When will value stocks perform again?

Everyone who is interested in value investing knows that this investment style has had an awful time. The US has experienced the longest economic expansion and the longest bull market in history since the end of the financial crisis and at the same time, value has underperformed growth for more than a decade now. And to make things worse, the underperformance of value stocks has not only been long-lasting but was also amongst the largest ever recorded.

Value investors are a hardy breed, but there is a limit to everything. Because what doesn’t kill you, does not make you stronger, but much weaker. In fact, what doesn’t kill you typically gets you really close to dying. At least in the world of value funds more and more are facing significant outflows or are struggling to retain investors who are losing patience.

Value investors desperately need a break but what is going to give them their long-desired performance recovery? The brief market setback in the fourth quarter 2018 didn’t trigger an outperformance of value stocks, even though we know that value stocks tend to outperform during a momentum crash. Josef Lakonishok and his colleagues have shown a quarter century ago that value starts to outperform once momentum and trend-following investors rush to the exits. However, the market decline at the end of last year wasn’t so much of a crash as more of an orderly retreat of investors for a couple of weeks. But once Christmas arrived, markets recovered quickly so that investors didn’t get spooked for too long. What value investors really need is a proper market crash which could be triggered by an external market shock. A significant sovereign crisis like the Asian crisis 1997 or the Russia crisis 1998 would do. Unfortunately, predicting such external shocks is about as easy as predicting earthquakes.

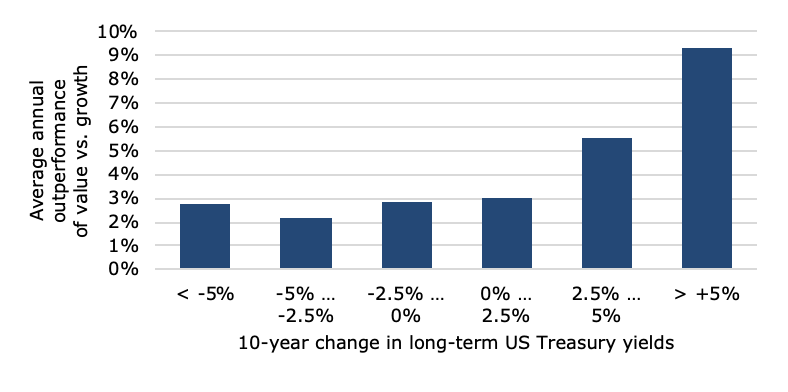

Another trigger for a sustained outperformance of value stocks would be higher interest rates, as I have shown here. As long as rates stay low, growth companies, which are often highly leveraged, can refinance their debt at low cost. Thus, even if revenues decline significantly, these highly leveraged companies can still cover their interest payments and do not have to shrink their balance sheet. Traditionally, once interest rates rose over a prolonged period, value companies tended to outperform.

Debt cost and the value premium

Source: Fidante Partners.

But of course, the possibility of seeing higher long-term bond yields is very low for the next twelve months as the global economy cools and central banks have gone back to easing mode.

Thus, we are left with the third major possibility for value stocks outperformance: a proper bear market. Messaoud Chibane and Samuel Ouzan recently showed nicely, how the value premium changes depending on the market environment. When overall market returns for the preceding two years were positive, the value premium disappeared, while the value premium shot up after a two-year period with negative market returns. At the time of writing the rolling two-year return of the S&P 500 is 17.5%. Thus, all we need for value to outperform is for the stock market to decline by close to 20% and we are good…

Well, most people won’t really feel too good about that, but such is life. “You can’t always get what you want”, as the eminent philosophers Mick Jagger and Keith Richards once said, “but if you try sometime you find, you get what you need”. And we might get what we need if the US and Eurozone economies dip into recession in 2020 as I fear they will. But until then, value investors are likely to continue to suffer some more.

Value premium and market environment

Source: Chibane and Ouzan (2019).