This explains why my performance is so good and my career so bad…

The cool thing about machine learning technologies is that you can create a completely new kind of research that was previously impossible to do. The problem with machine learning technologies is that you can use it to do ever more ridiculous research that was previously impossible to do. I let you judge, in which bucket the research by Chengyu Bai and Shiwen Tan falls.

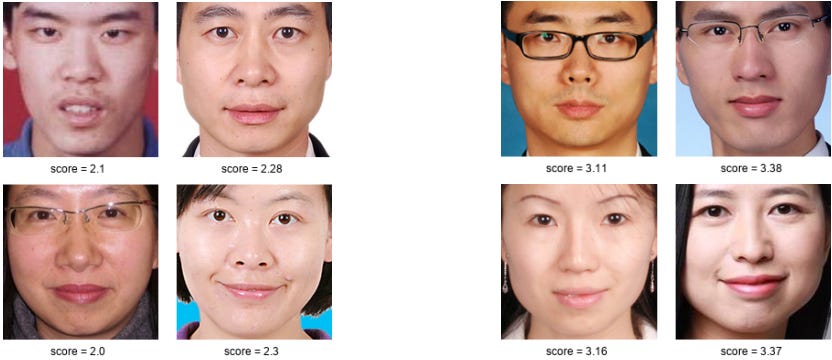

They used a machine learning algorithm to classify the faces of fund managers in China as more or less attractive. Below is an example of faces classified in the lowest quartile by attractiveness (left) and highest quartile by attractiveness (right).

Fund manager faces rated by attractiveness

Source: Bai and Tan (2023)

Once this kind of fund management “Facebook” has been created one can examine if there are systematic differences between the performance and flows of funds with attractive and less attractive fund managers.

First, the boring results: Attractive fund managers attract more money and have a higher chance of being promoted. Fund managers whose faces are one standard deviation more attractive (whatever that is supposed to mean) benefit from an average increase in flows into their funds of 1.1% per year. At fund platforms where the face of the fund manager is shown to retail investors, the excess fund flows increase to 1.9% of assets. No surprise also when we learn that attractive fund managers are more likely to be promoted internally and take charge of more funds and bigger funds over time.

Where things get weird is when the study claims that fund managers with less attractive faces systematically outperform fund managers with more attractive faces. Assuming that good-looking fund managers may be overconfident in their abilities while less attractive ones tend to work harder to prove their worth, they find that this seems to be true. Attractive fund managers tend to invest more in lottery and glamour stocks while less attractive ones invest more in value stocks and have higher active share. Put together, they claim that funds run by unattractive fund managers outperform funds run by attractive fund managers by more than 2% per year.

If only I could believe these results. It would explain why my performance is good, yet my career is so bad…

*feels ugly and old*

*looks in mirror*

*congratulates self on looking like a top tier fund manager*

*mood lifted for whole day*

:-D

That last sentence.