The sad state of public pension plans in the US

I recently came across a fascinating paper from the Board of Governors of the Federal Reserve that investigated the financial situation of public pension plans in the US and their reaction to low interest rates. In three simple charts this paper clearly demonstrated the dire straits public pension funds are in.

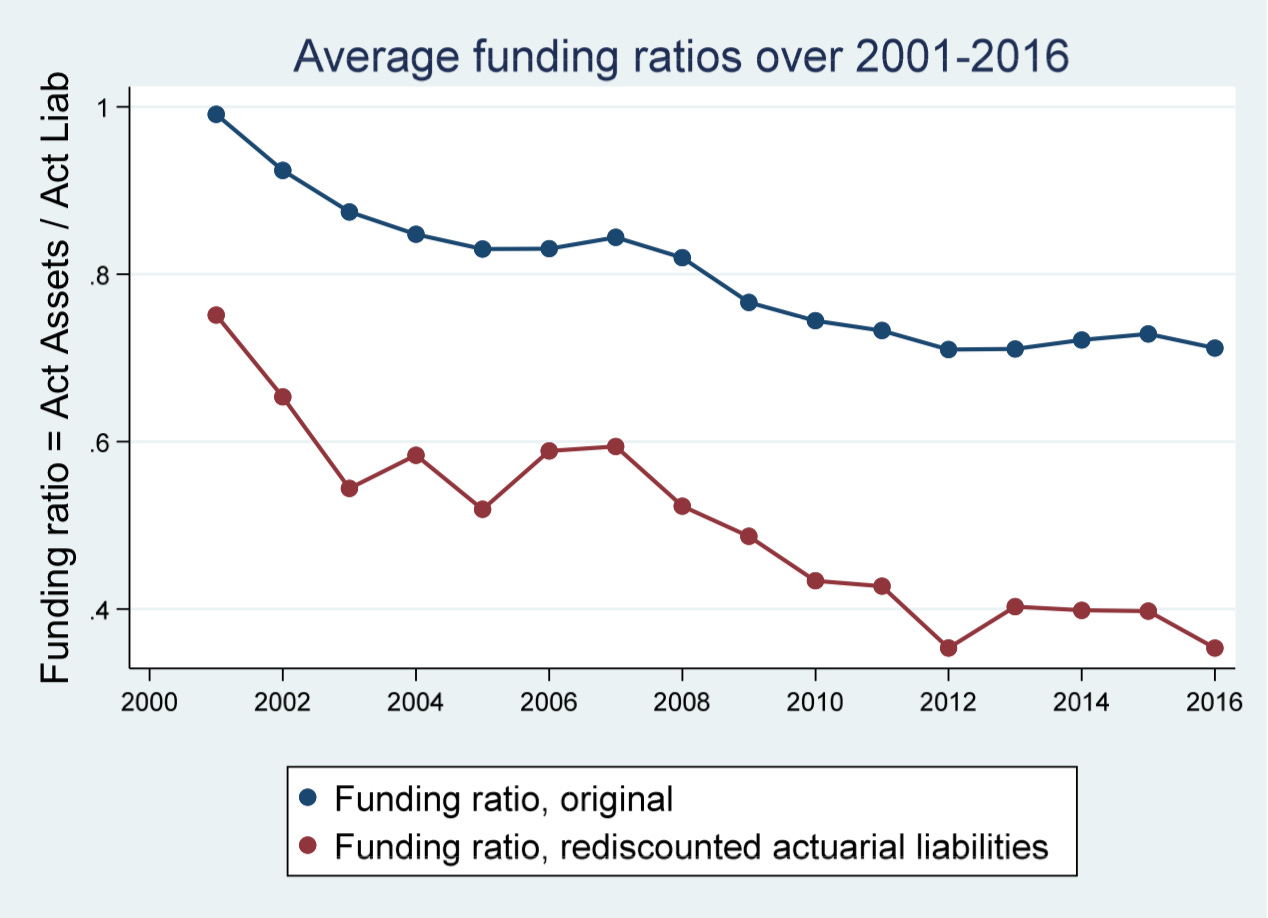

Let’s first take a look at the official funding ratios (the ratio of assets relative to the present value of future liabilities) of the 100 or so public pension plans in their sample. In 2001, the average funding ratio was close to 100% but despite the strong returns of stock markets and declining yields in Treasuries that boosted returns on all fixed income asset classes the average funding ratio declined to about 70% in 2016.

Funding ratios of public pension funds in the US

Source: Lu et al. (2019).

And these are only the official funding ratios. Currently, generally accepted accounting standards require pension fund liabilities to be discounted by a discount rate derived from the asset mix of the pension fund. But why the risk and timing of liabilities should be related to the risk and timing of equity returns, for example, is anyone’s guess. It makes no sense to use equity returns as input into the discount rate for pension fund liabilities. Instead, as practically every pension fund expert in the world has pointed out by now, one should use discount rates that reflect the risk and timing uncertainty of the liabilities of the pension fund.

Unfortunately, this data is not publicly available but in the paper the researchers made an effort to estimate the true funding ratio of the public pension funds in their sample. And the results are disastrous. The average funding ratio is more likely around 40% than 70%!

Estimated actuarial funding ratios of public pension funds in the US

Source: Lu et al. (2019).

In most countries, private pension funds with such massive underfunding would be forced to either restructure or close. Yet, thanks to some simple accounting tricks, the true level of underfunding has been covered up for years.

One of the tricks to use to keep funding ratios high is to keep expected returns for risky assets, such as equities high because that will allow the pension fund to discount liabilities at a higher discount rate. And despite a ten-year equity bull market and steadily declining Treasury yields, the expected returns of public pension funds remain stable at 8% per year. Every investor knows that expected returns vary over time, depending on the valuation of the assets today. But public pension funds seem to be oblivious of that fact.

Of course, they aren’t. They know full well that their expected returns are too high at the moment and that their true funding ratios are lower than their published numbers. But they can’t say that out loud because that would start a discussion about who is going to fund the gap. And in the case of public pension funds the answer to that question is very simple: it’s taxpayers.

So instead of owning up to the problem, politicians and trustees of public pension plans rather kick the can down the road and assume unrealistically high expected returns and discount rates for liabilities. And to achieve these high returns, they have to reach for yield, particularly in the fixed income space where current yields are extremely low. No wonder, bank loans, high yield and private debt are so popular with pension funds these days…

Expected returns of public pension funds in the US

Source: Lu et al. (2019).