What is an asset class?

We live in a world where the search for diversification and alternative returns in a portfolio is the main objective. Many investors are wary that low interest rates may have driven the valuations of stocks, bonds and other asset classes to unsustainable heights. So, we need to look for uncorrelated assets in our portfolios. Of course, product providers are all too happy to oblige and tout everything under the sun as a new asset class that can diversify your risk. But let’s take a step back and ask ourselves what an asset class is in the first place.

There is no universally accepted definition of an asset class. Some people would argue that an asset class is a financial asset with certain cash flows, but that would mean that commodities are not an asset class. Others may argue that an asset class has to pay a risk premium, but in this case, cash and money market investments would not be an asset class.

The definition that I have been using for many years is that an asset class is a group of assets with similar exposure to the fundamental drivers of the economy.

The problem with this definition is, of course, that it simply shifts the question one level up. It’s as if I would say that life didn’t start on Earth but instead came from the aliens who landed here some time ago. But how did alien life start, then?

So, the ultimate question to me is, what are the fundamental drivers of the economy and how do they influence different asset classes?

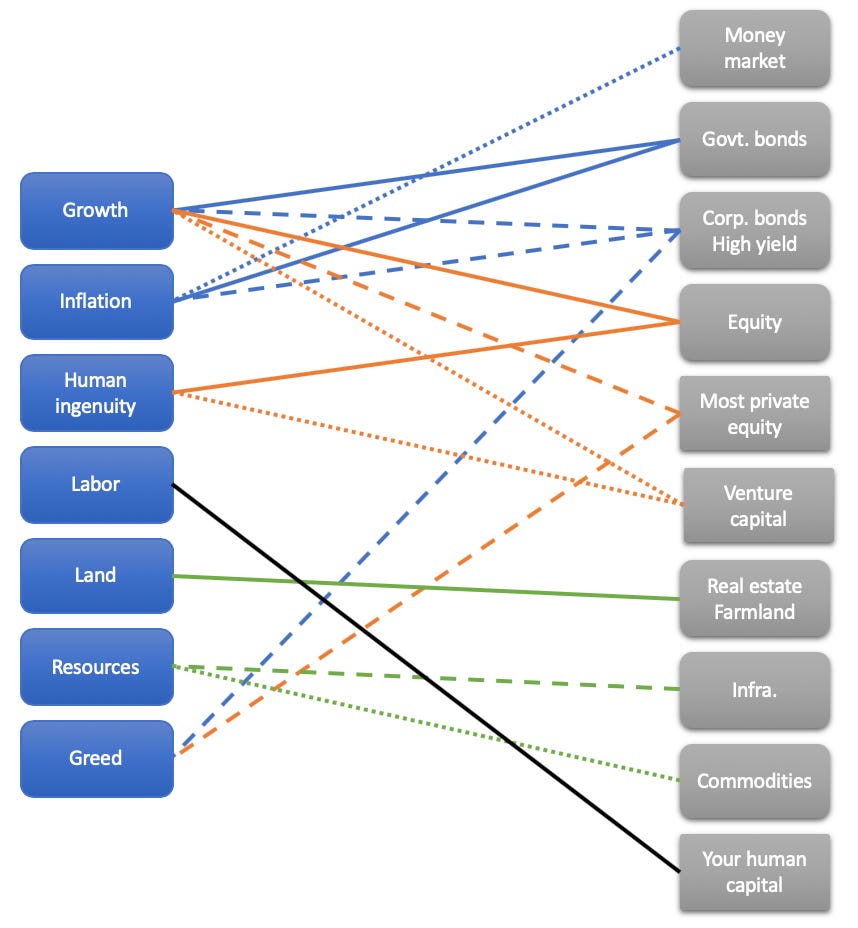

The way I see it, there is a potentially wide range of drivers of the economy, but there is only a handful or so that really make a difference:

Growth

Inflation

Human ingenuity

Labour

Land

Resources and infrastructure

Greed

The last one may sound like the odd one out but bear with me. What I mean with greed is the human tendency to want more of everything and in particular more money. This desire to create more money out of an existing pile of capital is at the heart of basically the entire financial industry. If a bank lends money to a corporation or a private household it does so to earn interest. Hence, all credit-related assets, be it corporate and high yield bonds or mortgages are exposed to the fundamental driver of society to not be satisfied with the money you already have. Hence, the credit cycle, which is essentially a cycle of greed and fear is an expression of this fundamental nature of human beings.

Another closely related driver of the economy is what I have called human ingenuity. It is our drive to make things better over time. Economists typically use the catch-all term productivity, but I prefer the term human ingenuity because it is essentially driven by our ability to ask questions and find answers to existing problems that drives productivity growth and makes things better over time.

With land, I imply that it is hard to run a society if you don’t have the land to feed the people, house them or build factories and offices etc. Hence, land and its location is the main driving force behind real estate returns, for example.

But the economy not only needs land as an input factor. It needs raw materials, most of which are still derived from natural resources (renewable and non-renewable) and it needs the basic infrastructure to get the raw materials to the production centres and the end consumers. I separate these input factors from land because you cannot create new land (at least not on a large scale) but you can develop access to new input factors by opening a mine, building roads, etc.

Finally, growth, inflation and human labour should be self-explanatory as fundamental drivers of the economy.

Note also, that what some people consider fundamental drivers of asset class returns like the real interest rate are not part of that list. Real interest rates are effectively set in reaction to expectations of growth, inflation and other factors, so I don’t consider them truly fundamental.

If I look at this list of fundamental drivers of the economy, I can map every asset class based on its exposure to these drivers. Stocks, for example, are driven mostly by economic growth and human ingenuity. Yes, they are also sensitive to inflation etc. but the main driver of stock returns are the rate of growth of the economy overall and the ability of entrepreneurs and businesses to increase productivity and develop new products and services that people want to have.

Government bonds are driven by the inverse of growth (slower growth meaning higher bond returns through declining real rates) and inflation. If you get credit exposure, then you also get some kind of exposure to greed. After all, why bother with corporate or high yield bonds if you could be satisfied with the return on your safe government bonds? I hope this makes it clear that credit exposure really is about greed.

Private equity typically is an asset class that is exposed to economic growth. In the case of venture capital, you also get a heavy dose of human ingenuity exposure while leveraged buyouts in my view are just exposed to greed since all they deliver is higher returns through the use of debt.

And what about hedge funds? To me, hedge funds aren’t really an asset class, since they invest in other asset classes. They are simply a form of active management and hence an expression of greed to get more return for a given level of risk than what would be achievable with passive investments.

To summarise, I have created the chart below that maps different asset classes to different fundamental drivers of the economy:

Once you have come to this point, however, you understand something truly important: There is no need for a large number of different asset classes in your portfolio. The plethora of alternative assets touted in the media is essentially a rehash of the exposure to different fundamental drivers of the economy. So, the next time someone comes to you to promote the benefits of aircraft leasing as an asset class, you can go back to the chart above and see that aircraft leasing is simply an expression of greed (it’s a credit instrument) with a little bit of economic growth exposure thrown in. But if you already have stocks in your portfolio and exposure to high yield, you probably won’t get much diversification by adding aircraft leasing to your portfolio as an asset class.

Many alternative asset classes aren’t truly different. This usually becomes painfully obvious once a crisis hits and the seemingly uncorrelated alternative assets suddenly become highly correlated with stocks or other assets. In fact, the chart above can help you identify how alternative asset classes might react in a crisis because then, all markets do is focus on the exposure to these fundamental drivers and their expected future development.