What makes an asset ‘safe’?

Stupid question, I know, but if you look into the world of the safest assets, different investors have different preferences. A case in point is the massive issuance of Eurobonds during the Covid pandemic.

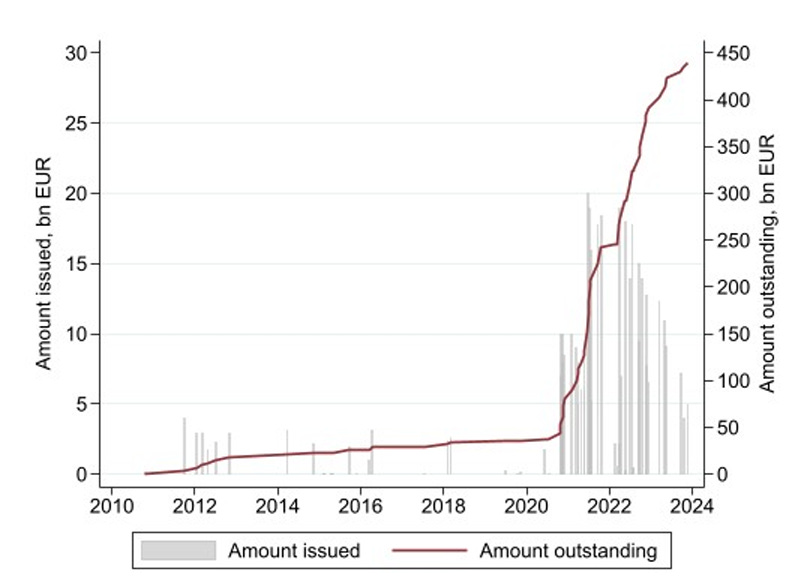

During the pandemic, the EU took the unprecedented step of issuing not just pan-European bonds that are secured by the members of the EU in proportion to their share of GDP, but true Eurobonds where the country with the best credit (usually Germany) implicitly guarantees the whole issuance should other EU member states default.

In total, the EU agreed to issue a massive €2tn of these common EU bonds. On top of that, there are bonds issued by supranational organisations like the European Investment Bank (EIB), bonds issued by the European Stability Mechanism (ESM), and the European Financial Stability Facility (EFSF). All of these bonds have a AAA rating and are debt against the EU as a whole. Plus, there are national government bonds, some of which are also AAA rated (Germany, Netherlands, Luxembourg).

EU debt issuance during the pandemic

Source: Breckenfelder et al. (2025)

All of them are denominated in Euros, so no currency risks. And all of them are supposedly as safe as Treasuries (or rather safer than Treasuries since the US no longer has a AAA rating from Standard & Poors or Fitch).

Researchers from the ECB and Imperial College in London used proprietary data to examine who bought which bonds during these days and infer from it, why they bought those bonds. Normally, this would be an academic exercise, but given the epochal change in fiscal spending under way in Europe it has taken on a new importance.

The chart below shows the holdings of the EU’s supranational bonds over time split into different investor groups. Note how the big wave of newly issued bonds was mostly picked up by banks and mutual funds together with pension funds. Insurance later joined the party as well once yields stated to rise in 2022. But the main insight is that the marginal buyers of these supranational AAA-rated bonds are banks and funds.

Holders of EU supranational bonds

Source: Breckenfelder et al. (2025)

These institutional investors prefer supranational bonds over national AAA-rated bonds because they trade at substantially higher yields and allow these investors to increase their portfolio returns. Additionally, from an accounting perspective and a regulatory perspective, these bonds are the safest assets out there. Especially for banks, this means they can reduce the amount of capital held against these investments.

Meanwhile, these newly issued supranational bonds crowd out national government bonds with the same rating in the portfolios of banks and funds as becomes clear in the chart below.

Holders of EU national government bonds

Source: Breckenfelder et al. (2025)

The main buyers of national government bonds – the people picking up the slack from the banks and funds – are private households. These investors have a significant home bias, and they often identify with the government of the country they live in. So, they prefer national government bonds over EU supranational bonds as ‘safer’.

Indeed, supranational bonds don’t have that ingrained investor base like national government bonds do. While people may think of themselves as German or Dutch, nobody thinks of themselves as EU-an or EIB-an. Some may identify as ‘European’ but that is different than identifying with the EU as an institution.

This lack of ingrained investor base helps to explain why European supranational bonds trade at higher yields than German or Dutch government bonds, even though the European bonds are guaranteed by all EU member states, not just one, which should make them safer. And it is this psychological disconnect that makes these supranational bonds the safe asset for banks and funds, while national government bonds are the safe asset for private investors.

One reason for retail investors preferring national bonds may be tax advantages.

Thanks for that Joachim. One objection: I believe the EU's issuance for NGEU was *not* joint and several, that is, Germany would not be liable for other countries shares. If there was joint and several liability, the German constitutional court would have objected (as the financial autonomy of the German parliament would have been infringed - in english: Germany would have to cough up money its parliament had not decided to cough up). There were several cases brought before the GCC on those (and other) grounds, which it rejected.