future, then the Renminbi would overtake the US Dollar in 2037 or so. But even that might be an optimistic assumption because as with every new market, growth rates slow down as the market matures and base volumes increase. If we assume that the US Dollar and the Renminbi grow at the same pace as in the last three years, the Renminbi would overtake the US Dollar only in 2050 or so. That’s about the time when the Renminbi can become a serious contender for global reserve currency.

But that does not mean it will automatically become the global reserve currency. There are significant political hurdles to overcome. The US economy was much larger than the British economy and the US Dollar as prominent in global currency markets as Sterling for many decades before the US Dollar replaced Sterling as the global reserve currency. In fact, it took the Second World War to get that far. And given this historical precedent, I am inclined to say that the Renminbi is not going to replace the US Dollar as global reserve currency in my professional career and possibly not in my lifetime.