Value is not a ‘risk premium’

One of the constant quarrels practitioners like me have with academics is that academics have a very strange definition of the term ‘risk’. Much has been said about the notion that academics have historically defined the risk of investments as the standard deviation of returns (i.e. volatility). This was due to computational limitations in the 1950s and 1960s when modern portfolio theory was developed but persisted into the 21st century. Thank goodness, the number of academics who use proper downside risk measures is increasing.

Another term tends to make me cringe as well. It is the term ‘risk premium’. The notion behind it is that assets that have systematically higher risks have to be rewarded with systematically higher returns to compensate investors for taking on that risk.

But normal people don’t think that way.

One of the experiments I liked to do with retail clients is to ask them if they think equity investments are riskier than owning a house. Most people will say that equities are riskier than houses. Then I asked them if they think if equities have higher returns than houses. A substantial minority (and in the times of the property boom before 2008 a majority) of people will say that houses have higher returns than equities. But that would mean that houses have higher returns with lower risk – something that should not be possible in the world of modern portfolio theory.

If equities are riskier than houses, then they should earn a risk premium in order to entice enough investors to buy them. If the risk premium isn’t high enough, then prices have to drop until they are. The same is supposed to hold true within stocks. Riskier stocks should earn a risk premium over safer stocks.

Tell that to the people investing in low volatility stocks…

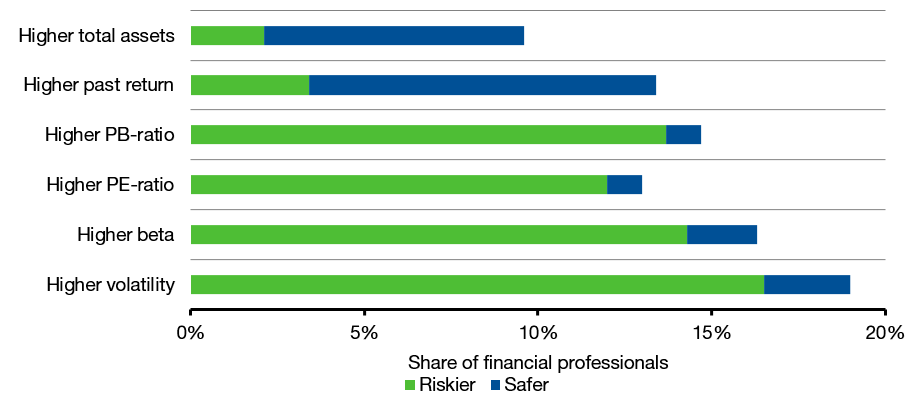

A recent experiment recruited 71 financial professionals in Germany via the CFA Germany and the DVFA Germany. All of the participants are financial experts in the sense that they have passed or studied for rigorous exams testing their knowledge in investment etc. So, it is safe to say that these people know what a risk premium is and how risky different stocks are in practice.

These participants were confronted with several choices for equity investments one at a time and had to estimate how risky or safe these stocks were and what their return expectations were for these stocks. The participants were then asked to describe based on which variable they most relied in their decision and which of severable variables indicated to them that the stocks was safer or riskier than average.

Perception of stocks as riskier or safer depending on the metric

Source: Merkle and Sextroh (2020)

The results were mixed, so to say. Stocks with higher volatility and higher beta were perceived by the majority of financial professionals as riskier than average. However, value stocks (i.e. stocks with a lower PE-ratio or a lower PB-ratio) were perceived as safer than growth stocks by the majority of professionals. Furthermore, high momentum stocks, i.e. stocks that have had high returns in the past were perceived as safer than average.

But, stocks with high price momentum tend to have higher PE-ratios and higher PB-ratios. Furthermore, if the price has gone up for a while, mean reversion poses a relevant risk for a setback in the future. Yet, people who use past returns as their main criterion to assess the riskiness of a stock often cite exactly this metric as a reason why they think the stock is safer.

The academic literature also assumes that value stocks outperform growth stocks in the long run because value stocks are stocks of companies that are systematically riskier than growth stocks (e.g. because they are close to default or because they are operating in an inherently more risky industry, etc.). Yet, finance professionals don’t think value stocks are riskier than growth stocks. Quite the opposite. The high PE-ratios of growth stocks are typically cited by professionals as arguments, why these stocks are riskier.

So either the academics are wrong in their theories why value outperforms growth or even finance professionals have no idea what they are doing. You choose which explanation you find more credible.

Primary reason why stocks are riskier or safer

Source: Merkle and Sextroh (2020)

Well, good idea but I cannot close the email channel because people typically just reply to the email that the blog is sent to 🙁

Well, it’s an elite blog this one with not too many people following it 😜 But seriously, most readers write to me via email and I have lots of exchanges directly with them.