The shadow payment system: An ignored risk

My friend Paolo Sironi complained on his recent trip to China that he couldn’t use cash. Either you have Alipay or you are lost. As you can see from the photo below, he wasn’t happy.

Apart from the obvious questions about the benefits and drawbacks of a cashless society, I was starting to wonder what would happen, if Alipay filed for bankruptcy? We live in a world where more and more of our financial transactions are not performed in cash or via wire transfer anymore but on shadow payment platforms. Just like the wider shadow banking system performs traditional banking functions outside the regulated banking system, so do shadow payment providers. The basic functions of a payment system are to provide liquidity (funds can be converted to and from cash at any time without delay), reliable transfer of funds from one participant to another, and custody functions (payments are held in custody for short, but often also long time).

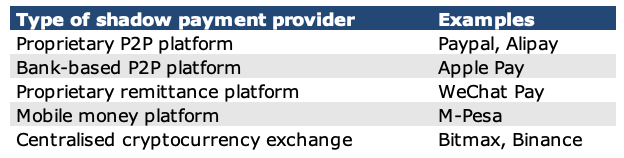

As Dan Awrey and Kristin van Zwieten show, there is now a wide-ranging system of shadow payment providers that can be classified into five different groups. First, there are proprietary peer-to-peer (P2P) platforms that take money from customers and transfer them to other customers. They typically also allow customers to keep the money on the platform for as long as customers want. While in possession of the customers’ funds, they provide custody for the funds. The world’s biggest proprietary P2P platforms are Alipay and Paypal and they have provided convenient and low-cost payment services to billions of individuals and businesses.

Types of shadow payment platforms

Source: Awrey and van Zwieten (2019).

However, nobody ever seems to ask what happens if these platforms become illiquid or insolvent? These payment providers are typically regulated like any other private company and Paypal explicitly states in its terms and conditions that customer funds constitute an unsecured debt of the company. Hence, if Paypal would file for bankruptcy it would likely take months, if not years for customers to get their money back and they could face significant haircuts given their subordinated status relative to other creditors. Crucially, a company like Paypal is not subject to the usual bank regulations that aim to protect customer funds. Paypal is not subject to deposit insurance regulation and hence, customer funds are not secured. Even more crucially, should Paypal become illiquid, it does not have access to the central bank as lender of last resort to keep it afloat and mitigate potential spillovers across the payment system and other payment providers.

In contrast, a bank-based P2P platform like Apple Pay does not have custody of customer funds directly but keeps customer funds at banks. If I buy a train ticket and pay with Apple Pay, funds are directly transferred from my bank account to the account of the train operator and in return, I get to enjoy a ride on a non-air-conditioned British train that tends to run 10 minutes late for every 30 minutes of scheduled distance.

Then, there are remittance platforms like WeChat Pay where customers can send electronic money directly to other customers. Custody is very limited in time and effectively is made only for the time it takes for money to move from the payer’s account to the payee’s account.

Another system is run by mobile money platforms that have sprung up in emerging markets like Safaricom’s M-Pesa. These mobile money systems essentially work like banking used to work in the Middle Ages before the invention of banks. Back then, customers would deposit precious metals like gold with a local goldsmith who in turn would hand the customer a certificate. These certificates could then be used for trade while the gold remained safely in the hands of the goldsmith. If the goldsmith wanted to issue more certificates (or notes) he needed to get more gold from other goldsmiths. The network of goldsmiths ensured that enough specie was available in the places where cash was needed. Similarly, agents of Safaricom provide e-money to customers of M-Pesa. If they want to issue more e-money, they need to deposit cash with other agents up the ladder to large wholesale agents that are linked (but legally separated) from Safaricom. With this system, Safaricom and other providers of e-money are able to bank the unbanked and provide basic payment services to customers without sufficient credit and access to traditional banks.

Finally, the most controversial type of shadow payment providers are cryptocurrency exchanges like Binance and Bitmax. It is in this area that we have seen the risks of the shadow payment system materialise. When Mt. Gox failed in 2014 many customers could not find their bitcoin anymore. Some of the bitcoin were stolen but other claims became part of the bankruptcy proceedings in Japan and the United States. Even today, six years after the bankruptcy, customers have unresolved claims on their funds demonstrating how illiquid and risky these shadow payment providers can become.

But at least, Mt. Gox was incorporated in Japan, a country with a sensible bankruptcy law. In their analysis of more than 100 shadow payment providers, they could not identify the country of incorporation of half the platforms. Good luck enforcing your rights with a company if you don’t even know where it is.

Country of incorporation of shadow payment providers

Source: Awrey and van Zwieten (2019).

Currently, shadow payment providers work in a largely unregulated environment and thus provide much lower customer protection than banks. Hence, using Apple Pay is inherently safer for customers than using Paypal, simply because Apple never holds custody of the funds. Of course, Paypal and other shadow payment providers are not completely unregulated. The United States, the UK, and the EU all have some minimal regulation in place, but given the size of these major payment providers, these regulations hardly provide any significant protection for customers.

Interestingly, because China is on its way to becoming cashless and because Alipay is so dominant in China, customer protection is far more advanced there than it is in the West. Since 2019, payment providers like Alipay and WeChat Pay have to hold 100% of the funds of Chinese customers in a non-interest bearing account at the People’s Bank of China (PBOC). While this costs Alibaba and Tencent an estimated $1 billion per year in foregone interest income, it also means that customer funds are safer there than anywhere else in the shadow payment system.